The Mental Game #002: How to Survive an AI Bubble Without Denying the Technology

AI is real. That's exactly why it's dangerous. Apollo estimates $5-6 trillion in US data center investment alone. Goldman projects $527B in hyperscaler capex for 2026. The technology will transform the world. Most investors betting on it will still lose money. Here's how to not be one of them.

The Uncomfortable Setup

AI is real.

That's exactly why it's dangerous.

Apollo Global Management's president Jim Zelter recently estimated that US data centers alone may require $5-6 trillion in investment over the next five years. Goldman Sachs projects $527 billion in hyperscaler AI capex for 2026, the largest annual step-up in corporate history. Apollo's internal research calculates the market is pricing in roughly $4-5 trillion of digital infrastructure investment by 2030.

These numbers are not speculation. They are real capital commitments being made right now by real institutions with real money.

And here is the problem almost nobody wants to look at directly:

For that investment to generate acceptable returns, annual AI revenue would need to reach $1.5-2 trillion by 2030. Actual AI revenue in 2025 was $35-65 billion.

That's a 30-50x gap between what's being invested and what's currently being earned.

The gap might close. The gap might not.

The honest position is that nobody knows. But the investor who acts as if the gap doesn't exist is betting their portfolio on something that the people building the infrastructure themselves are openly worried about.

This is The Mental Game #002 — how to stay invested in the biggest technology story of your career while preventing that story from destroying your capital.

