Quantum Sector Special Report: Not Commercialization Complete — An Investable Early-Stage Industry

Six quantum stocks now trade on US markets. IonQ, Rigetti, D-Wave, Infleqtion, Xanadu, Horizon Quantum — multiples from 64x to 1,277x EV/Revenue. The sector is not a bubble, but most stocks price it like one. Our verdict: one name, one thesis, one sector call.

The quantum sector in 2026 stands at a precise inflection: technology validation is accelerating, government and enterprise budgets are opening, and the public market now offers six distinct ways to invest. The question is not whether quantum is real. It is whether the stocks priced for quantum's future leave any return on the table for investors who buy today.

1. Executive Summary

The quantum sector in 2026 is entering its strongest year technologically. McKinsey reported that quantum technology startup funding reached approximately $2.0 billion in 2024, up roughly 50% year-over-year, with public funding announcements exceeding $10 billion in early 2025 led by Japan and Spain. Simultaneously, the industry's focus has shifted from simple "how many qubits" to error rates, error correction, hybrid HPC/GPU integration, and real-world applicability.

The technical progress is real. IBM is targeting its first scientific quantum advantage demonstration combined with classical HPC in 2026, maintaining its fault-tolerant system roadmap for 2029. Google's Willow demonstrated error correction improvements where errors decrease exponentially as qubits increase. Microsoft presented a topological qubit commercialization path through Majorana 1. NVIDIA unveiled NVQLink, binding QPUs and GPUs with low-latency infrastructure — treating quantum not as a standalone device but as part of a hybrid computing stack.

