Circle Internet Group (CRCL): The Stablecoin Leader That Fell Hard — and May Still Matter

Circle at $105: USDC at $75.3B circulation, 96% revenue from reserve yield, 162% EPS beat — but rate sensitivity and regulatory whiplash define this stablecoin infrastructure bet.

🔥 BRUTAL EDGE™ VERDICT

"Circle looks more attractive after the drawdown than it did at $299. But strip away the narrative and the economics are clear: 96% of revenue comes from reserve yield. This is a rate-sensitive stablecoin spread business with infrastructure ambitions — not the other way around. Investors who mistake the vision for the current reality will misprice this stock."

The Company

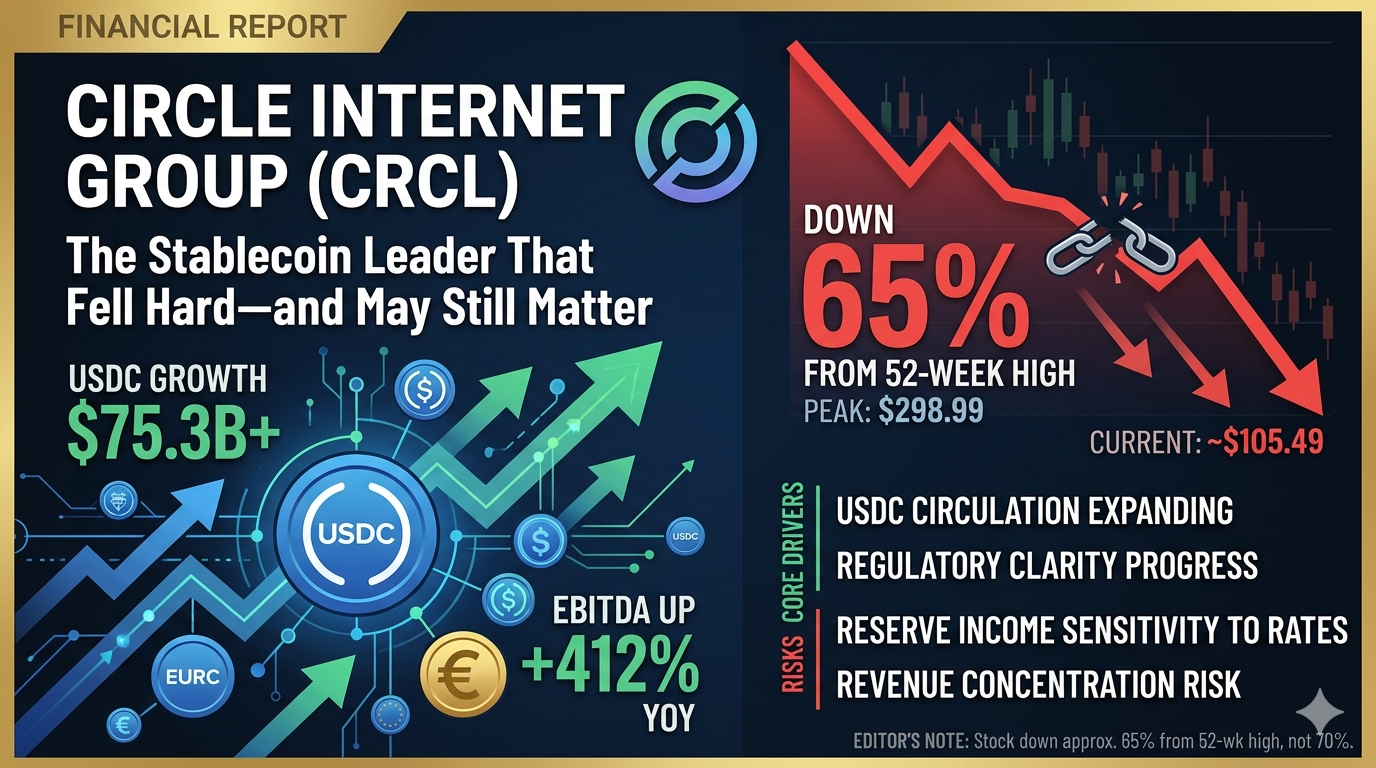

Circle is the issuer of USDC, the second-largest stablecoin in the world with roughly $75.3 billion in circulation as of Q4 2025. The company sits at the center of three linked businesses: it issues and manages a dollar-backed stablecoin, it earns reserve income on the assets backing those coins, and it is trying to turn USDC from a crypto trading instrument into a broader payments and financial infrastructure layer.

Circle frames this strategy as building an "Economic OS for the internet." That is ambitious language, but directionally useful. If USDC remains mainly a crypto-native settlement token, Circle stays a good but cyclical financial utility. If USDC becomes a widely used payments and treasury rail, Circle starts to look like a durable network business. The stock's long-term value depends on which of those two futures is closer to reality.

Approximately 88% of USDC reserves are held in the Circle Reserve Fund managed by BlackRock and custodied at BNY. That reserve structure matters — it gives institutional credibility that most competitors cannot match.

