Crypto Treasury Stocks: Leveraged Genius or Financial Engineering Gone Too Far?

Strategy, Bitmine, Metaplanet, Twenty One — a sector map for investors who want to know what they're actually buying. mNAV framework, BTC vs ETH treasury comparison, and the 5 risks that define this sector in 2026.

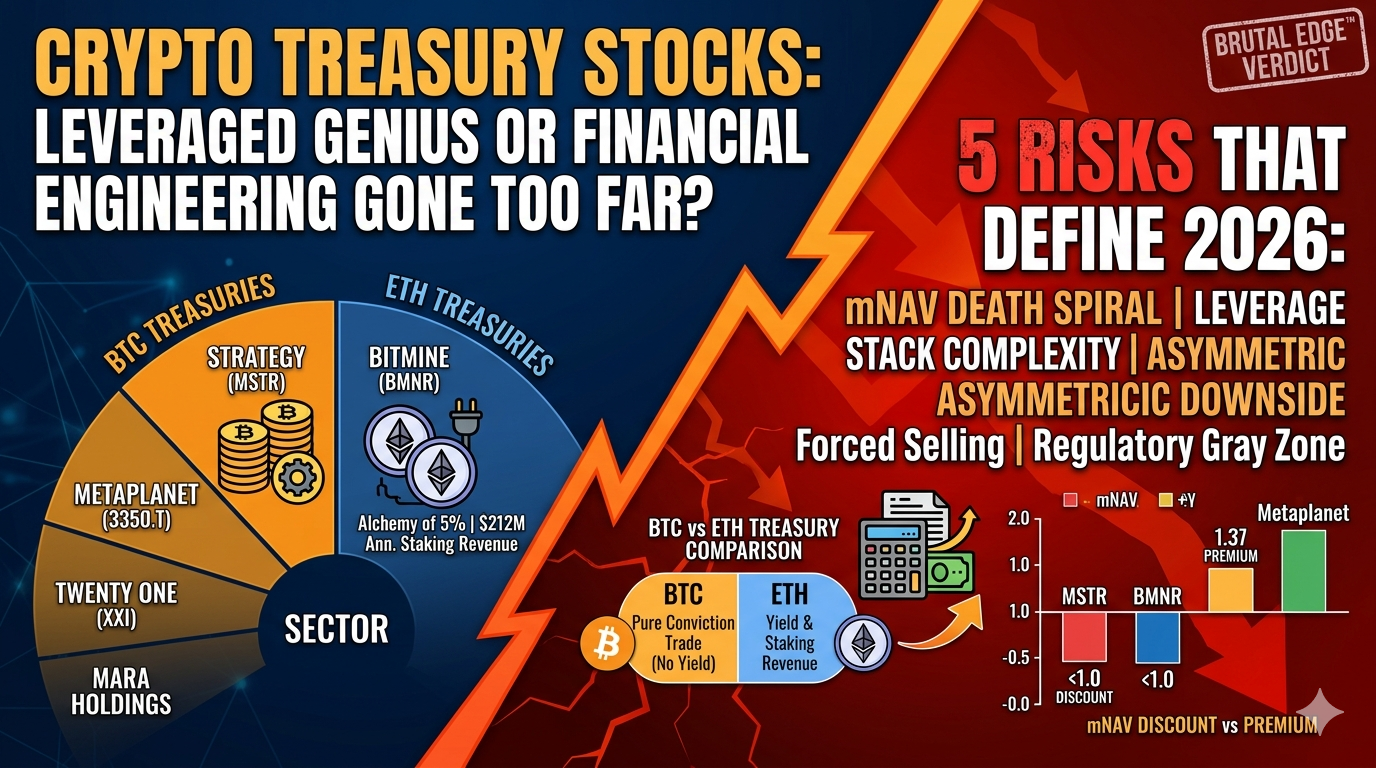

🔥 BRUTAL EDGE™ VERDICT

"Crypto treasury stocks are not equity investments. They are leveraged conviction trades wearing a stock ticker. The sector rewards you when crypto runs — and punishes you harder when it doesn't. Know which side of the bet you're on before you buy a single share."