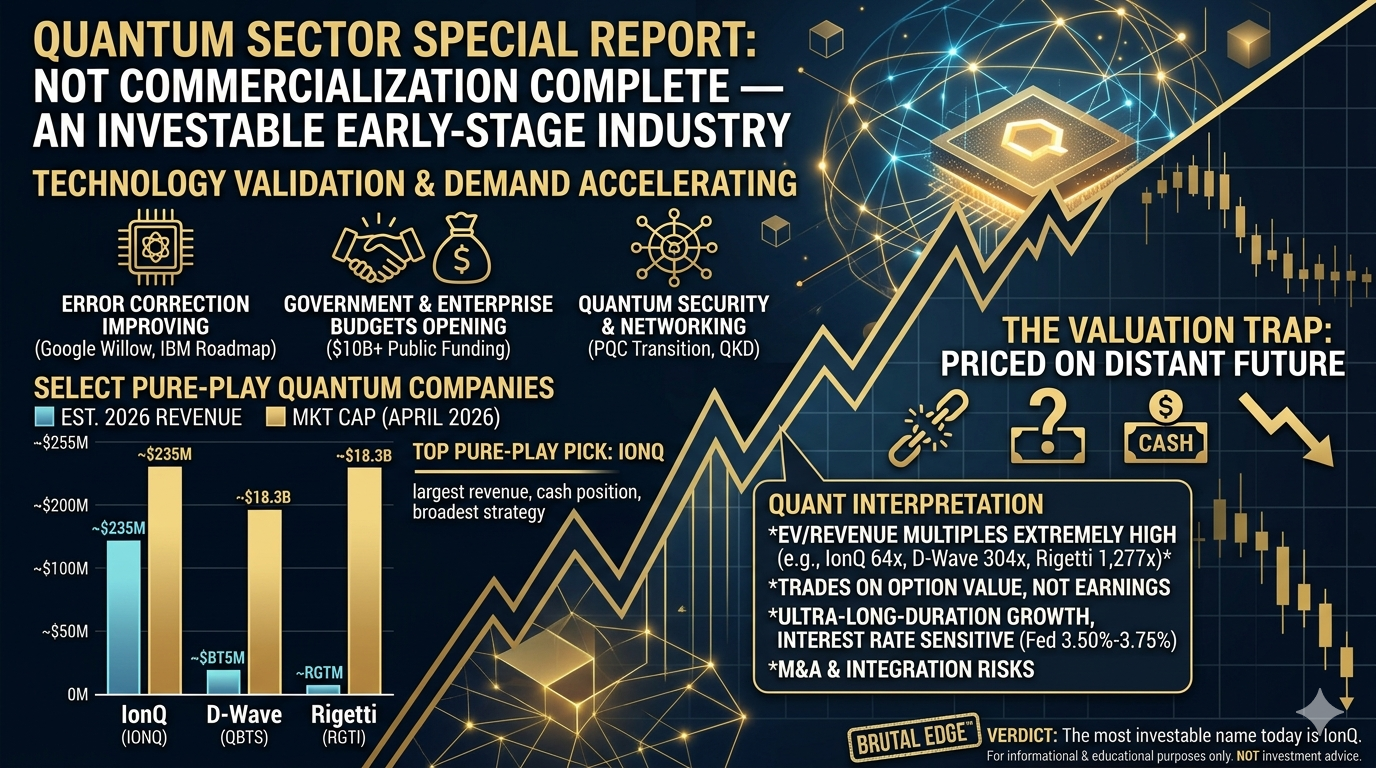

But the stock market must remain sober. Most publicly traded quantum stocks trade on long-term option value rather than revenue. IonQ's market cap is approximately $18.3 billion against 2026 revenue guidance midpoint of $235 million. D-Wave sits at roughly $8.37 billion market cap with 2025 revenue of $24.6 million. Rigetti is at approximately $9.66 billion market cap with 2025 revenue of $7.1 million. Rough EV/revenue multiples work out to approximately 64x for IonQ, 304x for D-Wave, and 1,277x for Rigetti — meaning the entire sector still trades on future technology platform premiums, not earnings.

My conclusion upfront: the quantum sector is not a bubble — it is an early-stage industry. But within it, you must distinguish between "where money arrives first" and "what is still too far in the future." By that standard, the current top pure-play quantum pick is IonQ, and the sector's key investment thesis is moving faster toward quantum networking, security, national infrastructure, and hybrid computing than toward quantum computing itself.

2. Why Look at the Quantum Sector Now

The reason to focus on quantum now is not "commercialization has finally arrived" — it is that the quality of technical validation has changed and the nature of capital has shifted. McKinsey estimated combined quantum computing company revenues at approximately $650-750 million in 2024, with the possibility of exceeding $1 billion in 2025. Still small, but it signals the industry is transitioning from pure research to early-revenue status.

The other shift is in funding sources. Where venture capital once dominated, governments, defense agencies, national research institutions, and major cloud providers now matter far more. IBM's roadmap, NVIDIA's NVQLink, and Amazon Braket's multi-modality approach all point in the same direction: quantum is no longer "a lab experiment" — it is becoming part of national strategic technology and data center infrastructure.

Security is moving faster than most realize. NIST finalized its first post-quantum cryptography (PQC) standards in 2024 and stated firmly that "now is the time to begin the transition." Google researchers also warned that future quantum attacks could break elliptic curve cryptography with fewer resources than previously expected. The key investment point: security budgets open before fault-tolerant universal quantum computers arrive.

3. Recent Technical Progress: What Constitutes Real Advancement

The core of recent technical progress comes down to three things. First, error correction is now producing data, not just promises. Google Willow demonstrated a regime where errors decrease as qubits increase — partially overcoming the long-standing problem of "error correction gets worse as it scales." IBM is also presenting modular fault-tolerance directions through Nighthawk and Kookaburra in 2026, maintaining its 2029 target.

Second, hardware diversity persists. The competition currently spans trapped ion, superconducting, neutral atom, photonic, annealing, and topological approaches simultaneously. The fact that Amazon Braket hosts multiple modalities on a single platform itself signals that the industry has not yet converged on one technology. For investors, this is both opportunity and trap — multiples remain open because no winner is confirmed, but the risk of being locked into the wrong modality is equally real.

Third, quantum is moving from standalone devices to hybrid infrastructure. NVIDIA's NVQLink was announced supporting 17 QPU builders, 5 controller companies, and 9 US national laboratories — demonstrating that quantum computing may deliver real value faster when combined with GPU/HPC. Most financial, materials, defense, and optimization problems will likely be commercialized first as classical-quantum hybrids, not "100% pure quantum."

4. Macro Environment and Geopolitics: Why Quantum Stocks Move Like Long-Duration Growth

From a macro perspective, quantum stocks remain interest-rate-sensitive ultra-long-duration growth plays. The Fed's policy rate stands at 3.50%-3.75% as of March 2026, with the next FOMC on April 28-29. In this environment, stocks that depend on distant future narratives rather than current earnings face the greatest valuation pressure. Since most pure-play quantum stocks still trade on technology expectations rather than profits, deteriorating rate and liquidity conditions could shake the entire sector.

Conversely, geopolitics is a paradoxical ally for the quantum sector. Budgets for quantum security, sovereign on-premise systems, defense optimization, and satellite-based secure communications can accelerate as geopolitical tensions rise. IonQ's European QKD network deployment, its listing on the Missile Defense Agency's SHIELD IDIQ, and D-Wave's promotion of missile defense simulation results with Davidson/Anduril all share this context. Interest rates are the enemy of valuation, but geopolitics is a tailwind for demand.

5. The Public Market Landscape: Recently Listed Quantum Stocks

Recent public market entries have favored SPAC/business combination listings over traditional IPOs. Prices are as of April 10, 2026 close.

