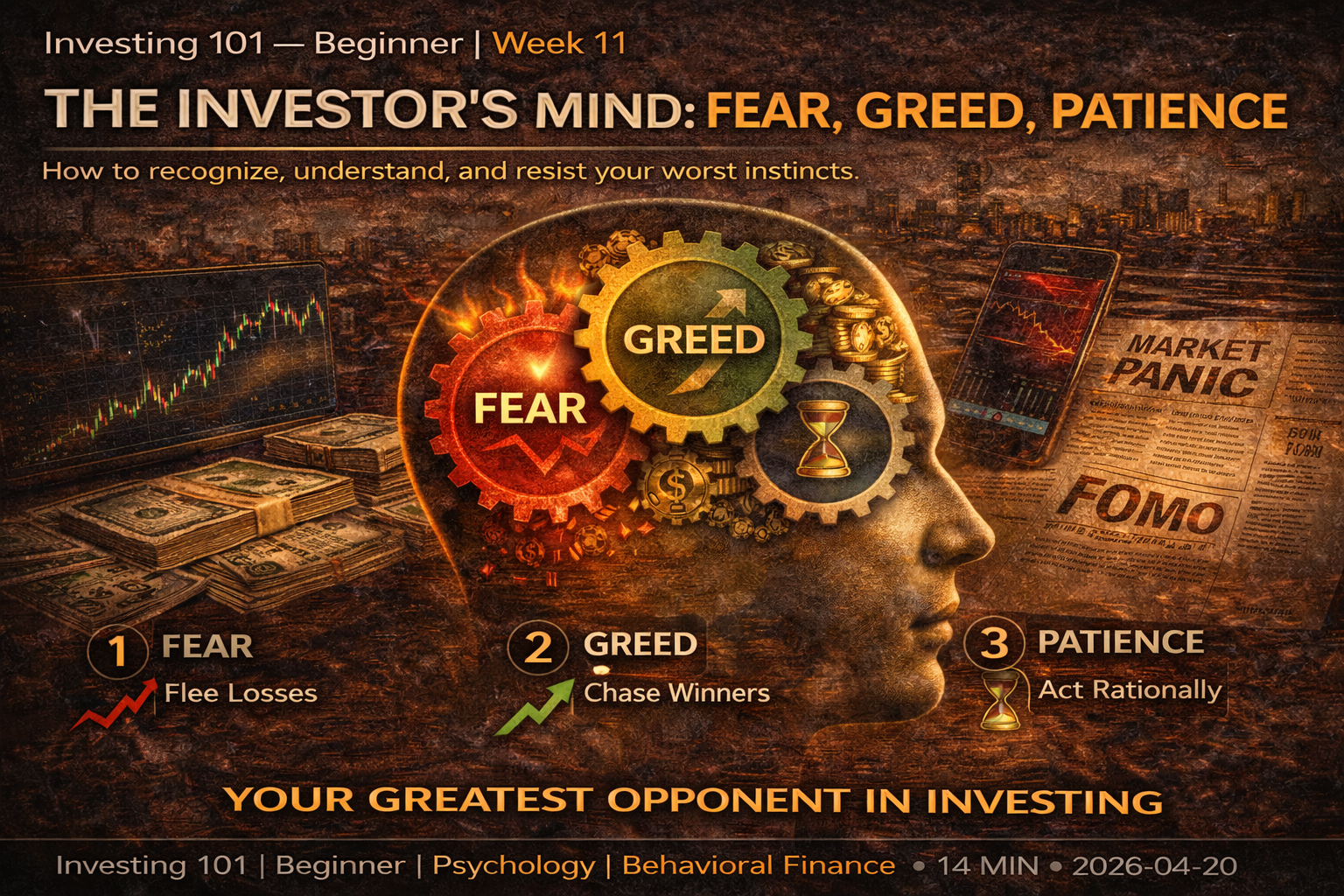

The Investor's Mind: Fear, Greed, Patience

You can know everything in this course and still lose money. The enemy is usually not the market — it is the investor's own mind. Here is what you are up against, and how to survive yourself.

The Investor's Mind: Fear, Greed, Patience

Ten weeks of this course have been about skills. How to read a balance sheet. How to analyze a business. How to value a stock. How to build a portfolio. These are real skills, and they matter.

This week is different.

This week we talk about the thing that ruins more retail investor returns than any lack of knowledge, any bad stock pick, any mistaken valuation. The enemy is almost always the investor themselves — specifically, the investor's own mind, acting under pressure, in the presence of money, in the presence of news, in the presence of other people making and losing fortunes.

