SpaceX IPO Special Report: The $1.75 Trillion Question

SpaceX's rumored $1.75T IPO would be the largest in history. Revenue breakdown, SOTP valuation, risk scenarios, and our Brutal Edge verdict.

1. Executive Summary

SpaceX's rumored 2026 IPO is not merely another tech listing. If the deal prices anywhere near the widely discussed $1.5T to $1.75T range and raises up to $75B, it would surpass Saudi Aramco and become the largest IPO in market history. More importantly, it would mark the public-market debut of the world's most strategically important private industrial company: part telecom infrastructure provider, part launch monopoly-in-the-making, part defense contractor, and part long-duration option on space transportation.

What makes this deal especially disruptive is the reported intention to reserve an unusually large share for retail investors. If that survives into the prospectus, it would be a sharp break from the standard institutional-heavy allocation model used in mega IPOs. That alone could turn the listing into a global cultural and financial event rather than a conventional underwriting exercise.

But the central question is brutally simple: is $1.75 trillion justified? At that price, investors are not just buying today's launch business or even today's Starlink. They are prepaying for a future in which SpaceX becomes the dominant operator of orbital internet, a quasi-utility in launch, a major defense platform, and eventually the owner of the world's most important heavy-lift logistics system. The bull case is extraordinary. So is the valuation burden.

2. Why This IPO Matters

| IPO | Year | Raised | Valuation |

|---|---|---|---|

| Saudi Aramco | 2019 | $29.4B | ~$1.7T |

| Alibaba | 2014 | $25B | ~$231B |

| SpaceX | 2026E | up to $75B | $1.5T–$1.75T reported |

Saudi Aramco raised about $29.4B in 2019. Alibaba raised $25B in 2014 and finished its first trading day up about 38%. A SpaceX transaction at the top end of current media reports would be far larger than both.

This IPO also matters because a deal of this size could have immediate benchmark consequences. Nasdaq's new rule change, reported to take effect in 2026, allows newly listed mega-cap companies that rank among the Nasdaq-100's biggest constituents to be added after roughly 15 trading days, versus a much longer waiting period previously. That creates the possibility of unusually fast passive-fund demand if SpaceX lists on Nasdaq.

By contrast, S&P 500 inclusion is not automatic. S&P uses committee discretion, requires U.S. listing and size thresholds, and still applies financial viability criteria. The current S&P U.S. Indices methodology shows an S&P 500 market-cap guideline of $22.7B or more, but profitability and committee judgment remain essential.

Editorial conclusion: this IPO matters not only because it is big, but because it could reshape how index providers, passive funds, and retail investors interact with late-stage private giants.

3. The Business: What SpaceX Actually Does

Public discussion still undersells how unusual SpaceX has become. It is no longer just a rocket company. Its economic engine increasingly appears to be Starlink, its credibility anchor is Launch Services, and its valuation optionality sits inside Starship and defense-adjacent businesses such as Starshield.

Editorial revenue mix estimate: Starlink 60%+ of revenue; Launch Services ~25%; Other / Starshield / emerging programs: balance.

| Segment | 2024 | 2025E | 2026E | 2028E |

|---|---|---|---|---|

| Starlink | $6.6B | $11B | $18B | $35B |

| Launch | $3.5B | $4.5B | $5.5B | $7B |

| Other | $0.5B | $1B | $1.5B | $3B |

| Total | $10.6B | $16.5B | $25B | $45B |

These figures are editorial estimates, not reported company guidance. Anchored to Starlink customer growth, SpaceX launch tempo, and defense and lunar contract relevance.

4. Starlink Deep Dive

This is the most important section because Starlink is likely the main reason investors are even willing to entertain a trillion-plus valuation.

Starlink added more than 4.6 million new active customers in 2025 and expanded service to 35 additional countries, territories, and markets per its own 2025 progress report. Third-party summaries place the installed base at over 9 million customers by year-end 2025.

That matters because Starlink is no longer a niche rural broadband product. It is becoming a layered connectivity platform spanning residential, enterprise, maritime, aviation, disaster recovery, government, and direct-to-cell services.

Subscribers: already past the 5M+ talking point; the more relevant question is whether Starlink can sustain multi-million annual net adds.

Geographic expansion: the network added 35 markets in 2025 alone, suggesting the addressable footprint is still widening rather than maturing.

ARPU: a blended $90 to $120 per month remains a reasonable editorial range for modeling, but actual ARPU likely varies sharply by geography and vertical. Because SpaceX has not publicly disclosed Starlink segment ARPU, this remains a modeling assumption.

Competition: Amazon Leo (formerly Project Kuiper) had deployed 241 satellites by early April 2026, still far behind Starlink in scale. OneWeb remains meaningful in enterprise and government connectivity but does not match Starlink's consumer scale.