The Thesis

There is a new category of public company on Wall Street that doesn't sell products, doesn't generate operating revenue in any traditional sense, and doesn't pretend to. These companies exist for one purpose: to accumulate cryptocurrency on their balance sheet, then convince the stock market that their shares are the best way to get exposure to that crypto.

They are called Digital Asset Treasury companies, or DATs. And in 2026, they are one of the most polarizing sectors in the market.

The pitch is simple. Buy crypto. Hold it. Issue equity or convertible debt to buy more. If the crypto goes up, your stock goes up faster — because shareholders get leveraged exposure without managing wallets, custody, or tax complexity. The company becomes a publicly traded vehicle for a directional bet on a single digital asset.

The problem is equally simple. If the crypto goes down, the stock goes down faster. And if the company's market capitalization falls below the value of the crypto it holds, the entire financial engineering machine starts to work in reverse.

This report is not about whether crypto will go up. That is a different question. This report is about what you are actually buying when you buy a crypto treasury stock — and whether the financial structures underneath these companies create value, or just amplify risk.

The Sector Map

The crypto treasury sector splits into two camps: BTC treasuries and ETH treasuries. The distinction matters far more than most investors realize.

BTC Treasury Companies

Strategy (MSTR) is the sector's origin story. Michael Saylor began accumulating Bitcoin in 2020 and never stopped. As of April 2026, Strategy holds approximately 766,970 BTC — roughly two-thirds of all Bitcoin owned by public companies. The company acquired 44,377 BTC in March 2026 alone, funded largely through its STRC preferred share offering. Strategy has filed for a $42 billion at-the-market program to continue buying. If proceeds arrive at roughly $2.3 billion per month and Bitcoin stays near $75,000, the company could reach 1 million BTC by late 2026.

The financial architecture here is important. STRC is a variable-rate perpetual preferred share yielding around 11.5% annually. It sits above common stock in the capital structure, which means STRC holders get paid before MSTR shareholders see any benefit. That structure funded record Bitcoin purchases, but it also means the common equity is subordinated to a growing layer of preferred obligations.

Strategy trades at an mNAV below 1.0 — meaning the stock market values the company at less than its Bitcoin holdings. That discount reflects skepticism about dilution, the cost of the preferred stack, and the concentration risk of having one company dominate 94% of net corporate Bitcoin accumulation in a single month.

Metaplanet (3350.T / MTPLF) is the Japanese counterpart. The company holds approximately 40,177 BTC acquired at an average cost of about $97,000 per coin. In Q1 2026, Metaplanet added 5,075 BTC for roughly $398 million, overtaking MARA Holdings to become the third-largest corporate Bitcoin holder globally.

Metaplanet trades at an mNAV of 1.37 — a premium. That premium matters enormously because it means equity issuance is accretive: every time Metaplanet issues stock to buy Bitcoin, existing shareholders end up with more Bitcoin per share. Operating outside the US regulatory environment and maintaining a relatively clean capital structure gives Metaplanet structural advantages that Strategy currently lacks.

Twenty One Capital (XXI) holds 43,514 BTC and sits in second place globally, but it has not purchased Bitcoin since August 2025. Its rise in the rankings is purely a function of MARA selling. XXI is a passive holder in what should be an active accumulation game.

MARA Holdings (MARA) is the cautionary tale. The former mining giant borrowed aggressively during the bull run, then had to sell approximately 15,133 BTC in Q1 2026 to service debt. As one analyst noted: this is the exact scenario critics of debt-fueled treasury strategies have warned about. MARA has gone from the second-largest Bitcoin treasury to a diminished position, illustrating what happens when leverage meets a drawdown.

Strive Asset Management took a different path. It increased its treasury to 13,628 BTC through PIPE proceeds and, notably, acquired Semler Scientific in an all-stock deal that added 5,048 BTC. The acquisition play is worth watching — it suggests the sector may consolidate rather than grow through individual accumulation alone.

ETH Treasury Companies

Bitmine Immersion Technologies (BMNR) is the ETH sector's defining company. As of April 13, 2026, Bitmine holds 4,874,858 ETH — equal to 4.04% of total Ethereum supply. The company's stated goal, which it calls the "Alchemy of 5%," is to own 5% of all ETH in existence. It is 81% of the way there.

