Anthropic: Private Investor Report — April 2026

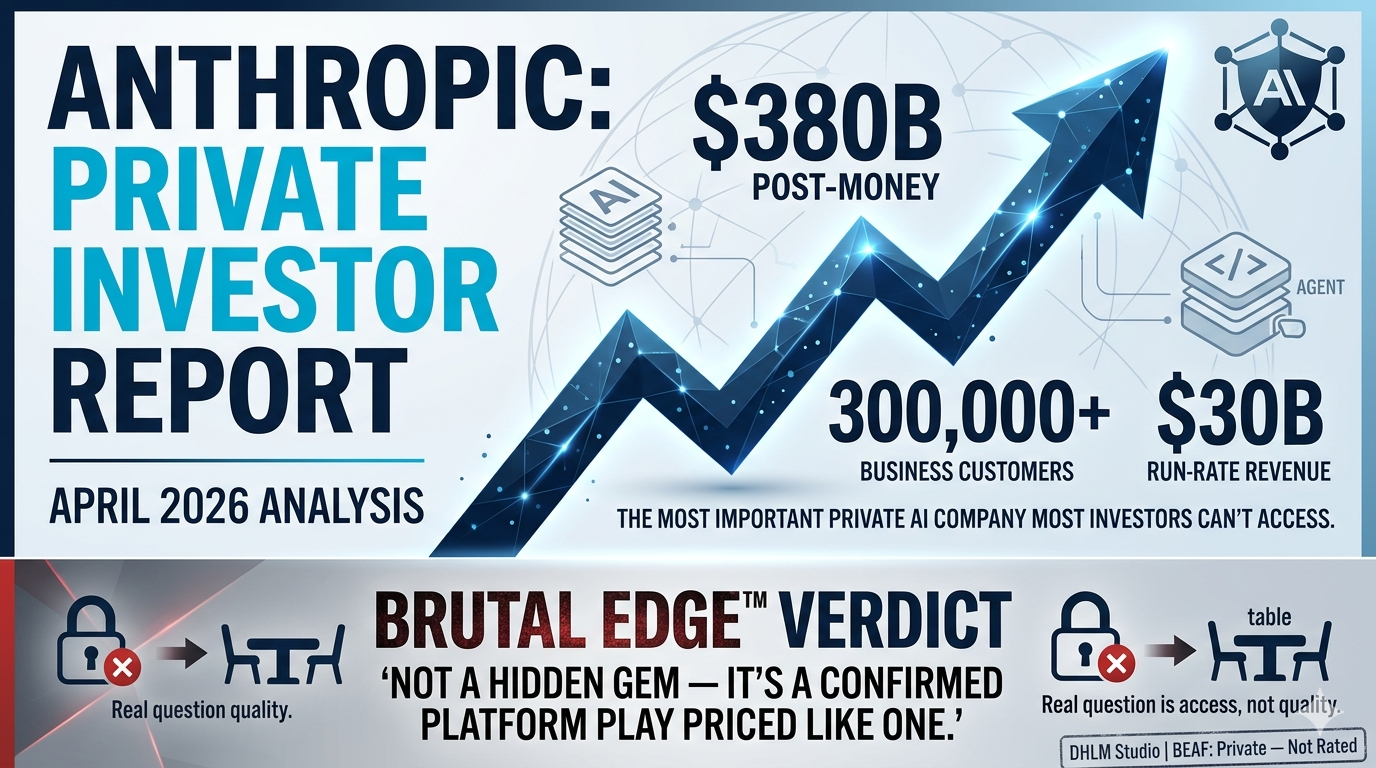

Anthropic at $380B post-money, $30B run-rate revenue, 300,000+ business customers. The most important private AI company most investors can't access. Here is what you need to understand before you try.

Editor's note: Anthropic is a private company. There is no public-market ticker today, and the most relevant valuation data comes from private funding rounds and secondary transactions. As of April 14, 2026, Anthropic has disclosed a $30 billion Series G at a $380 billion post-money valuation, and has said its annualized run-rate revenue has passed $30 billion. That run-rate figure is important, but it is not the same thing as audited full-year revenue.

Anthropic matters because it is no longer just "an AI lab with a good model." It increasingly looks like a full-stack enterprise AI platform: frontier models, a fast-growing API business, coding and agent products, deep cloud distribution, and a corporate structure built around safety and long-term governance. For investors, that combination is rare. It also explains why so many people are asking the same question: is Anthropic one of the most attractive private AI investments in the market today?

The short answer is yes — but the price tag already knows it. Anthropic looks like one of the highest-quality private AI assets available. It does not look like a cheap one. The investment debate is no longer about whether the company has product-market fit. It clearly does. The real debate is whether Anthropic can turn today's extraordinary growth into durable platform economics while managing the cost, governance, and safety burdens that come with being a frontier AI company.

> 🔥 BRUTAL EDGE™ VERDICT

> "Anthropic at $380B is not a hidden gem — it's a confirmed platform play priced like one. The real question isn't quality. It's whether you can even get a seat at the table."