Why "the AWS of space" is the right analogy

The analogy works because Starlink is building foundational network infrastructure first, with monetization layers following later. Like AWS in its early years, the most valuable feature may not be today's product set, but the platform characteristics: global reach, low latency, resilience, and the ability to serve multiple verticals from the same physical network.

5. The Elon Musk Factor

A SpaceX IPO cannot be analyzed without confronting the Musk premium and the Musk discount.

The premium is real. Markets repeatedly value Musk-led companies not only on near-term cash flows but on the belief that he can compress industrial learning curves, attract elite engineering talent, and redefine category boundaries. Tesla is the clearest precedent.

The risk is equally real. Musk is simultaneously linked to Tesla, SpaceX, xAI, X, Neuralink, and The Boring Company, which raises questions of attention dilution, governance complexity, related-party optics, and political controversy spillover.

Governance is the unresolved issue. Until the S-1 is public, investors do not know the final voting structure, related-party disclosures, or how much post-IPO control Musk will retain. For a company at this scale, governance can directly influence valuation multiple, index eligibility perceptions, and institutional participation.

Manufacturing lens: SpaceX won because it treated rockets as manufactured systems to be iterated, reused, and cost-reduced, not as bespoke monuments. The deepest version of the SpaceX bull case is not "Musk is a genius." It is: he industrialized a category that incumbents managed like a guild.

Put differently: the people who understand manufacturing are more likely to understand SpaceX. Software can scale without atoms. Rockets cannot. SpaceX's moat is not just code, brand, or access to capital. It is a compounding advantage in design-for-manufacture, vertical integration, refurbishment, cadence, and operational learning.

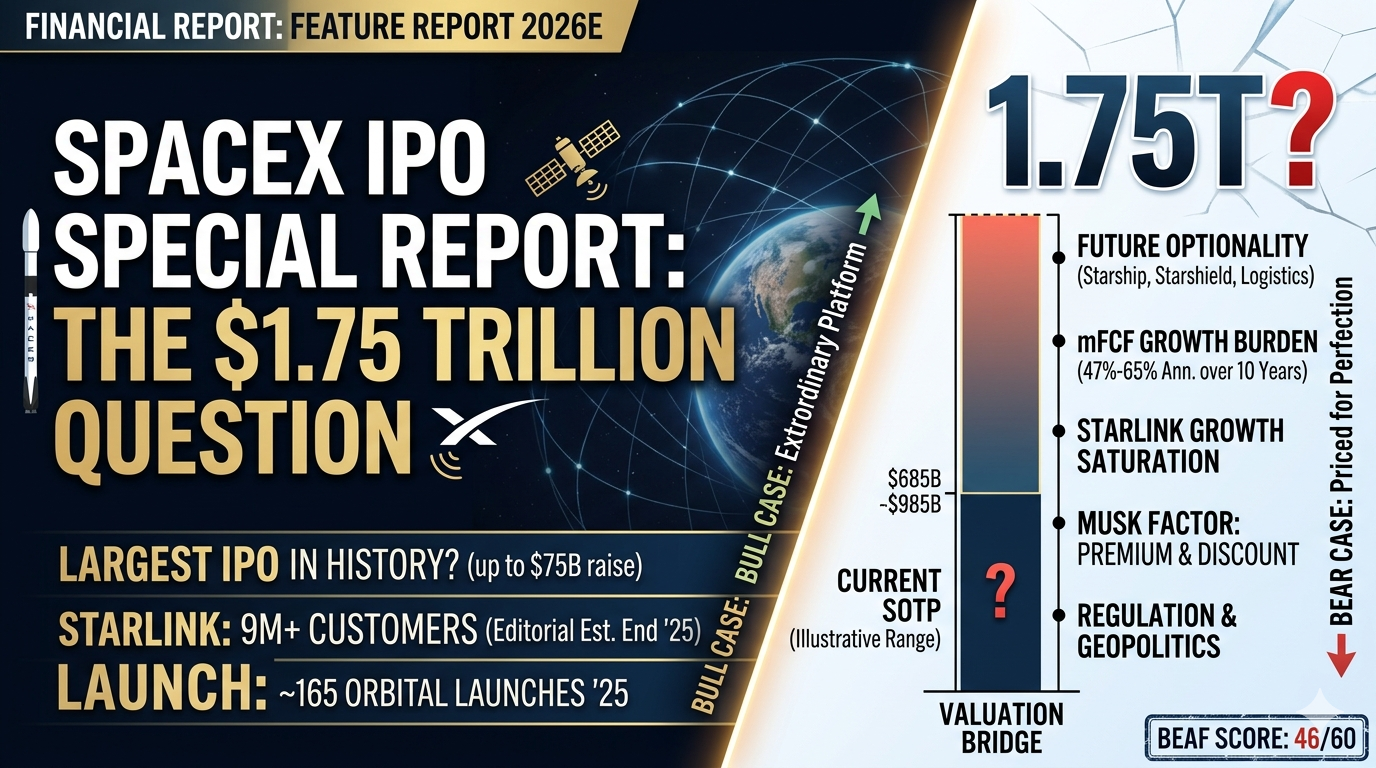

6. Valuation Analysis

This is where the story becomes uncomfortable.

