NVIDIA Ising: Why the Quantum Control Plane Matters More Than the Qubits

NVIDIA Just Launched the Operating System for Quantum Computers. Ising attacks the hardest practical problem in quantum — calibration and error correction. This is CUDA for quantum, launched before the era has fully arrived. Not a 2026 earnings catalyst. A decade-long moat extension.

⚡ SPECIAL REPORT — BRUTAL EDGE™ VERDICT

Ising matters because it attacks the hardest practical problem in quantum computing — calibration and error correction — not because quantum is suddenly commercial. NVIDIA is not trying to build qubits. It is trying to own the software layer that makes qubits usable. This is CUDA for quantum, launched before the era has fully arrived. Not a 2026 earnings catalyst. A decade-long moat extension.

The Move

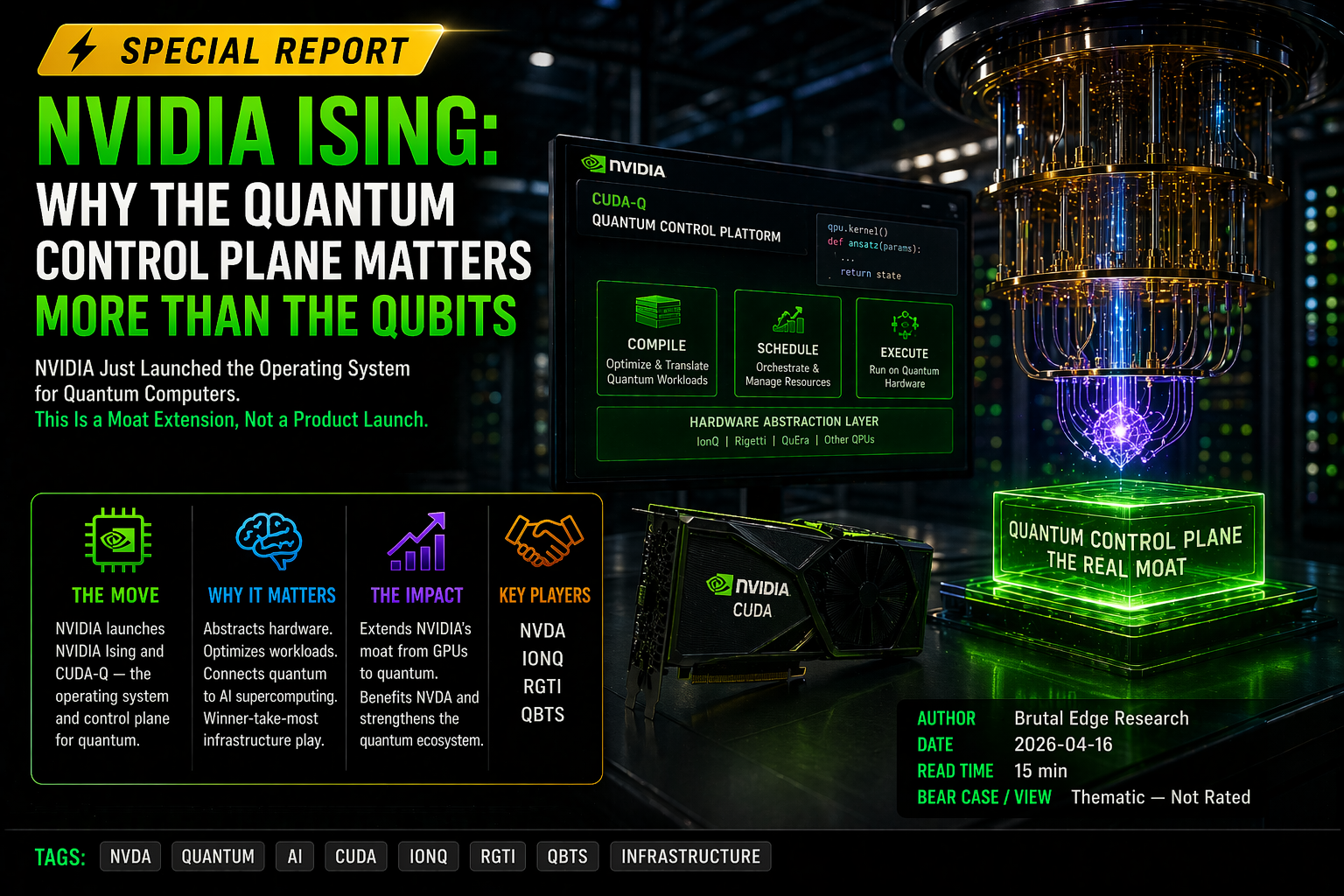

On April 14, 2026, NVIDIA announced Ising — "the world's first open AI models to accelerate the path to useful quantum computers." Jensen Huang framed it in one sentence that matters more than any benchmark: "AI becomes the control plane — the operating system of quantum machines."

