Most 'Moats' Aren't Moats. Here Are the Five That Are.

The word moat gets used for almost any advantage a business has. Most of those advantages erode within five years. This week we isolate the five structural moats that actually hold — and apply them to five real businesses.

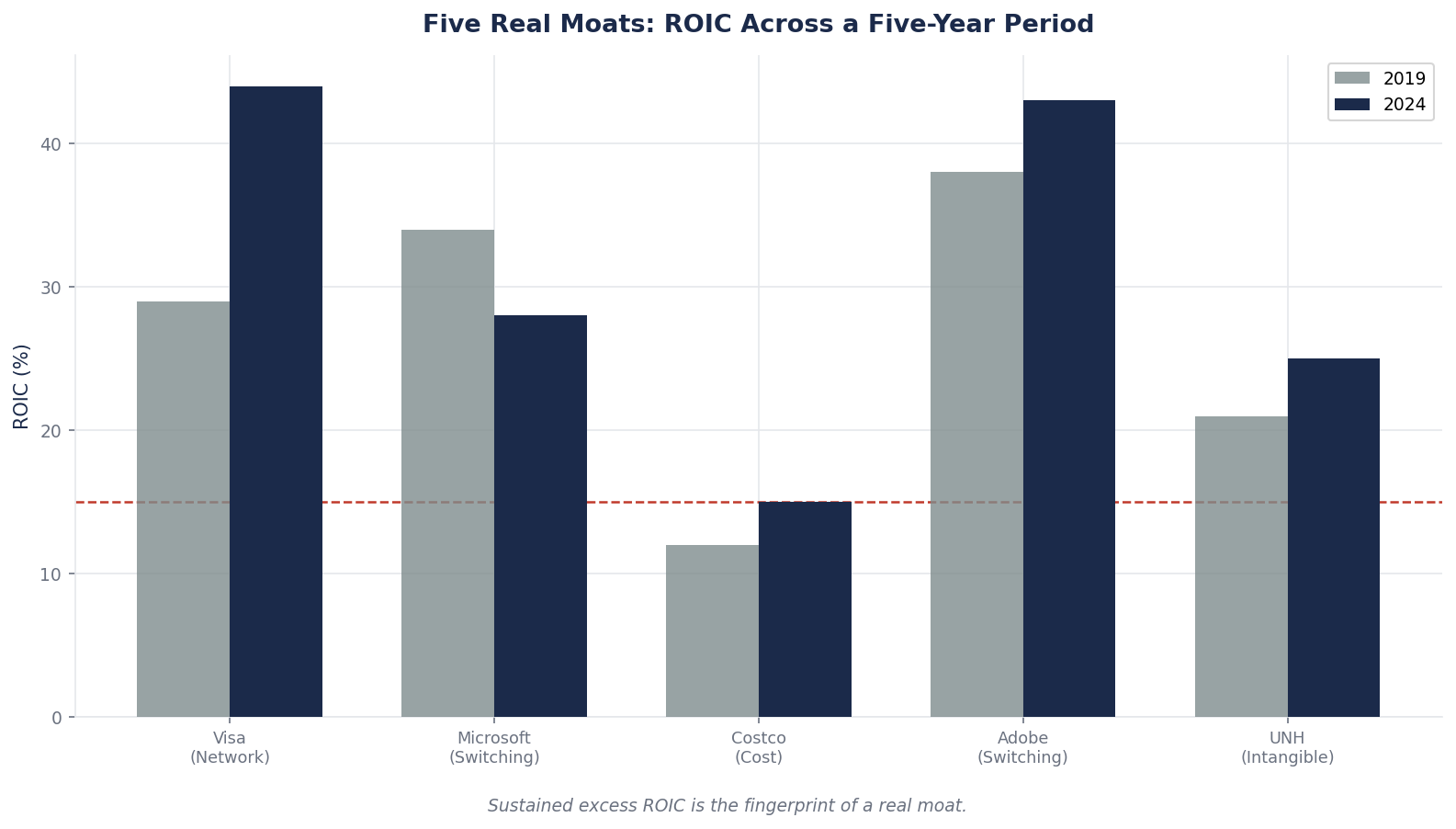

Five Real Moats

Walk into any investor conference and count how many times you hear the word "moat." It will be in the first five minutes. By the end of the afternoon you will have heard it applied to brand, to technology, to culture, to customer service, to execution speed, to management quality, to "network effects" that are not actually network effects, to "scale advantages" that are not actually scale advantages.