At a reported $1.75T valuation and using a 12% discount rate with 3% terminal growth, the implied long-term cash-flow burden is extreme. In a simple reverse-DCF framework, if SpaceX were generating roughly $2.5B to $7.5B of free cash flow around 2026 — equivalent to roughly 10% to 30% FCF margins on a $25B revenue base — it would still need approximately 47% to 65% annual FCF growth for a decade, ending with something like $350B to $375B of annual FCF in year 10 to justify $1.75T. The valuation asks investors to underwrite one of the largest cash-flow ramps in industrial history.

(Author reverse-DCF calculation; 12% WACC, 3% terminal growth; valuation input based on reported IPO range.)

Sum-of-the-Parts (illustrative)

| Segment | Method | Valuation |

|---|---|---|

| Starlink | 15x 2026E revenue | $270B–$375B |

| Launch | 20x 2026E revenue | $110B |

| Starship / Starshield / optionality | Strategic option value | $200B–$500B |

| Total | $685B–$985B |

That leaves a very large gap versus a $1.75T IPO valuation — roughly a 78% to 155% premium over this SOTP range. The only way to bridge that gap is to assign extraordinary value to outcomes that are not yet mature businesses: Starship becoming the dominant heavy-lift platform, Starlink becoming a global telecom utility, and defense or orbital infrastructure evolving into categories large enough to matter at trillion-dollar scale.

Comparison table

| Company | Revenue | P/S | Market Cap |

|---|---|---|---|

| SpaceX (2026E, reported valuation) | $25B | 70x | $1.75T |

| Tesla | ~$97B | ~15x | ~$1.5T |

| Amazon | ~$650B | ~3.4x | ~$2.2T |

| Boeing | ~$78B | ~1.2x | ~$95B |

| Lockheed Martin | ~$68B | ~1.8x | ~$120B |

Bottom line: the valuation is not justified by current business lines alone. It is justified only if investors are willing to capitalize future monopoly-like economics plus Starship optionality far in advance.

7. Competitive Landscape

In launch, SpaceX competes with ULA, Blue Origin, Rocket Lab, and Chinese launch providers. But in practice, the relevant question is cadence and cost, not logo count. SpaceX's 2025 record of roughly 165 orbital launches reinforces how far ahead it remains in operational tempo.

In satellite internet, the most serious strategic challenger is Amazon Leo. Amazon has the balance sheet, cloud ecosystem, and enterprise relationships to matter, but as of early April 2026 it was still only at 241 deployed satellites, versus Starlink's much larger installed base.

In defense and national security, SpaceX increasingly intersects with Lockheed Martin, Northrop Grumman, and L3Harris, especially as launch, secure communications, missile warning, and space transport architectures converge.

SpaceX's moat: reusable rocketry at industrial scale. In aerospace, being five years ahead is not a lead. It is a strategic era.

8. Risk Analysis: Four Scenarios

Scenario 1: Starlink growth slows — Probability: 25%

This is the most important bear case because Starlink likely carries the valuation. Risks include competitive pricing pressure, saturation in early adopter geographies, lower blended ARPU, and the capital burden of replenishing the constellation.

Scenario 2: Starship disappoints or is delayed — Probability: 20%

Starship is still more option than earnings stream. If commercialization slips materially, a large portion of the future platform premium evaporates.

Scenario 3: Musk risk — Probability: 15%

The key-man dependency is obvious. Political controversies, distraction across multiple companies, or governance complications could hit sentiment even if the operating business remains sound.

Scenario 4: Regulation and geopolitics — Probability: 15%

Satellite congestion, orbital debris policy, national-security scrutiny, export controls, and great-power competition all matter here. The larger Starlink becomes, the less it will be treated as a consumer broadband novelty and the more it will be treated as a geopolitical asset.

9. IPO Mechanics

The deal is widely described as potentially raising up to $75B, with unusually high retail participation. The timing most often cited is mid-2026, though that can still move depending on SEC review and market conditions.

