The CLARITY Act: Who Owns the Toll Roads When Crypto Gets Legal Roads

The U.S. Market-Structure Bill That Matters More Than Any ETF Approval. The Stablecoin Yield Fight Is 99% Resolved. Here's What Changes — and who captures the value when legal roads get built.

⚡ SPECIAL REPORT — BRUTAL EDGE™ VERDICT

The CLARITY Act is not a crypto bill. It is a market-access bill. It converts the U.S. digital-asset market from litigation-defined to law-defined. That is a structural shift larger than spot ETF approval, because it affects exchanges, brokers, custodians, stablecoin issuers, and the entire market plumbing — not just one or two assets. The stablecoin yield fight — the single biggest political bottleneck — is now 99% resolved. Banking Committee markup must happen by late April to stay on track for passage before August recess. If it advances, value accrues first to infrastructure, then to assets. Coinbase is the clearest listed beneficiary. Circle is the clearest stablecoin infrastructure play. XRP is a narrative trade, not an equity thesis.

What CLARITY Actually Does

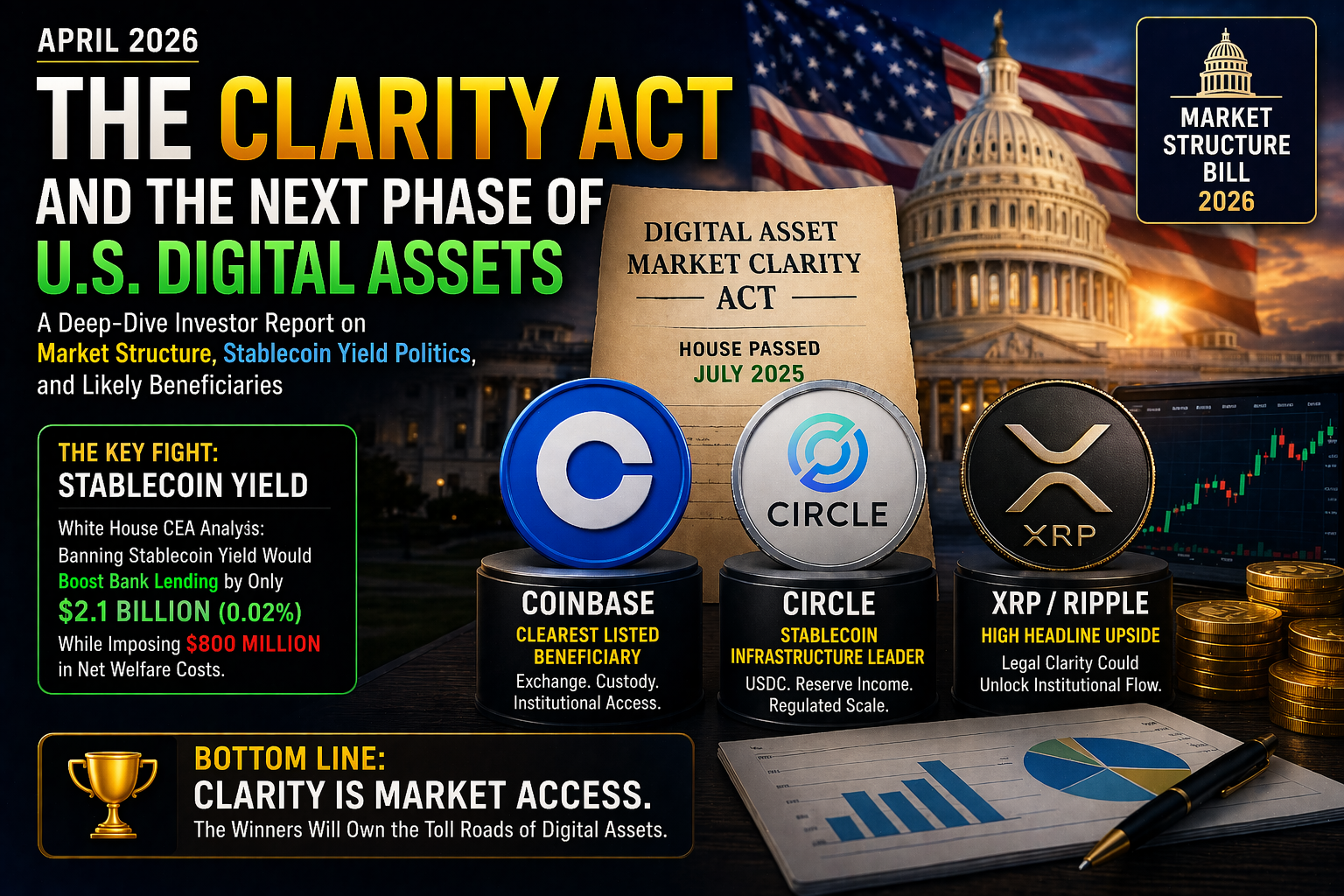

The Digital Asset Market Clarity Act is a federal market-structure bill. It defines where the SEC stops, where the CFTC begins, and how digital asset businesses can legally operate without guessing which regulator reinterprets the rules next.