That is not a product statement. It is a platform statement.

Ising consists of two core components:

Ising Calibration: A vision-language model that interprets measurements from quantum processors and automates continuous calibration. NVIDIA claims it reduces calibration time from days to hours.

Ising Decoding: Two 3D convolutional neural networks optimized for real-time quantum error-correction decoding. NVIDIA claims performance up to 2.5x faster and 3x more accurate than pyMatching, the current open-source industry standard.

Both are open-source. Both integrate with CUDA-Q and NVQLink, NVIDIA's QPU-GPU interconnect. Both are designed to sit above quantum hardware regardless of which qubit architecture wins the underlying race.

The Real Bottleneck

Most retail narratives around quantum computing still focus on qubit counts. Investors should reframe.

The industry's real bottleneck is not adding more qubits. It is keeping them stable, calibrated, and error-corrected long enough to do useful work. A quantum chip with impressive lab specs but weak calibration and error management is not a commercial machine. It is a research instrument.

NVIDIA's own announcement makes this explicit: "significant breakthroughs are needed in quantum processor calibration and quantum error correction" to achieve useful applications at scale. AI is the key to turning today's processors into "large-scale, reliable computers."

This is the economic unlock. If calibration and decoding improve meaningfully, the path from laboratory hardware to commercially relevant systems becomes shorter. And the companies that control that software layer capture disproportionate value — regardless of which qubit architecture ultimately dominates.

Current quantum hardware is fragmented across trapped ions, superconducting qubits, neutral atoms, photonics, and annealing approaches. NVIDIA is not betting on any one of them. It is betting on the layer above all of them.

NVIDIA's Strategy: Own the Brains, Not the Qubits

The smartest part of this move is what NVIDIA is not doing. It is not trying to outbuild IonQ, IQM, or Infleqtion at the qubit level. It is doing what it has done for twenty years: build the software, tooling, and accelerated-computing layer that everyone else needs.

The CUDA parallel is exact.

CUDA was not just a toolkit. It was a lock-in mechanism disguised as developer enablement. Developers who built on CUDA stayed on CUDA. When AI demand arrived in 2022, NVIDIA did not have to compete for the software ecosystem — it already owned it.

Ising follows the same playbook. If Ising and CUDA-Q become the default environment for quantum-classical workflows, NVIDIA ends up owning the most valuable layer in the quantum stack without manufacturing a single quantum processor.

The strategic question Ising answers is the one investors should be asking about NVIDIA: How does NVIDIA keep expanding its moat once GPUs themselves become more contested?

The answer: move up the stack, then sideways into adjacent stacks, before rivals do. AI factories. Now quantum control planes. Next, whatever comes after that.

The Ecosystem Signal

The adoption list matters more than the marketing copy.

Ising Calibration early adopters: Atom Computing, Academia Sinica, EeroQ, Conductor Quantum, Fermilab, Harvard SEAS, Infleqtion, IonQ, IQM, Lawrence Berkeley National Laboratory's Advanced Quantum Testbed, Q-CTRL, UK National Physical Laboratory.

Ising Decoding early adopters: Cornell University, Infleqtion, IQM, Sandia National Laboratories, SEEQC, UC San Diego, UC Santa Barbara, University of Chicago, USC, Yonsei University.

Three signals to extract:

1. Multi-modality engagement. NVIDIA is not locking itself to a single qubit type. It is partnering across ion traps, superconducting, neutral atoms, and photonic approaches simultaneously.

2. Commercial + government traction. Hardware startups plus national labs plus top universities. This is how standards get set — not through press releases, but through embedded workflows at institutions that define the field.

3. International reach. US, UK, Taiwan, South Korea, EU representation. NVIDIA is positioning Ising as the global default, not a US-only standard.

Standards do not emerge from who has the best marketing. They emerge from who becomes indispensable in real workflows. NVIDIA is executing that playbook with speed.

NVIDIA Key Metrics

| Metric | Value |

|---|---|

| Stock Price (Apr 16) | ~$198.87 |

| Market Cap | ~$4.53T |

| FY2026 Revenue | $215.9B |

| FY2026 Gross Margin | 71.1% |

| CUDA Developers | 6M+ |

| CUDA Applications | 6,000+ |

| Quantum Market Size (2030 est.) | $11B+ |

Ising does not change 2026 earnings. The quantum market is still too small to move NVIDIA's top line materially in the near term. That is not the investment point.