Bitmine's financial profile is dramatically different from a BTC treasury. Here is why.

First, ETH generates yield. Bitmine has 3.33 million ETH staked through MAVAN (Made in America Validator Network), its proprietary staking platform, generating $212 million in annualized staking revenue at a 2.89% yield. At full deployment, projected annual staking revenue reaches $310 million. That makes Bitmine arguably the only crypto treasury company with a real recurring revenue line.

Second, Bitmine's stock tells a more volatile story. BMNR traded between $3.20 and $161.00 over the past year. It currently trades around $21, down roughly 87% from its peak. The company's market capitalization is approximately $9.7 billion, against total holdings of $11.8 billion including cash. That means the market is valuing Bitmine at a discount to its assets — the same mNAV compression afflicting Strategy.

Third, Tom Lee — the Fundstrat co-founder and prominent market strategist — serves as Bitmine's chairman, and he recently made a striking claim: that ETH outperforming gold by 2,743 basis points since the start of the Iran conflict demonstrates that ETH is "the wartime store of value." That framing is aggressive, but it tells you how Bitmine's leadership thinks about positioning.

Bitmine also holds $200 million in Beast Industries, $85 million in Eightco Holdings (which gives indirect exposure to OpenAI), $719 million in cash, and 198 BTC. The company uplisted from NYSE American to the New York Stock Exchange on April 9, 2026, and expanded its share repurchase authorization to $4 billion — among the largest announced this year.

The mNAV Framework

If you take one thing from this report, let it be this: mNAV is the single most important metric for evaluating any crypto treasury stock.

mNAV stands for market-to-net-asset-value. It compares the company's stock market valuation to the value of the crypto on its balance sheet. An mNAV above 1.0 means the market values the company at more than its crypto holdings. An mNAV below 1.0 means the opposite.

Why this metric matters so much is structural. When a crypto treasury company has an mNAV above 1.0, issuing new equity is accretive. The company sells shares worth more than the crypto it buys with the proceeds, so each existing shareholder ends up owning more crypto per share after the issuance than before. This is the "flywheel" that made Strategy's early accumulation so powerful and that Metaplanet is currently exploiting.

When mNAV falls below 1.0, the math inverts. Issuing equity becomes dilutive — shareholders lose crypto-per-share with every issuance. The company can still buy crypto with debt, but that introduces leverage risk. Or it can buy back shares (since shares are "cheaper" than the underlying crypto), which is what Bitmine's $4 billion buyback authorization signals.

The current sector snapshot tells a clear story. Metaplanet operates at a premium mNAV. Strategy and Bitmine operate at discounts. That bifurcation is the sector's central tension in 2026: one company can still issue equity accretively, while the two largest cannot.

BTC Treasury vs ETH Treasury

The choice between BTC and ETH treasury exposure is not just about which crypto you think will outperform. It is about fundamentally different business models dressed in similar packaging.

A BTC treasury is a pure conviction trade. Bitcoin does not generate yield at the protocol level. A company that holds Bitcoin generates no revenue from that Bitcoin unless it lends it, sells it, or uses it as collateral. Strategy's revenue comes entirely from the spread between its cost of capital and Bitcoin's appreciation. If Bitcoin does not appreciate, the company's financial obligations do not shrink — they keep accumulating.

An ETH treasury adds a yield layer. Ethereum's proof-of-stake consensus mechanism means staked ETH generates protocol-level rewards. Bitmine's 2.89% staking yield translates to real revenue: $212 million annualized, with $310 million projected at full deployment. That does not make Bitmine "safe" — it is still overwhelmingly exposed to ETH price risk — but it does mean the company generates cash flow that a BTC treasury structurally cannot.

The tradeoff is liquidity depth and institutional acceptance. Bitcoin has deeper institutional adoption, more ETF infrastructure ($147 billion+ in ETF assets), and a simpler narrative. Ethereum's ecosystem is more complex, its regulatory status less settled, and its price action more volatile. Each 1% move in ETH adds or subtracts roughly $100 million from Bitmine's holdings.

For investors, the question reduces to this: Do you want leveraged exposure to digital gold with no yield (BTC treasury), or leveraged exposure to a yield-generating smart contract platform (ETH treasury)? Neither is inherently better. Both amplify the underlying asset's volatility through the equity wrapper.