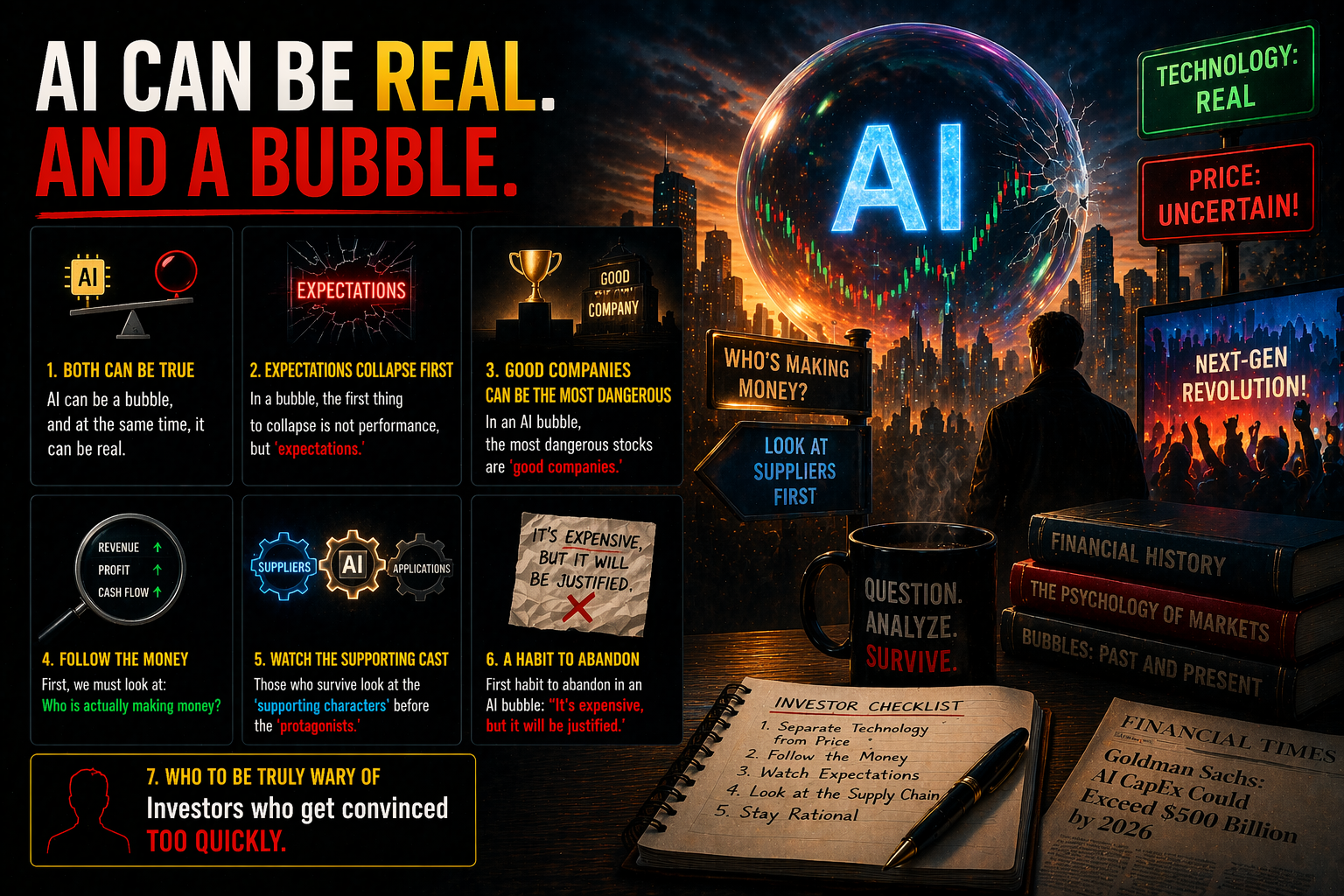

1. First Admission — AI Can Be Both a Bubble and Real

Most investors misunderstand what bubbles are.

When they hear "bubble," they immediately think "fake." But historically, the most dangerous bubbles have not come from fake technology. They have come from genuinely transformative technology.

Railways were real. The internet was real. AI is real.

That's what makes them more dangerous. Markets are easier to excite when they see actual innovation. They justify high prices longer when the underlying story has legitimacy. The gap between "technology will matter" and "this stock at this price will make money" widens before anyone is willing to acknowledge it.

Goldman Sachs' 2026 outlook makes this distinction explicit. The bank projects massive continued capex growth while simultaneously warning that investor attention is shifting from "infrastructure builders" to "companies actually monetizing AI productivity." Those are different companies. The market is starting to ask a harder question than it was asking in 2024.

The first sentence an investor needs to stop saying:

> "AI is real, so AI stocks will eventually go up."

The more accurate sentence:

> "AI can be real and still not justify every current price attached to it."

The first sentence is a narrative.

The second sentence is a framework.

One of them keeps you invested through the inevitable volatility. The other one gets you wiped out when volatility arrives and reality doesn't instantly arrive with it.

2. What Breaks First in a Bubble Isn't Earnings — It's Expectations

A common mistake in bubble regimes is assuming the business has to collapse for the stock to collapse.

It doesn't. What usually breaks first is not the business. It's expectations.

Look at what's actually happening right now in AI:

- Real capex is rising

- Real data centers are being built

- Real chips are being shipped

- Real products are being deployed

- Real revenue is growing

The business is moving. The problem is that the stock price is moving faster.

This is exactly what Jim Zelter warned about. In his Goldman Sachs podcast interview, he drew on three decades of credit market experience to make one surgical distinction:

> Transformative technology and profitable technology are not the same thing.

He specifically compared AI to the cell phone era. Utility was never in doubt. Economic returns to capital owners were far less predictable than the utility suggested they should be.

Zelter's direct quote: "Just because companies need capital doesn't mean they're all great investments."

That is the most important sentence in the current AI debate, and it comes from someone whose firm has deployed $40 billion into AI infrastructure. He is not an AI skeptic. He is a capital allocator warning you that needing capital and rewarding capital are separate events.

The real question for 2026-2030 is this:

> The technology will likely succeed.

> Will the capital that financed it get paid back at the rates the market is currently assuming?

That's the question the stocks are increasingly being priced on. Not "does AI matter?" but "who collects the economic rent when AI matters?"

Those are very different inputs, and they produce very different price paths.

3. The Most Dangerous Stock in a Bubble Is the "Good Company"

This sounds paradoxical, but it's structurally true:

In bubble regimes, good companies are often riskier than bad companies.