The research on this is unambiguous. Study after study shows that retail investors earn significantly lower returns than the very funds they invest in. The gap — sometimes called the "behavior gap" — is the cost of bad timing decisions. People buy into funds after they have risen. People sell out of funds after they have fallen. They do this predictably, repeatedly, across generations and markets and asset classes. The skills do not save them, because the moment the skills are needed most, the skills are overridden by emotion.

This is not a character flaw. It is a feature of how human brains work, and it requires deliberate effort to overcome. This week we name the patterns, understand their origins, and set up the mental frameworks that let you operate calmly in conditions that make most people panic.

The Two Masters: Fear and Greed

Every investing mistake beginners make can be traced to one of two emotional states. The experience of being in the market is, functionally, a constant oscillation between them.

Greed is the feeling when markets are rising and other people seem to be making money easily. Your friend mentions a stock that doubled. A headline claims a new technology will "change everything." The stock you were watching keeps going up without you. Every day you are not in, the gains seem to accelerate. You feel left behind. You feel stupid for not having acted. Eventually, if greed wins, you buy — not based on a careful analysis of what the thing is worth, but based on the painful feeling of watching others profit while you stay on the sidelines.

Fear is the feeling when markets are falling and losses are mounting. The news runs constant coverage of the crisis. Your portfolio value drops by thousands, then tens of thousands. Every day the losses compound. You read articles arguing that the worst is still ahead. You feel stupid for having bought when you did. You feel the weight of possibly losing even more. Eventually, if fear wins, you sell — not based on a careful analysis of whether the underlying businesses have actually deteriorated, but based on the painful feeling of watching your net worth shrink.

Greed buys near tops. Fear sells near bottoms. This single pattern — baked deep into human psychology, repeated across every market cycle in history — is the reason retail investors as a group systematically underperform the assets they invest in. The money is transferred, not through any malicious mechanism, but through the simple behavioral inevitability of people buying what has already gone up and selling what has already gone down.

Knowing about this pattern does not automatically protect you from it. In the moment, greed does not feel like greed — it feels like obvious opportunity that you would be foolish to miss. Fear does not feel like fear — it feels like rational recognition of a deteriorating situation that you would be foolish to ignore. The emotions dress themselves up as logic. That is what makes them dangerous.

Why Your Brain Works This Way

The emotional patterns you are fighting are not random quirks. They are evolved responses that served human survival for most of our species' history — and they happen to misfire badly when applied to financial markets.

Loss aversion. Humans feel losses roughly twice as intensely as they feel equivalent gains. Losing $1,000 hurts about twice as much as gaining $1,000 feels good. This made sense in a world where losing a week's food could mean starvation while gaining an extra week's food was merely comfortable. It makes much less sense in a world where paper losses and gains in a brokerage account are temporary fluctuations in values that will almost certainly recover. Loss aversion is why people sell at bottoms — the pain of continued losses feels more threatening than it actually is.

Herd behavior. For most of human history, being part of a group was the difference between survival and death. Your ancestors who noticed everyone else running from something and ran too without asking questions survived more often than the ones who hung around to analyze the situation. This instinct is still live. When everyone around you is buying, the pull to buy is powerful. When everyone is selling, the pull to sell is powerful. The instinct that saved your ancestors from predators now pulls you into market bubbles and crashes.

Recency bias. Recent events feel disproportionately important compared to older ones. If the market has been rising for two years, you begin to feel that rising markets are normal and will continue. If the market has been falling for six months, you begin to feel that falling markets will continue indefinitely. Neither is a logical conclusion from the available evidence — it is simply how human memory weights experiences.

Confirmation bias. Once you form a view, you preferentially notice information that confirms it and discount information that contradicts it. If you believe a stock you own is going to the moon, you will find yourself reading bullish articles and ignoring bearish ones, not because you are being dishonest but because it is how human attention naturally works.

Anchoring. The first piece of information you receive about something disproportionately shapes your view of it. If you bought a stock at $50 and it is now $30, your "anchor" is $50, and the $30 price feels like a loss that must be recovered. The actual value of the business has nothing to do with where you happened to buy. But your brain does not process it that way.

These patterns are universal. They affect professionals as well as amateurs. They affect people with high IQs just as much as people with average ones. The difference between good investors and bad ones is not that good investors have escaped these biases — it is that good investors have built practices and structures that limit how much damage the biases can do.

The Patience Problem

Set aside fear and greed for a moment. Here is a quieter psychological failure that hurts beginners almost as much: impatience.