BEAF: Private — Not Rated

Anthropic is a private company. Standard BEAF 6-axis scoring is not applicable. This report uses qualitative framework analysis in place of quantitative BEAF scoring.

The Company

The simplest way to understand Anthropic is this: it sells intelligence, agent capability, and trust. The company's flagship product family is Claude. Around Claude, Anthropic has built Claude Code for software development, Managed Agents for enterprise automation, and a growing workplace layer that includes Slack, Excel, PowerPoint, Word, Chrome, and enterprise search integrations. Anthropic is not just selling a chatbot; it is building an AI work platform.

The company's identity is unusually important here. Anthropic is a Public Benefit Corporation, and its purpose is the "responsible development and maintenance of advanced AI for the long-term benefit of humanity." It also has a Long-Term Benefit Trust — an independent body with authority to select and remove part of the board, with that authority designed to grow over time. That structure makes Anthropic different from a conventional maximize-shareholder-value startup. It is part of the company's appeal, and part of its investment complexity.

That mission is not just branding. Anthropic's research identity is built around reliable, interpretable, and steerable AI systems, its Constitutional AI approach, and its Responsible Scaling Policy, now on version 3.0. In March 2026, it also launched The Anthropic Institute, a new effort focused on how powerful AI will affect jobs, resilience, governance, and the broader economy. Put plainly, Anthropic is trying to become not only a model builder, but also one of the companies that defines how frontier AI is governed.

The Business Model

Anthropic's monetization model is much easier to understand than many casual readers assume. It has a consumer subscription business, a team and enterprise seat business, and a usage-based API business. On the consumer side, Claude offers Pro plans at $17 per month billed annually or $20 billed monthly, while Max starts at $100 per month. For organizations, Team starts at $20 per seat per month billed annually, and Enterprise starts at $20 per seat plus usage at API rates.

The most important investor point is that Anthropic is not primarily monetizing attention; it is monetizing work. Its business model is built around people and companies paying to use Claude for coding, analysis, workflow automation, search, and enterprise tasks. That matters because it gives Anthropic a much more software-like revenue profile than a consumer internet profile. The company has also publicly committed to keeping Claude ad-free, which reinforces the idea that its long-term revenue model is based on subscriptions, enterprise contracts, and API usage — not advertising.

Recent reporting suggests the growth engine is increasingly the Claude Platform, not the consumer chat product by itself. WIRED reported that the majority of Anthropic's recent growth has come from the enterprise product that lets developers access Claude through an API, and that Managed Agents is designed to lower the barrier for businesses to deploy autonomous AI systems. That is exactly the kind of shift investors should want to see: from a popular model to a productized enterprise platform.

The Traction

The reason Anthropic has become such a serious investment topic is not hype alone. It is traction. In October 2025, Anthropic said it served more than 300,000 business customers, and that the number of accounts generating more than $100,000 in run-rate revenue had grown nearly 7x year over year. Then, on April 6, 2026, the company said its run-rate revenue had passed $30 billion, up from about $9 billion at the end of 2025, and that the number of customers spending over $1 million annually had risen to more than 1,000, doubling in less than two months.

That kind of growth is why private investors are willing to pay up. In February 2026, Anthropic raised $30 billion at a $380 billion post-money valuation. By simple arithmetic, that values the company at roughly 12.7x current revenue run-rate. That is a rich multiple, but it also tells you how the market is thinking about Anthropic: not as a point product, and not as a lab experiment, but as a potential long-term platform company in enterprise AI.

It is also worth noting that Anthropic appears to have real private-market demand, not just paper enthusiasm. Bloomberg reported that the company recently completed a tender offer at the same valuation basis as its February fundraising, but that many investors could not buy as much as they wanted because employee share supply was limited. That is not a valuation argument by itself, but it does tell you something about market appetite and scarcity.

The Differentiators

Anthropic's strongest differentiator is not simply "better model performance." It is the combination of enterprise focus, safety positioning, and distribution. The company's recent model launches emphasize coding, agents, professional work, finance, tool use, and computer use. Claude Code is described by Anthropic as an agentic coding system that can read a codebase, make changes across files, run tests, and deliver committed code. Managed Agents extends that idea by giving enterprises a harness, memory layer, and sandbox so they can deploy AI agents more easily at scale.

The second differentiator is trust. Anthropic's enterprise offering includes the features large organizations actually care about: SSO, SCIM, audit logs, role-based access, compliance APIs, data retention controls, enterprise deployment controls, and a HIPAA-ready offering. It also states that customer content is not used for model training by default on enterprise plans. In the AI market, buyers are not choosing only on benchmark scores. They are choosing on security, compliance, governance, and whether deployment feels safe inside a real organization.

The third differentiator is distribution. Anthropic says Claude is the only frontier AI model available on all three leading cloud providers: AWS, Google Cloud, and Microsoft. AWS is Anthropic's primary cloud and training partner, with Amazon's total investment at $8 billion while remaining a minority stake. Google has committed to a TPU expansion worth tens of billions of dollars, and Anthropic's April 2026 announcement added a new multi-gigawatt compute agreement with Google and Broadcom. Microsoft announced that Anthropic would scale Claude on Azure, that Anthropic had committed to purchase $30 billion of Azure compute capacity, and that Microsoft and NVIDIA would invest up to $5 billion and $10 billion, respectively.