Bad companies scare everybody. Investors naturally apply skepticism. Position sizes stay small.

Good companies earn universal admiration. Investors feel safe. Position sizes grow. Prices compound faster than fundamentals justify.

When the correction arrives, the good company doesn't fall because it's a bad business. It falls because it was priced for perfection, and perfection wasn't delivered.

The investor's rationalization during bubbles:

> "It's a great company."

> "Dominant market share."

> "Strong cash flow."

> "Best technology in the category."

> "Will be even bigger in 10 years."

All of these statements can be true. The stock can still fall 40-60% from its peak. It happened to Cisco in 2000 even though Cisco's underlying business continued to grow for decades afterward. Cisco's 2000 high took 24 years to be exceeded — in 2024 dollars, adjusted for inflation, it arguably still hasn't been.

The principle most retail investors never internalize:

> A good company and a good stock are not the same thing.

A good company is likely to survive and eventually win in its market.

A good stock requires that the company's win is not yet fully priced in.

In a bubble regime, good companies are easy to find.

Good stocks are not.

4. The Question That Separates Survivors From Casualties

In AI bubble regimes, the most common analytical mistake is conflating technological importance with investment attractiveness.

The first survival technique is to change the question.

Stop asking:

> "Will AI change the world?"

Start asking:

> "Because of AI, who is already making money, and from which layer of the stack?"

This question immediately segments AI companies into four useful categories.

Category 1: Infrastructure Sellers

Chips, networking, power, cooling, data center equipment. They get paid simply because the AI boom is happening. They don't need AI to succeed commercially — they only need the buildout to continue.

Currently dominant narrative. Most crowded positioning. Goldman Sachs flagged that AI infrastructure stocks returned 44% year-to-date while consensus 2-year forward EPS estimates rose only 9%. The gap between price action and earnings growth is the precise definition of multiple expansion. Multiple expansion works until it stops.

Category 2: Platform Operators

Foundation models, developer environments, software middleware, enterprise AI services. Revenue comes from usage and subscriptions.

Less crowded. Harder to analyze. More dependent on monetization path than infrastructure.

Category 3: Productivity Beneficiaries

Companies not selling AI directly, but whose cost structure improves or demand grows because of AI deployment in the broader economy. This is the segment Goldman sees as the 2026 "phase 3" of the AI trade.

Least narrative-driven. Hardest to identify early. Often the longest-duration winners historically.

Category 4: Narrative Holders

Companies talking AI but with weak actual monetization. Their stocks move on association, not fundamentals.

Most fragile. First to break in any correction. Usually indistinguishable from Category 2 during the bubble phase, distinguishable only after.

What the survivors do differently:

They do not blend these four categories. They especially do not treat Category 4 the way they would treat Category 1 or 2.

When you see an AI stock pitched, the first question should not be "is this company exciting?" but "which of these four buckets does this actually belong in, and what multiple am I paying for that bucket?"

5. Look at the Supporting Cast, Not the Stars

Every bubble has stars. Everyone focuses on the loudest, most visible names. The stocks everyone is already talking about.

But wealth in transformative technology cycles rarely concentrates exclusively in the stars. It concentrates significantly in the supporting infrastructure — the boring-looking companies that become indispensable precisely because the stars need them to function.

In the internet era, the obvious winners were portals and search engines. The less obvious winners — logistics, payments, cloud infrastructure, advertising networks, cybersecurity — built structural positions that compounded for 20+ years.

In the AI era, the overlooked supporting cast likely includes:

- Power generation and transmission

- Cooling systems and thermal management

- Electrical grid modernization

- Industrial automation components

- Testing and measurement equipment

- Construction-heavy data center buildout

- Specialized logistics and semiconductor supply chain

- Security and regulatory compliance software

Apollo's research notes that global data center demand could require an additional 90 GW of power by 2030. In US terms, that's equivalent to adding three New York Cities to the power grid. Every gigawatt requires approximately $50 billion in infrastructure investment.