The math of compounding rewards patience unusually heavily. A dollar invested at 10% annual returns becomes $1.10 after one year, $1.61 after five years, $2.59 after ten years, $6.73 after twenty years, and $17.45 after thirty years. The first decade produces less growth than the last one does. The vast majority of the total wealth-creation happens in the later years, after decades of modest-looking growth have compounded into something substantial.

This is a problem for most beginners because most people do not have the temperament to sit through a decade of modest-looking results waiting for the compounding to kick in. They want to see meaningful progress in a year or two. When they do not, they conclude that investing is not working and look for something more exciting. They switch strategies. They try to pick better stocks. They leverage up. They move to options or crypto. Each move, on average, hurts them.

The investors who do extraordinarily well over long periods are almost always the ones who found a reasonable strategy early, stuck with it through decades of unexciting-looking progress, and let the math do its work. They do not look like geniuses year to year. They look like geniuses at age 70, when the compounding they have been patiently absorbing for forty years has produced something extraordinary.

This is not a motivational point. It is a structural fact about the mathematics of compound growth. And it is the single hardest thing for a beginner to accept emotionally, because "be patient for thirty years" does not feel like advice — it feels like non-action. It is action, of a specific and difficult kind. The action is the discipline to not react, to not tinker, to not chase, to not panic. Most people cannot sustain it. The ones who can, win.

Time Horizon and Emotional Bandwidth

Here is a practical framework that helps enormously: match your emotional bandwidth to your time horizon, not to market movements.

If you are investing money you will not need for ten or twenty years, market movements over the next six months are irrelevant. Literally irrelevant. Whether the market goes up 20% or down 20% between now and the end of the year has no bearing on whether you meet your long-term goal, because that goal is a decade or more away, and in the meantime the market will go up and down many times.

Knowing this intellectually and feeling it emotionally are different. Most beginners check their portfolios constantly. Every price move registers as a little emotional event. A bad day feels like a setback. A good day feels like progress. But none of it is setback or progress when your horizon is measured in decades — it is just noise, and absorbing each moment of noise as an emotional event slowly wears down the discipline needed to hold through the genuinely difficult stretches.

The practical implication: reduce how often you check. Daily is too often. Weekly is too often for most people. Monthly is probably enough. Quarterly is fine. If you are invested in quality businesses with long-term tailwinds, you do not need to monitor prices daily to ensure nothing has gone catastrophically wrong. A few times a year of honest review is more than sufficient.

Professional investors often check prices throughout the day because their jobs require it. Their jobs also require managing the emotional cost of that constant exposure, which many of them handle poorly. As an individual investor with no obligation to watch the market minute by minute, you have a structural advantage. Use it. Do not voluntarily subject yourself to emotional inputs you do not need.

The News Problem

The financial news media exists to capture attention. This is not a moral failing of individual journalists — it is the economic model of the industry. Content that makes you feel calm and patient does not get clicks. Content that makes you feel anxious, excited, or outraged does.

This has predictable consequences for how financial news is written. Dramatic language. Constant crisis framing. Extreme predictions, especially extreme bearish ones. Stories about individual people who made or lost fortunes. Daily micro-analysis of movements that, at any reasonable time horizon, are noise.

None of this is information, in the useful sense. Most of it is entertainment dressed in business clothing. And it actively damages long-term investor performance because it repeatedly triggers the emotional responses we are trying to manage.

A reasonable discipline for beginners: do not consume daily financial news. Read longer-form analysis on a weekly or monthly cadence, when you are in a calm state and can process it carefully. Avoid financial Twitter during market stress, because it specifically amplifies both greed and fear through its recommendation algorithms. Ignore the headlines on finance sites that are designed to pull you into taking action.

This sounds harsh. In practice, stepping back from daily news consumption is one of the best things a retail investor can do for their returns. The information you need to run a long-term portfolio is quarterly earnings reports and occasional major news. Everything else is optional, and most of it is harmful.

What Discipline Actually Looks Like

When we say "investor discipline," we do not mean willpower. Willpower runs out. The investor who is relying on willpower to not panic-sell in a bear market is almost certainly going to panic-sell eventually, because everyone runs out of willpower at some point, usually at the worst possible time.

Discipline in investing is really about structure — setting up rules and systems that protect you from yourself when your judgment is compromised, so that willpower is not the last line of defense.

Have a written investment thesis for each holding. Before you buy, write down why you are buying, what you expect the business to do over the next five years, and what would cause you to sell. When the stock is down 40% and you are tempted to panic-sell, you can pull out the document and ask: has any of this actually changed? If nothing has changed except the price, the reason to sell is not based on any fundamental fact. It is based on the feeling of losing money, which is not a reason.