Publicly Traded Quantum Companies

| Company | Ticker | Technology | Status | Notes |

|---|---|---|---|---|

| IonQ | IONQ | Trapped-ion + networking/security | Listed | Pure-play quantum bellwether |

| Rigetti | RGTI | Superconducting | Listed | High-beta hardware turnaround |

| D-Wave | QBTS | Annealing + gate-model | Listed | Optimization/defense early revenue |

| Infleqtion | INFQ | Neutral atom + sensing | Listed Feb 2026 | First public neutral-atom quantum |

| Xanadu | XNDU | Photonic + PennyLane | Listed Mar 2026 | Photonic fault-tolerance story |

| Horizon Quantum | HQ | Software infrastructure | Listed Mar 2026 | Software/OS layer, not hardware |

Stock prices: IONQ $28.79, RGTI $14.68, QBTS $14.25, INFQ $12.59, XNDU $8.96, HQ $8.86. As of April 10, 2026.

Even grouped as "quantum stocks," these are effectively different industries. D-Wave pushes annealing-based optimization alongside gradual gate-model expansion. Xanadu bets on room-temperature photonics and the PennyLane ecosystem. Infleqtion covers neutral-atom computing plus sensing and timing. Horizon Quantum operates closer to a software layer.

The pipeline continues. Pasqal is pursuing a listing at approximately $2.0 billion pre-money in H2 2026. IQM targets a mid-year combination at roughly $1.8 billion pre-money. 2026 is shaping up to be a year where the number of publicly traded quantum names keeps growing.

6. Where Money Arrives Fastest: An Investment Lens

The most common investor mistake is viewing the entire quantum sector through the lens of "the universal quantum computer that will someday arrive." In reality, certain areas are generating early revenue.

First is quantum networking and security. The PQC transition has already begun, and QKD plus secure communications are aligned with national defense demand. IonQ's acquisitions of ID Quantique, Capella Space, and Skyloom target this position — and this represents a revenue opportunity far closer than fault-tolerant universal QC.

Second is hybrid optimization and industry-specific computation. Lloyds Bank's IBM use case and D-Wave's missile defense simulations prove that for certain workloads, enterprises are moving beyond pilot stage. From an investment perspective, "which narrow tasks generate revenue first" matters far more than "when does universal advantage arrive."

Third is sovereign on-premise systems. KISTI's 100-qubit IonQ Tempo system, Jülich's D-Wave Advantage system, and IQM/Pasqal deliveries to European public institutions show that quantum computing is not exclusively a cloud game. Like AI data centers, some quantum infrastructure will inevitably become nationally or institutionally owned.

7. IonQ Deep Dive: Why This Is the Name Investors Watch First

IonQ currently has the most "investable story" among publicly traded pure-play quantum stocks. 2025 revenue was $130.0 million, up 202% year-over-year, with 2026 guidance of $225-245 million. Year-end cash, equivalents, and investments totaled $3.3 billion. Over 60% of 2025 revenue came from commercial customers, with over 30% from international sales. While still unprofitable, IonQ is no longer "an experimental stock with almost no revenue." Among pure quantum plays, it is the first to look like it could grow into a platform business.

On the technology side, IonQ has consistently put up numbers the market wants to see. In October 2025, IonQ announced 99.99% two-qubit gate fidelity — a "four nines" milestone the company claims as a world first. In September, Tempo achieved AQ 64. A critical caveat: AQ is IonQ's proprietary benchmark and should not be directly compared to IBM's qubit counts or Rigetti's fidelity figures. The right investor stance is remembering both "IonQ's performance has improved" and "that metric is not an industry-standard unit."

IonQ's true differentiator is not hardware alone but business expansion. ID Quantique brings security and networking. Capella Space and Skyloom add satellite-based secure networking. The SkyWater acquisition pursuit targets US-based trusted foundry capabilities. IonQ's investment thesis is no longer "cloud trapped-ion computing company" — it is a full-stack strategy spanning quantum computing, networking, security, and manufacturing. Among public pure-play quantum stocks, it is the most ambitious and the most complex.

Execution has been solid. IonQ delivered a 100-qubit Tempo to KISTI, announced a 6th-generation 256-qubit chip-based system deployment at its Cambridge Innovation Center in March 2026, and in April, Horizon Quantum agreed to adopt one of IonQ's early 256-qubit systems. In Europe, IonQ announced a large-scale QKD network deployment. This trajectory shows IonQ moving from "roadmap company" to one capable of shipping on-premise systems and networking infrastructure.

8. IonQ Valuation and Quant Interpretation

IonQ's greatest strength is scale and cash; its greatest weakness is still valuation. With a market cap of approximately $18.3 billion, year-end cash of $3.3 billion, and 2026 revenue guidance midpoint of $235 million, the approximate EV/2026 revenue multiple is roughly 64x. In absolute terms, very expensive — but within the sector, it is actually "less expensive." D-Wave and Rigetti show far higher EV/revenue multiples on current revenue bases. The market pays IonQ a premium for the largest revenue, largest cash position, and broadest story.