These are not headline stocks. They are the physical reality making the headline stocks possible.

The second survival principle:

> Find the businesses the bubble cannot succeed without — especially the ones the bubble isn't obviously paying for yet.

This is where patient investors historically outperform. Not because they predicted the star correctly, but because they identified the bottleneck that would be compensated regardless of which star won.

6. The Habit to Kill Immediately — "It's Expensive but Justified"

The single most dangerous sentence in late-stage bubbles:

> "Yeah, it's expensive, but this time is different."

This sentence is almost always wrong. Not always. Almost always.

Here's the nuance most investors miss: the statement "this time is different" isn't wrong because things are never different. The statement is dangerous because it's where analysis ends instead of where it begins.

Saying "it's justified" should trigger the harder follow-up questions:

- How many years of growth is already priced in?

- Is that growth mathematically possible given market size?

- Will margins hold as competition intensifies?

- Who funds the capex, and how is it financed?

- Is reported profit matching actual cash flow?

- What specifically needs to go right for this price to be correct?

- What happens to the thesis if growth comes in 10% below expectations?

Most bubble casualties don't fail because they were analytically ignorant. They fail because they stopped at "justified" and never did the work underneath it.

Valuation is not the enemy. The enemy is the habit of ignoring valuation.

You can choose to pay a premium multiple. That's a strategy. But paying it while refusing to do the math that justifies it is not a strategy — it's a position you hold until reality corrects you.

7. The Investor Most at Risk Right Now — The Fast Convert

Late-bubble psychology has one reliable pattern: investors become more convinced over time instead of less convinced.

This is the opposite of what disciplined investors do. Disciplined investors demand more evidence as prices rise, not less.

In AI bubble regimes, investor internal monologue starts sounding like this:

> "This is generational."

> "I can't miss this."

> "Even if it's expensive, it's still right."

> "Traditional valuation doesn't apply to AI."

> "Productivity gains this time are actually real."

Some of these statements may even be true. The problem is that each of them disables a self-check. Each of them makes it harder to ask:

- If this company isn't the winner, does the technology still succeed through another path?

- Am I buying the technology, or am I buying the price?

- When this stock drops 40%, what specific fact will keep me holding?

- Am I using my own analysis, or borrowing conviction from the crowd?

Late-stage bubbles compress the time investors spend on questions like these. Survivors deliberately slow that compression down.

The third survival principle:

> The more confident you feel, the more questions you should be asking.

If your confidence is rising while your question count is dropping, you are in the exact psychological position that late-cycle bubbles exploit.

8. The AI Bubble Survival Playbook — Six Rules

Now move from principles to practice. These six rules, used together, do not guarantee outperformance. They materially improve the odds of staying in the market long enough to benefit when the real wealth-creation phase arrives.

Rule 1: Separate the technology from the price.

Your view on AI's long-term importance and your view on a specific stock's attractiveness are two separate decisions. The stronger your technological conviction, the colder you need to be on individual entry prices. Enthusiasm about AI is not a valuation input.

Rule 2: Expectations matter more than valuation multiples.

A stock at 40x earnings can still fall if consensus expectations were for 50x deserving. A stock at 20x can still fall if expectations were for 15x. The hard work is not the multiple — it's what's already priced in. Always ask "what specifically is expected?" before "is this cheap or expensive?"

Rule 3: Look at the supporting cast, not just the stars.

Power, cooling, electrical, automation, supply chain, specialized services. The companies the AI buildout cannot function without often offer better risk-adjusted returns than the obvious winners.

Rule 4: Reduce leverage.

Bubble regimes are high-volatility, high-news-flow environments. Leverage in these conditions amplifies mistakes more than it amplifies skill. The investors who blow up in bubbles usually did not blow up because their thesis was wrong. They blew up because leverage turned survivable losses into terminal ones.

Rule 5: Treat cash as optionality, not failure.