Legislative timeline:

- May 2025: House introduction

- June 2025: Cleared both House committees

- July 2025: Passed the House with bipartisan support

- January–March 2026: Senate stalled on stablecoin yield dispute

- March 23, 2026: Senators Alsobrooks and Tillis announce compromise language

- April 13, 2026: White House crypto adviser Patrick Witt confirms stablecoin yield deal is holding. Says remaining hurdles are "no longer unsolvable."

- Late April 2026: Banking Committee markup must happen to stay on track for passage before the August congressional recess

The bill classifies digital assets into three functional categories: digital commodities (CFTC-supervised), investment-contract-like assets (SEC-supervised), and stablecoins (subject to separate stablecoin legislation). Assets tied to blockchain functionality and decentralized network use get a clearer path toward commodity-style treatment. Securities-like issuance stays inside securities law.

This classification matters because it is what institutions have been waiting for. Pension funds, insurers, and asset managers do not avoid crypto only because of volatility. They avoid large parts of the market because the legal perimeter is unclear. CLARITY defines that perimeter. If it succeeds, the consequence is not just higher token prices. It is the normalization of brokerage, custody, market-making, treasury, and payments infrastructure for digital assets in the U.S.

The Real Fight: Stablecoin Yield

The largest practical dispute has been over yield-bearing stablecoins. Banks view them as a deposit flight threat. Crypto platforms view them as a natural extension of on-chain dollars.

The compromise (March 23, 2026 draft):

- Passive yield on stablecoin balances: banned

- Activity-based rewards (payments, transfers, platform usage): permitted on a narrow basis

- Programs that resemble bank interest in any way: prohibited

- Applies to exchanges, brokers, and affiliated entities

The crypto industry's reaction was mixed. The language is broad enough to close structural workarounds that platforms like Coinbase had used to pass stablecoin rewards to users even after the GENIUS Act restricted issuers directly.

The CEA data that changed the debate:

The White House Council of Economic Advisers published an analysis in April 2026 concluding that banning stablecoin yield would increase bank lending by only $2.1 billion — or 0.02% — while imposing a net welfare cost of $800 million. That finding directly undercuts the banking lobby's core argument.

As of April 13, White House adviser Patrick Witt confirmed the yield compromise is holding. Senator Lummis's press team stated that stablecoin yield negotiations are "99% of the way to resolution." The remaining friction is political, not technical.

The deadline pressure:

Failure to advance from the Banking Committee before May could severely damage the bill's chances of becoming law before the November 2026 midterm elections. The legislative window is real but narrowing.

The Beneficiary Stack

Value flows in layers when market plumbing gets legalized.

Layer 1: Infrastructure — Exchanges, brokers, custodians, stablecoin issuers

Layer 2: Assets — Tokens with cleaner legal standing and institutional utility

Layer 3: Adjacent — Compliance, analytics, treasury infrastructure

Layer 1 is where public-market investors have the clearest visibility today.

Coinbase (COIN) — Clearest Listed Beneficiary

Coinbase is not the best token picker. It is the most directly levered listed U.S. company to regulatory normalization across trading, custody, brokerage, staking-adjacent services, and institutional access.

Why CLARITY specifically helps COIN:

- Legal clarity expands the addressable institutional market

- A formal U.S. stablecoin framework strengthens USDC as regulated dollar infrastructure

- Coinbase receives 50% of Circle's residual USDC reserve revenue — stablecoin regulation is directly a Coinbase earnings story

The stablecoin yield risk:

If the final legislation heavily constrains yield-bearing features, some parts of Coinbase's product ambition around on-chain dollars become less monetizable. The March compromise language is broader than bulls hoped. Coinbase's ability to pass stablecoin rewards to users may be permanently limited.

Net assessment: Among listed equities, Coinbase remains the highest-conviction CLARITY beneficiary. Regulatory normalization compresses legal discount rates on its entire business model.

Circle (CRCL) — Stablecoin Infrastructure, More Nuanced Than Headlines

Circle sits at the center of regulated stablecoin infrastructure through USDC and EURC. But the investment case requires more precision than "stablecoins up = Circle up."

Three things investors should understand:

1. Revenue concentration. Reserve income remains the overwhelming majority of Circle's revenue. Q4 2025 reserve income was $733 million, up 69% year over year, driven by a 100% increase in average USDC circulation. This is a rate-sensitive spread business, not a diversified fintech platform.

2. Shared economics. Coinbase receives 50% of residual USDC reserve revenue. Circle's economics are partly shared economics. How lawmakers handle yield features and distribution directly affects how much of the reserve stack Circle keeps for itself.