Have a fixed contribution schedule. Put money into the market on a regular schedule — weekly, monthly, whatever fits your cash flow — regardless of what the market is doing. This removes the decision from your hands. You are not trying to time anything. You are not trying to wait for the right moment. You are just contributing, mechanically, on the schedule you set in advance.

Have rules for when to check and when not to. Decide, in advance, how often you will review your portfolio. Stick to the schedule. Do not check in response to news. The market could be crashing — especially do not check in response to news. The schedule exists precisely so that you do not make decisions in the presence of emotional inputs.

Accept that you will make mistakes. You will. Every investor does. The goal is not to avoid all mistakes — it is to avoid mistakes big enough to ruin you, and to learn from the ones that do happen. A single stock going to zero, if it was 5% of your portfolio, is a learning experience. A single stock going to zero, if it was 50% of your portfolio, is a disaster. The difference is not skill in picking stocks. The difference is position sizing and discipline.

Automate what you can. Automatic transfers to the brokerage. Automatic reinvestment of dividends. Automatic index fund purchases on a schedule. Each automation removes a decision point where emotion could intrude. The less you have to decide in the moment, the better.

The Uncomfortable Truth About Temperament

Warren Buffett has said that investing does not require extraordinary intellect — an IQ of 125 is plenty, and beyond that, additional brainpower is largely wasted. What it does require, he says, is temperament: the ability to stay calm when everyone else is panicking, to avoid buying into mania, to hold quality businesses for decades without getting bored or cute.

This is not a comforting message for beginners, because temperament is not something you can study for. You cannot take a course on it. You cannot read your way into it. It is developed, if at all, through the repeated experience of making decisions under stress and — painfully — learning from the ones that go wrong.

What you can do is build the structures described above, which limit how much your temperament has to carry. And you can be honest about your own emotional tendencies. Some people are, by nature, calmer around money than others. If you know you are the kind of person who panics during market drops, build your portfolio and your routines around that fact. Use index funds instead of individual stocks so there is less temptation to second-guess individual positions. Use a contribution schedule so you do not have to make discretionary decisions. Keep a meaningful cash reserve so that a market drop does not coincide with needing to raise cash.

You can work with your temperament. You cannot easily override it. Accept who you are, and design your investing life to fit.

The Long Game

The investors who build real wealth over long periods share a small number of characteristics, and none of them is "picked the best stocks."

They started early. They saved consistently. They stayed invested through multiple market cycles. They avoided catastrophic mistakes. They let time and compounding do the heavy lifting. They did not try to be heroes. They did not chase the hot strategy of the moment. They held durable businesses or broad index funds and — this is the important part — they stayed the course when the course was uncomfortable.

The course will be uncomfortable. There will be 30% drawdowns. There will be years when your portfolio goes nowhere. There will be periods when everyone around you seems to be getting rich on something you are not in. There will be moments when selling everything and waiting for clarity feels like the only sensible option.

Your job is to not sell. Your job is to keep buying on schedule. Your job is to keep reading quarterly reports of the businesses you own. Your job is to not check prices on your phone during meals or in bed. Your job is to trust the process you built when you were calm, at the moments when you are not calm.

This sounds simple. It is not easy. The gap between the two is where most retail investor returns are lost.

What You Should Do This Week

Write one investment thesis. Pick a stock you own or are considering buying. Write down, on paper or in a document you can retrieve: (a) why you believe this is a good business, (b) what you expect it to look like in five years, and (c) what specific events or data would cause you to change your mind and sell. Keep this document. When the stock is down someday, read it.

Audit your news consumption. For the next few days, track how often you look at financial news, social media, or stock prices. Be honest. Most people are shocked at how often they check. Then decide: what is the minimum frequency that actually serves you? Commit to that frequency for the next month.

Set up at least one automation. An automatic monthly transfer into your brokerage. An automatic purchase of an index fund. Dividend reinvestment, if you have dividend-paying holdings. Pick one automation and set it up this week. This is the kind of decision that pays compounding dividends for decades.

Identify your emotional tendency. Are you more likely to be pulled into mania during bull markets, or to panic during bear markets? (Most people are one or the other more strongly than they realize.) Knowing your dominant failure mode helps you build specific defenses against it.

Looking Ahead

Next week is the last week of the Beginner Series, and it is the one that brings everything together. We move from theory to execution — the concrete path from where you are now to where a well-run portfolio lives after five years of consistent practice. What to do in month one. What to do in year one. What to do in year five. A realistic roadmap for a beginner to become a competent long-term investor.

Investing 101 — Beginner Series. Week 11 of 12.

Next week: Your First 5 Years — A Realistic Roadmap.

Educational content only. Not investment advice. Always do your own research.