What to watch

- Retail allocation: if the reported record retail allocation survives into the final deal terms, this could become the largest mainstream public-market access event for individual investors in years

- Expected listing date: market reporting points to a possible June 2026 window, but still tentative

- Lock-up period: not yet public; investors should assume a standard post-IPO lock-up unless the prospectus says otherwise

Reference: large IPO aftermarket behavior

| IPO | First Day | 1 Month | 1 Year |

|---|---|---|---|

| Aramco | +10% | Mixed / below debut highs | Below early peak by year-end |

| Alibaba | +38% | Strong early follow-through | Positive in year one |

| +0.6% | Weak | Strong rebound by year one |

Should investors buy on day one? History gives a frustrating answer: only sometimes. Great companies and great IPOs are not the same thing. When first-day demand is driven by cultural intensity and benchmark flows, buyers can easily overpay even for exceptional businesses.

10. Historical Context

Mega IPOs tend to sort into two families.

The first family is the prestige deal priced for perfection — celebrated because it is huge and symbolic, but often struggling afterward because too much future success is already in the price. Aramco is the cleanest comparison.

The second family is the platform company that looks expensive but proves underpriced because the market still misunderstands the compounding engine. Google/Alphabet is the archetype. Investors who focused only on search advertising missed what became one of the most productive cash machines in modern corporate history.

Where does SpaceX fit? Today it looks more like a blend of both. It has the ceremonial prestige and political gravity of Aramco, but also the category-creating platform characteristics that once made Google hard to value with traditional comparables.

That is why the IPO will be so divisive. Bears will call it peak hype. Bulls will call it the public birth of a new industrial platform. Both sides will have evidence.

11. Brutal Edge Verdict + BEAF Score

BEAF Score (IPO-adapted — 6 factors, 10 points each, 60 max)

| Factor | Score (/10) | Comment |

|---|---|---|

| Business quality | 10 | World-class strategic asset |

| Addressable market | 10 | Connectivity, launch, defense, logistics |

| Advantage / moat | 10 | Reuse, cadence, vertical integration |

| Founder / leadership | 8 | Massive premium, real governance risk |

| Financial visibility | 5 | Still opaque until S-1 |

| Valuation discipline | 3 | At $1.75T, burden is enormous |

| **Total** | **46 / 60** | Elite business, difficult IPO price |

Brutal Edge verdict

SpaceX is almost certainly one of the best businesses ever to come public. That does not automatically make it one of the best-priced IPOs ever to buy.

If the final valuation settles materially below the high end of current reporting, the deal could still be attractive for long-term investors who want exposure to orbital infrastructure. If it prices near $1.75T with euphoric first-day demand, investors are effectively paying today for multiple businesses that do not yet fully exist at scale.

Editorial manufacturing insight

Rockets are not software. SpaceX deserves a premium because it mastered manufacturing where others managed complexity. But no premium is infinite.

The deepest truth about SpaceX is this: it is a manufacturing company disguised as a technology myth. Investors who understand throughput, reliability, supply chains, and iterative cost compression will understand why SpaceX is extraordinary. Those same investors should also understand why industrial execution is never linear, even for the best operator in the field.

Final call

- Business quality: Extraordinary

- Strategic importance: Extraordinary

- IPO attractiveness at $1.75T: Debatable

- Verdict: Buy the company, question the price

12. Sources and Methodology

Primary factual anchors used in this report

1. Major media reporting that SpaceX has confidentially filed for a 2026 IPO with a $1.5T to $1.75T valuation range and up to $75B raise.

2. Reporting that the deal may include an unusually large retail allocation.

3. Nasdaq reported 2026 Fast Entry rule change for large IPOs.

4. S&P official U.S. index methodology for size and eligibility framework.

5. Starlink 2025 progress reporting on 4.6M+ new active customers and 35 new markets.

6. Independent summaries indicating Starlink ended 2025 with 9M+ customers.

7. Amazon Leo / former Project Kuiper deployment progress as of April 2026.

8. NASA description of SpaceX role in Human Landing System missions.

9. Historical IPO debut references for Aramco, Alibaba, and Facebook.

Modeling notes: Segment revenues, revenue mix, ARPU ranges, 2026 to 2028 forecasts, SOTP values, and reverse-DCF scenarios are editorial estimates prepared for feature-reporting purposes. They are not company guidance. The reverse-DCF uses 12% WACC and 3% terminal growth. Because SpaceX has not yet published a public S-1, all valuation work should be treated as preliminary framework analysis.

About SPACEX

Share your analysis

Keep it data-driven. No investment advice.

- Keep it data-driven and respectful

- No investment advice (buy / sell / hold)

- No spam, promotion, or solicitation

- No profanity or offensive content

- Violations are automatically removed

Data: Financial Modeling Prep, Alpha Vantage, CoinGecko

NOT investment advice. Always do your own research.