What It Means for NVIDIA Stock

Short term: minimal earnings impact.

NVIDIA remains priced primarily on AI infrastructure demand, Blackwell/Rubin execution, hyperscaler capex, and data center margins. Quantum software will not add meaningful revenue in 2026 or 2027.

Long term: moat reinforcement.

NVIDIA's premium valuation does not come only from current revenue. It comes from the belief that the company can repeatedly capture the next adjacent compute layer. Ising supports that narrative directly.

The market rewards platform expansion more than single-product dominance. Companies that extend their moat into adjacent categories sustain premium multiples longer than companies that defend a single category. Apple did this with services. Microsoft did this with Azure. NVIDIA is attempting to do this with AI factories and now quantum orchestration.

If Ising gains real adoption, it reinforces the thesis that NVIDIA is the default systems company for advanced compute — not just the dominant GPU vendor. That distinction is worth multiple points of sustained P/E ratio over time.

Concrete implication: Ising is not a reason to buy NVIDIA today. It is a reason to stay long NVIDIA through valuation compressions. The moat keeps widening.

What It Means for Quantum Stocks

Quantum equities rallied after the Ising announcement.

| Ticker | Company | Recent Price |

|---|---|---|

| IONQ | IonQ | ~$43.25 |

| RGTI | Rigetti Computing | ~$19.11 |

| QBTS | D-Wave Quantum | ~$20.81 |

The rally logic is reasonable. If Ising reduces the pain of calibration and error correction, quantum hardware companies move one step closer to commercial deployment. This is a de-risking event for the sector narrative.

But investors should be careful about the translation.

Ising does not solve the economics of quantum hardware businesses. It improves one critical bottleneck. It does not eliminate capital intensity, low current revenue and negative margins, execution risk, competition between qubit architectures, or timeline uncertainty for commercial applications.

The correct reading is not "all quantum stocks are now cheap." It is: the software and control-plane layer around quantum just got stronger, which raises the value of viable hardware platforms over time.

IonQ at a 60x+ revenue multiple is still priced for a future that hasn't arrived. Rigetti and D-Wave face the same valuation challenge. Ising helps. It does not transform the economics.

Sector-wide thesis: Ising is a tailwind. It is not a rescue.

The Risk Stack

1. Benchmark claims are company-stated.

The 2.5x speed and 3x accuracy improvements are NVIDIA's own benchmarks, not yet independently validated across all qubit architectures and real-world workloads. Actual performance gains may vary significantly by platform and implementation.

2. Long-duration market with small near-term revenue.

NVIDIA cites a quantum market expected to surpass $11 billion in 2030. That is strategically meaningful but tiny compared to NVIDIA's current $215B+ annual revenue base. Near-term financial contribution will be narrative-enhancing, not revenue-moving.

3. Open-source doesn't guarantee monetization.

Open-source ecosystem adoption does not automatically translate into revenue. Sometimes it builds standards and moat. Sometimes it builds goodwill without monetization. The bullish case depends on Ising deepening NVIDIA's role across CUDA-Q, NVQLink, and hybrid system orchestration — not merely GitHub download counts.

4. Competing frameworks emerging.

IBM Qiskit, Google Cirq, Microsoft Q#, and Amazon Braket all have their own quantum software frameworks. Ising enters a competitive landscape where NVIDIA has scale advantages but not incumbency.

Bottom Line

NVIDIA Ising is important because it attacks the hardest practical problem in quantum computing, not because it proves quantum is suddenly commercial.

The right investor framing is three-layered:

For NVIDIA: Ising is a strategic moat extension into quantum control software and hybrid compute orchestration. Long-duration catalyst, not quarterly driver.

For quantum hardware companies: Ising is a credible ecosystem tailwind. It does not resolve valuation concerns or capital intensity, but it shortens the timeline to commercial relevance.

For the broader market: Ising is an early signal that the next battle in compute is not about more hardware. It is about who controls the intelligence layer that makes advanced hardware usable.

If CUDA made NVIDIA indispensable to modern AI, Ising is NVIDIA's attempt to make itself indispensable to the future of quantum-classical computing. The playbook is identical. The timing is earlier.

That is why this announcement matters. Not as a curiosity from World Quantum Day, but as a deliberate move by NVIDIA to own another control point in the next computing era.

The qubits are fragmented. The control plane is consolidating.

About NVDA

Share your analysis

Keep it data-driven. No investment advice.

- Keep it data-driven and respectful

- No investment advice (buy / sell / hold)

- No spam, promotion, or solicitation

- No profanity or offensive content

- Violations are automatically removed

Data: Financial Modeling Prep, Alpha Vantage, CoinGecko

NOT investment advice. Always do your own research.