3. Reserve quality is the moat. The majority of USDC reserves sit in the Circle Reserve Fund (USDXX), an SEC-registered 2a-7 government money market fund holding short-dated Treasuries, repo, and cash. That reserve architecture becomes more valuable when regulation turns from theory into enforcement. Scaled, reserve-heavy, transparency-oriented issuers are favored by regulatory frameworks. Circle is one of very few issuers that fits that description.

Net assessment: Circle benefits from CLARITY, but the upside still depends on rates, circulation growth, and how much reserve economics it retains versus shares.

XRP / Ripple — Narrative Trade, Not Equity Thesis

XRP benefits from reduced legal uncertainty if CLARITY creates clearer classification for non-Bitcoin, non-Ethereum assets. Some market commentary frames a Senate path for CLARITY as a direct XRP catalyst.

The distinction that matters:

Ripple is not a listed equity like Coinbase or Circle. XRP is a token. The investment pathway is more speculative, more narrative-driven, and more exposed to token-market volatility than direct infrastructure equity.

Coinbase and Circle can be underwritten as enterprises. XRP can be traded as a legal-regime beta asset. These are not the same kind of investment.

Key Metrics

Coinbase (COIN)

| Metric | Value |

|---|---|

| Market Cap | ~$55B |

| 2025 Revenue | ~$6.6B |

| USDC Reserve Revenue Share | 50% of Circle residual |

| Institutional Custody AUC | $220B+ |

| CLARITY Leverage | Trading + Custody + Brokerage + Staking |

Circle (CRCL)

| Metric | Value |

|---|---|

| Market Cap | ~$8B (post-IPO) |

| Q4 2025 Reserve Income | $733M (+69% YoY) |

| USDC Circulation | $60B+ |

| Reserve Fund | USDXX (2a-7 gov MMF) |

| CLARITY Leverage | Stablecoin framework + institutional trust |

Scenario Analysis

Scenario A: Senate moves, passage path credible

Banking Committee markup in late April. Floor debate before August recess. Market begins pricing passage probability above 60%.

- COIN: Multiple expansion through lower regulatory discount rates

- CRCL: Reserve economics reinforced by framework legitimacy

- Large-cap digital assets: De-risked U.S. legal treatment broadens institutional appetite

- Stablecoin adoption accelerates where institutions have waited for legal clarity

Scenario B: Delay extends, window narrows

Stablecoin yield or political riders (community bank deregulation, conflict-of-interest provisions) stall the markup. Bill drifts past May.

- Institutional deployment slows in the U.S.

- Value accrues to offshore jurisdictions with clearer frameworks

- Already-legitimized exposures (BTC-linked products) strengthen relative to broader altcoin and infrastructure complexity

- U.S. crypto infrastructure businesses trade at persistent regulatory discount

Delay does not kill the market. It narrows the opportunity set.

The Risk Stack

1. One bill cannot solve everything. CLARITY reduces legal uncertainty. It does not eliminate business-model risk, token dilution, competitive pressure, or execution risk.

2. Stablecoin yield compromise may satisfy neither side. The narrow activity-based rewards model is less bullish than crypto platforms wanted and less restrictive than banks demanded. Parts of the economics may be less attractive than current speculation implies.

3. Valuation risk. Good regulatory news can be overpaid for if the market front-runs passage and prices in perfect outcomes before the legal process completes.

4. Political riders. Senate Republicans are discussing attaching community bank deregulation to CLARITY. Senate Democrats are focused on conflict-of-interest provisions targeting government officials' crypto investments. Either rider could slow the bill or change its scope.

Bottom Line

The CLARITY Act is an attempt to turn the U.S. digital-asset market from a litigation-defined market into a law-defined market. That is a structural shift larger than spot ETF approval, because it affects the entire market plumbing — not just access to one or two assets.

The stablecoin yield dispute, which had been the single largest bottleneck, is now 99% resolved. The legislative window is real but narrowing. Banking Committee markup must happen by late April to maintain a credible path to passage before the August recess.

Beneficiary ranking:

1. Coinbase — Best listed market-structure beneficiary. Most directly levered to regulatory normalization across trading, custody, brokerage, and institutional access.

2. Circle — Best pure stablecoin infrastructure play. High-quality reserve architecture becomes more valuable under enforcement. Upside depends on rates, circulation, and retained economics.

3. XRP — Highest headline sensitivity. Less clean as an investable operating-business exposure. Narrative trade, not equity thesis.

The analogy is not "another ETF catalyst." The analogy is the legalization of market plumbing.

When legal roads get built, the biggest winners are the companies that own the toll roads. Coinbase and Circle are building those toll roads now.

About COIN

Share your analysis

Keep it data-driven. No investment advice.

- Keep it data-driven and respectful

- No investment advice (buy / sell / hold)

- No spam, promotion, or solicitation

- No profanity or offensive content

- Violations are automatically removed

Data: Financial Modeling Prep, Alpha Vantage, CoinGecko

NOT investment advice. Always do your own research.