The Numbers

| Metric | Value |

|---|---|

| Price (Apr 15) | ~$105.49 |

| Market Cap | ~$24.4B |

| 52-Week Range | $49.90 — $298.99 |

| IPO Price (2025) | $31.00 |

| Q4 2025 Revenue | $770M |

| Q4 2025 Reserve Income | $733M (69% YoY growth) |

| Q4 2025 Adjusted EBITDA | $167M (+412% YoY) |

| Q4 2025 EPS | $0.43 (est. $0.16 — 162% beat) |

| USDC Circulation | $75.3B (+72% YoY) |

| Reserve Return Rate | 3.8% (down 68bps YoY) |

| Reserve Income % of Revenue | 96.4%–98.5% (H1 2025) |

| Next Earnings | June 3, 2026 |

The Q4 earnings beat was massive — 162% above estimates. But the number that matters most is buried in the SEC filings: reserve income accounted for between 96.4% and 98.5% of total revenue in the first half of 2025. That is the single most important fact investors need to understand about Circle. Everything else is narrative until this ratio changes.

Why It Collapsed

Three reasons, in order of importance.

The stock ran too far ahead of itself. A 52-week high of $298.99 versus the $31 IPO price implies investors were paying for a near-perfect combination of stablecoin adoption, favorable regulation, strong rates, and platform expansion. Once any one of those assumptions wobbled, the stock compressed hard.

Circle is not a pure volume growth story. Its profitability is tied to both USDC in circulation and the reserve return rate. Q4 showed this dynamic clearly: reserve income rose 69% year over year, helped by 100% growth in average USDC in circulation, but partly offset by a 68 basis point decline in the reserve return rate. Strong stablecoin growth can be partially neutralized by lower yields. This is the structural tension at the core of the business.

The market has no valuation framework for this company. Circle is not a bank, not a software company, not a classic exchange, and not a crypto token proxy. When a business sits between categories, the stock becomes unstable because investors keep rotating between different valuation lenses. That instability is a feature of the stock, not a temporary condition.

The Investment Case

Four pillars support the long case.

USDC growth is real and at scale. $75.3 billion in circulation is no longer hypothetical. This is a functioning monetary network with institutional reserve infrastructure managed by BlackRock.

The core model is profitable when both adoption and rates cooperate. Q4's $167 million adjusted EBITDA (+412% YoY) demonstrates the earnings power that emerges when circulation rises and yields stay healthy.

Regulation is becoming a tailwind. The GENIUS Act framework is moving toward final rulemaking with July 2026 as an important deadline. Regulatory clarity tends to favor scaled, reserve-heavy, compliance-oriented issuers over weaker competitors. Circle is positioned to benefit more than any other public stablecoin company.

The stock has already derated sharply. At ~$105 versus a $299 peak, speculative premium has been removed. That does not make it cheap automatically, but it makes the setup more balanced than when CRCL was trading at euphoric levels.

The Risk Stack

1. Rate sensitivity — the dominant risk.

If short-term yields fall materially, Circle's reserve income softens even if USDC circulation keeps growing. The company has already demonstrated this: lower reserve return rates offset part of its circulation growth benefit in Q4. Every Fed cut compresses Circle's top line directly. The company is diversifying into CPN and Managed Payments precisely because it knows the reserve yield model has a ceiling. Whether those products scale fast enough to offset rate pressure is the central investment question.

2. Revenue concentration.

96% of revenue from reserve income means Circle's "fintech platform" narrative is still aspiration, not reality. Until non-reserve revenue becomes a material part of the story, Circle struggles to justify a high software-like multiple. Platform diversification is part of the pitch, but not yet the economic center of gravity.

3. Competitive and distribution pressure.

Stablecoins are a scale game, and scale attracts both incumbents and regulators. The stronger the sector becomes, the more competition Circle will face from exchanges, payment companies, banks, and other regulated issuers. Tether remains dominant globally. Circle's business quality can improve at the same time its competitive moat becomes more contested.

4. Regulatory whiplash.

The GENIUS Act helps, but the Clarity Act draft on March 24 showed that Congress can giveth and taketh in the same quarter. Circle's stock dropped 30%+ on a single legislative draft suggesting potential limits on stablecoin yield. That kind of policy sensitivity is unusual for a $24 billion company and will persist as long as the regulatory framework remains unfinished.

Bottom Line

Circle is one of the more interesting public-market names in digital assets because it offers something rare: real revenue, real reserves, real regulation, and real macro sensitivity all in one stock. It is not a concept stock.

But discipline matters here. CRCL is easiest to misunderstand when it is described as either a revolutionary software platform or a plain interest-income shell. It is neither. It is a stablecoin infrastructure company whose current economics still look more financial than software-like, but whose long-term upside depends on whether that infrastructure becomes deeply embedded in global payments and onchain finance.

Circle looks more attractive after the drawdown than it did at the peak. It still needs to prove that its non-reserve platform story can become material enough to support a premium valuation through a lower-rate cycle. For investors, CRCL is best viewed as a high-quality, rate-sensitive stablecoin network bet — not as a simple rebound trade.

About CRCL

Share your analysis

Keep it data-driven. No investment advice.

- Keep it data-driven and respectful

- No investment advice (buy / sell / hold)

- No spam, promotion, or solicitation

- No profanity or offensive content

- Violations are automatically removed

Data: Financial Modeling Prep, Alpha Vantage, CoinGecko

NOT investment advice. Always do your own research.