The Risk Stack

Five risks define this sector in 2026. Every investor in a crypto treasury stock needs to understand all five before buying.

1. mNAV Death Spiral

When mNAV falls below 1.0 and the company cannot issue accretive equity, its primary growth engine stalls. If it continues issuing equity anyway, it dilutes shareholders. If it stops, it cannot accumulate more crypto, and the growth narrative dies. This is what Strategy is navigating right now.

2. Concentration: The One-Buyer Market

In March 2026, Strategy accounted for approximately 94% of net corporate Bitcoin purchases. Strip out Strategy, and the rest of the sector is flat to negative. That level of concentration creates systemic risk: if Strategy ever becomes a forced seller, the impact on Bitcoin's price — and therefore on every other treasury company — would be severe.

3. Leverage Stack Complexity

Strategy's capital structure now includes common equity, STRC preferred shares, STRK preferred shares, and convertible notes. Each layer has different seniority, different obligations, and different break-even points relative to Bitcoin's price. Bitmine's structure is simpler today, but the $4 billion buyback authorization signals that complexity may grow. Investors buying common equity in these companies are buying the most subordinated layer of a levered crypto position.

4. Crypto Price Asymmetry

When Bitcoin drops 2%, crypto treasury stocks often drop 6% or more. This asymmetric downside is the leverage working against shareholders. In a sustained drawdown, the equity can lose multiples of the underlying crypto's decline. BMNR's 87% fall from its 52-week high while ETH declined roughly 50-55% illustrates this amplification effect.

5. Regulatory and Governance Risk

Crypto treasury companies operate in a regulatory gray zone. Tax treatment of crypto holdings, SEC reporting requirements for concentrated digital asset positions, and evolving accounting standards all create uncertainty. Additionally, executive compensation structures deserve scrutiny — Bitmine recently amended employment agreements granting the CEO and CFO annual stock option grants totaling $2.25 million, a move that triggered selling pressure.

The Survival Playbook

Not all crypto treasuries will survive 2026. The ones that do will share three characteristics.

Cash reserves matter. Strategy announced a $1.4 billion cash reserve covering roughly 21 months of preferred dividend obligations. That buffer means the company will not be forced to sell Bitcoin to meet obligations during a bear market. Companies without similar reserves — like MARA, which had to sell — are structurally fragile.

Staking revenue changes the equation. Bitmine's $212 million in annualized staking revenue does not eliminate ETH price risk, but it creates a revenue floor that pure BTC treasuries do not have. As staking operations scale, this revenue line becomes a meaningful differentiator.

mNAV discipline determines long-term value. Companies that issue equity only when mNAV exceeds 1.0 protect existing shareholders. Companies that issue regardless are transferring value from shareholders to the crypto on the balance sheet. The best-run treasuries will maintain strict mNAV discipline and pivot to buybacks when trading at discounts.

Bottom Line

Crypto treasury stocks are not equity investments in the traditional sense. They are structured leverage on a directional crypto bet, wrapped in a stock ticker for convenience. The financial engineering can be brilliant when crypto rises and devastating when it falls.

The sector in April 2026 is bifurcated. Metaplanet operates at a premium and retains the accretive issuance flywheel. Strategy and Bitmine operate at discounts and must rely on buybacks, debt, or crypto appreciation to create shareholder value. MARA is a cautionary tale about what happens when leverage meets a drawdown. The rest of the field — Twenty One, Strive, GameStop's crypto allocation — ranges from passive to opportunistic.

If you buy a crypto treasury stock, know exactly what you are buying. You are not buying a company. You are buying a leveraged view on a specific cryptocurrency, filtered through a capital structure that may or may not work in your favor. The mNAV tells you which side of that equation you are on today. Everything else is narrative.

For informational and educational purposes only. NOT investment advice. Always do your own research before making investment decisions.

About MSTR

Share your analysis

Keep it data-driven. No investment advice.

- Keep it data-driven and respectful

- No investment advice (buy / sell / hold)

- No spam, promotion, or solicitation

- No profanity or offensive content

- Violations are automatically removed

Data: Financial Modeling Prep, Alpha Vantage, CoinGecko

NOT investment advice. Always do your own research.