That matters enormously for the investment case. Anthropic is not trying to win with one distribution channel. It is using multi-cloud availability, hyperscaler relationships, enterprise seat plans, and partner-led implementation to reduce customer friction. The March 2026 launch of the Claude Partner Network, backed by $100 million, plus expanded alliances with Deloitte and Infosys, shows Anthropic trying to turn model adoption into organization-wide deployment.

The Investment Case

For a private-market investor, Anthropic's appeal comes from five things happening at once.

First, real demand at scale. This is no longer a story about pilots and demos. Anthropic has a very large business customer base, a rapidly growing population of seven-figure accounts, and one of the fastest revenue ramps in software history.

Second, high-quality revenue. Anthropic's model is based on subscriptions, enterprise seats, and API consumption rather than advertising. That usually produces better monetization clarity and more durable customer relationships than a consumer-attention model. Anthropic's own decision to keep Claude ad-free strengthens that positioning.

Third, platform expansion, not just model expansion. Claude, Claude Code, Managed Agents, workplace integrations, and enterprise admin tools all point in the same direction: Anthropic is trying to own more of the workflow, not just the model call. WIRED's reporting that most recent growth came from Claude Platform is consistent with that reading.

Fourth, infrastructure backing and distribution reach. Very few private AI companies can say they are deeply integrated with AWS, Google Cloud, Microsoft, and a broad partner ecosystem simultaneously. Anthropic can. That does not guarantee victory, but it creates serious advantages in reach, resilience, and enterprise credibility.

Fifth, a distinct identity. Anthropic's governance, Responsible Scaling Policy, Constitutional AI work, and Institute give it a clearer philosophical and policy profile than many peers. There is real commercial value in being seen as the frontier AI company that large organizations can trust with sensitive work.

The Risk Stack

The biggest risk is simple: Anthropic is already expensive. A $380 billion post-money valuation is no longer "early" in any ordinary sense. At this level, the question is not whether Anthropic is interesting. It is whether it can keep compounding fast enough, long enough, to justify a valuation that already assumes very large future cash flows. And the headline $30 billion is a run-rate, not a reported full-year revenue number.

The second risk is infrastructure intensity. Anthropic's business is scaling into enormous compute commitments: tens of billions of dollars of Google Cloud TPU expansion, a multi-gigawatt Google/Broadcom agreement, AWS as primary training partner, and a reported $30 billion Azure compute commitment. Those relationships are strengths, but they also mean the company is operating in a brutally capital-intensive part of the market. Growth is not cheap here.

The third risk is governance complexity. Anthropic's Public Benefit Corporation structure and Long-Term Benefit Trust are core to the company's identity, but they also mean investors are not buying into a standard shareholder-first machine. If management ever has to choose between speed and safety, or between monetization and restraint, Anthropic's structure suggests the answer may not always favor short-term shareholder returns. That is a feature of the company, but investors should recognize it clearly.

The fourth risk is access. Anthropic remains private, and direct access is limited. Bloomberg's recent reporting on the tender offer suggests that even willing buyers could not always get the shares they wanted. That makes Anthropic attractive, but it also makes it difficult for ordinary investors to build meaningful direct exposure at the right price.

The Framework

The cleanest way to think about Anthropic is not as "the company behind Claude." That is too small. A better framework:

Anthropic is trying to become the trusted enterprise operating layer for frontier AI. Its models are the engine, Claude Code and Managed Agents are the wedge, enterprise controls are the trust layer, and its cloud and partner relationships are the distribution machine. That is why the company feels so important to investors. It sits at the intersection of model capability, enterprise software, infrastructure, and AI governance.

For public-market investors, Anthropic is also a reminder that indirect exposure is not the same as direct exposure. Amazon, Microsoft, Alphabet, and NVIDIA all have meaningful strategic ties to Anthropic, but none of them is a clean proxy for owning Anthropic itself. Their businesses are too large and too diversified. For private-market investors, that means Anthropic remains a special asset precisely because direct exposure is scarce.

Bottom Line

Anthropic is one of the most compelling private AI companies in the market today. It has real revenue, real enterprise adoption, real product breadth, real infrastructure support, and a distinct safety-and-governance identity that makes it easier for serious organizations to trust. It is no longer just an AI lab. It is becoming a business platform.

That said, the stock — if it were publicly tradable — would not be a hidden bargain. Anthropic's valuation already reflects immense optimism. The investment case is not "this is undiscovered." The case is: this may be one of the few private AI companies with a believable path from frontier model leadership to durable enterprise platform economics. For investors, that makes Anthropic highly attractive. It also means the bar is now extraordinarily high.

About

Share your analysis

Keep it data-driven. No investment advice.

- Keep it data-driven and respectful

- No investment advice (buy / sell / hold)

- No spam, promotion, or solicitation

- No profanity or offensive content

- Violations are automatically removed

Data: Financial Modeling Prep, Alpha Vantage, CoinGecko

NOT investment advice. Always do your own research.