IonQ vs. Peers: Revenue Multiple Comparison

| Company | Market Cap | 2025/2026E Revenue | EV/Revenue |

|---|---|---|---|

| IonQ | ~$18.3B | $235M (2026E) | ~64x |

| D-Wave | ~$8.37B | $24.6M (2025A) | ~304x |

| Rigetti | ~$9.66B | $7.1M (2025A) | ~1,277x |

Market cap and revenue as of April 2026. EV approximated as market cap minus net cash.

But there are traps. First, IonQ's forward roadmap is extremely aggressive — SkyWater materials reference 200,000-qubit QPUs enabling 8,000 logical qubits from 2028, which remain company targets rather than verified reality. Second, increasing M&A raises integration risk. Third, competition has intensified: IBM and Google on error correction, NVIDIA on infrastructure, Amazon on distribution, and Pasqal/Xanadu/Infleqtion as new public challengers with different modalities. IonQ leads, but does not dominate unchallenged.

My interpretation: IonQ is the highest-quality pure play in the quantum sector, but it is not "cheap and therefore good." This stock is priced on 2027-2030 platform value, not current earnings. Short-term, revenue guidance raises, major government/commercial contracts, on-premise system deliveries, and networking/security revenue visibility must continue to justify the multiple. If execution stumbles for even one or two quarters, premium compression can be swift.

9. 2026 Sector Outlook

The quantum sector is likely to split three ways this year. First, companies that demonstrate real bookings and revenue will survive. IonQ and D-Wave are relatively better positioned here. D-Wave reported 2025 revenue of $24.6 million, liquidity of $884.5 million, and bookings exceeding $32.8 million in early Q1 2026. At minimum, there are attempts to show "workloads where real money changes hands." Rigetti has also begun general availability of its 108-qubit Cepheus-1, though the numbers remain smaller.

Second, newly listed stocks are likely to see elevated volatility. Xanadu showed strong initial reactions at listing but quickly gave back some gains. Horizon Quantum and Infleqtion still carry more "thematic" than "fundamental" characteristics. In this phase, technological appeal and stock returns may not align. Good technology does not automatically mean good stock.

Third, the industry as a whole is gradually transforming from a "quantum computing sector" into a "quantum infrastructure sector." The 2026 winners are more likely to be companies with error rates, networking, security, hybrid connectivity, and national budget access — not simply the most qubits. By this standard, IonQ and infrastructure plays like IBM/NVIDIA hold relative advantages, while single-story pure hardware companies may face greater volatility.

10. Brutal Edge Verdict

The quantum sector is not yet "AI 2023." It is not generating massive earnings today, nor has any single company definitively set the standard. But dismissing it as "hype with nothing behind it" ignores the accelerating pace of technical progress and budget flows. The accurate description of the sector right now: technology is genuinely advancing, but stock prices are pulling that future forward too aggressively.

First, among pure-play quantum stocks, IonQ is the top pick. It has the largest revenue, largest cash position, and broadest business expansion potential. However, this assessment means "best pure play" — not "cheap."

Second, the most underappreciated opportunity in the sector is quantum security and networking. Budget allocation will likely arrive here before fault-tolerant universal computing.

Third, newly listed stocks are technologically fascinating but far riskier as investments. Xanadu, Infleqtion, and Horizon Quantum are all worth watching, but at this stage they are closer to "early options that have entered the public market" than "confirmed winners."

One sentence to close:

The quantum sector sits not between fraud and revolution, but between revolution and overvaluation. And on that boundary, the most investable name today is IonQ.

11. Sources & Methodology

This report was prepared as of April 14, 2026. Technology roadmaps and announcements sourced from IBM, Google, Microsoft, NVIDIA, and Amazon official publications. Startup funding and industry revenue estimates from McKinsey. Post-quantum cryptography standards from NIST. Stock prices from financial data providers as of April 10, 2026 close. Company financials from IonQ, D-Wave, and Rigetti earnings releases and SEC filings. Market cap data from financial data providers. New listing information from SEC filings and company announcements. Scenario analysis and investment assessments are author estimates.

For informational and educational purposes only. NOT investment advice. Always do your own research before making investment decisions.

About IONQ

Share your analysis

Keep it data-driven. No investment advice.

- Keep it data-driven and respectful

- No investment advice (buy / sell / hold)

- No spam, promotion, or solicitation

- No profanity or offensive content

- Violations are automatically removed

Data: Financial Modeling Prep, Alpha Vantage, CoinGecko

NOT investment advice. Always do your own research.