In bull markets, cash feels stupid. In bubble resolutions, cash is the scarcest asset — because it's the only thing that lets you buy dislocated quality. Cash during the bubble is future firepower. Framing it as "sitting out" misses the point. You're not sitting out. You're waiting for a moment that statistically always arrives.

Rule 6: Write down what you'll do if you're wrong.

Entry logic is easy when prices are rising. The real test is exit logic when prices are falling. Stop-loss rules, thesis-review triggers, position-size rules — all of these should be written before you need them, because emotion will prevent you from writing them during a drawdown.

9. The Real Opportunity Is After the Bubble, Not During It

Here is the uncomfortable truth most investors never process:

Surviving the bubble is not the goal. Being able to invest again after the bubble is the goal.

Railways survived the 1840s collapse. Internet survived the 2000 collapse. AI will likely survive whatever corrects next.

The question is not whether the technology continues. The question is whether you, the investor, are still in position to deploy capital when quality companies become cheap.

The historical pattern is remarkably consistent. Bubble-era investors who try to "perfectly escape" before the crash almost always fail — either by exiting too early and missing upside, or by exiting too late and losing the gains.

The realistic goal is different:

- Avoid terminal damage during the overheating phase

- Maintain cash and mental discipline through the correction phase

- Remain capable of buying surviving quality at better prices

This is where real wealth is generated in technology cycles. Not at the top. At the reset.

Apollo's analysis suggests that the AI buildout itself will take years — data center construction, power infrastructure, grid modernization. The technology won't disappear if prices correct. It will continue. The investors with preserved capital will simply own more of the survivors at better entry points.

Wealth in transformative technology cycles does not go to the investors who had the most conviction at the top. It goes to the ones who could still think clearly at the bottom.

10. The Single Sentence That Summarizes Everything

If this entire article had to compress to one sentence, it would be this:

> AI will likely transform the world.

> That fact alone does not automatically make any specific stock a good investment at any specific price.

If you genuinely internalize this, your investing behavior changes.

You become:

- More careful

- Slower to conviction

- More focused on cash flow

- Less reactive to narrative

- More willing to wait

These are the exact behaviors bubbles punish in the short term and reward over full cycles.

Surviving an AI bubble is not pessimism. It is structural optimism — believing in the technology's long-run importance enough to not overpay for it today.

The true optimist does not need to chase every short-term move. Their optimism is durable because it doesn't require exact timing. It only requires surviving long enough for the technology to fulfill its promise.

That is the posture that wins this cycle.

Self-Check Before Closing This Page

Before you leave, answer these eight questions honestly:

1. What am I currently buying — technology, or a specific stock at a specific price?

2. Is this company actually generating cash, or generating expectations?

3. Does today's price reflect strong execution, or flawless execution?

4. Am I holding this because of my own analysis, or the crowd's conviction?

5. If the market corrects 30%, does this company's financial structure survive?

6. If a drawdown arrives, am I positioned to buy more, or to be forced out?

7. Have I looked at the supporting cast, or only the obvious winners?

8. Does my investment plan include what I'll do when I'm wrong?

If any of these questions is uncomfortable to answer, that discomfort is probably the most useful signal you'll receive from this entire piece.

Next in The Mental Game:

Issue #003 will examine herd psychology in the social media era — specifically, how X, Reddit, and the endless flow of market commentary create new forms of conviction that feel like research but are actually crowd dynamics in faster cycles.

Related Reading

- The Mental Game #001: Why Bull Markets Make You Worse at Investing — The foundational psychology of why rising markets degrade investor skill

- NVTS Special Report — A supporting-cast AI infrastructure bet, not a star

For informational and educational purposes only. Not investment advice. The author has no position in any security mentioned. Always conduct your own research.

For the edge that cuts through the noise — Brutal Edge.

Share your analysis

Keep it data-driven. No investment advice.

- Keep it data-driven and respectful

- No investment advice (buy / sell / hold)

- No spam, promotion, or solicitation

- No profanity or offensive content

- Violations are automatically removed