Nearly all of it is wrong. Not malicious — just imprecise. A moat is a very specific thing: a structural feature of a business that allows it to earn returns on invested capital above its cost of capital, for an extended period, without being competed away. That definition is narrower than most people realize. By that definition, most public companies do not have one. Most businesses described as "wide moat" in sell-side reports are competitive positions that will erode within a decade, not structural moats that compound for a generation.

This week we identify the five competitive advantages that actually qualify. Each comes with a concrete public-market example. Visa for network effects. Microsoft for switching costs. Costco for cost advantage. Adobe for intangibles. UnitedHealth for efficient scale. Every durable compounder in investing history is explained by one or more of these five, usually stacked on top of each other. If a company you own has none of them, it has no moat — no matter how good the product is or how well-liked the management team.

Core Framework: What a Moat Must Do

A real moat does three things simultaneously.

| Test | The Question | If the Answer Is No |

|---|---|---|

| Pricing | Can the business raise prices without losing significant volume? | Probably no moat |

| Returns | Are returns on invested capital consistently above cost of capital? | Probably no moat |

| Durability | Can a well-funded competitor replicate this within 3 years? | Probably no moat |

All three tests, not two out of three. A business can charge premium prices for a while on brand sizzle, but if returns on invested capital revert to cost of capital within five years, the brand was not a moat — it was a tailwind.

With that framework in mind, here are the five structural moats.

Moat 1: Network Effects — Visa

A network effect exists when each additional user makes the product more valuable to every existing user. The math compounds: doubling the users typically more than doubles the value, because every new participant creates incremental utility for everyone already there.

The cleanest public-market example is Visa.

Visa operates the largest payments network in the world. It processed roughly $17 trillion in total payment volume in fiscal 2025 and holds approximately 61 percent market share of global digital payments. The network has three sides — cardholders, merchants, and card-issuing banks. Each side reinforces the other two. More cardholders make merchant acceptance valuable. More merchant acceptance makes cardholders want Visa-branded cards. More volume lets Visa negotiate better terms with both sides, reinforcing its position.

Now look at the financial signature.

Visa — financial fingerprint of a real network moat

| Metric | Visa (recent) | Typical "good" business |

|---|---|---|

| Revenue (TTM) | ~$41.4B | — |

| Operating margin | ~65% | ~15–20% |

| Net margin (TTM) | ~50% | ~10–12% |

| ROIC (TTM) | ~32% | ~12% |

| ROIC vs 5-year WACC (~7.75%) | +24 percentage points | +3–5 points |

| Free cash flow conversion | >100% of net income | 70–85% typical |

A 65 percent operating margin and 32 percent ROIC in a business that has existed in roughly its current form for six decades is not management talent. It is structural. Visa does not manufacture anything, does not take credit risk, and does not hold the money. It operates a tollbooth on a network so large that duplicating it would cost more than Visa's entire market capitalization — and a duplicate would still have no volume on day one, because merchants and cardholders have no reason to move.

What Makes the Moat Real, Not Just a Tailwind

Notice what Visa's moat is not. It is not brand (though brand helps). It is not technology (Visa's infrastructure is reliable but not uniquely sophisticated). It is not customer service. It is the accumulated network itself — the physical fact that roughly 4 billion cards, 150+ million merchant locations, and 15,000+ financial institutions connect through it. A new entrant with a better product and ten billion dollars cannot win, because the moat is not the product. The moat is the users themselves, and you cannot buy them with marketing.

Where Visa's Moat Could Erode

Network effects are not invincible. They typically do not die from a direct attack — they die from a platform shift that makes the old network partially irrelevant. For Visa, the watch items are: regulatory caps on interchange fees (the US has active debates on this), central bank digital currencies that could route around card networks, and stablecoin-based merchant settlement. None of these has punctured the moat yet, but each is a plausible 10-year erosion vector. A moat that lasts forever is a story. A moat that lasts two decades while generating 30 percent returns on capital is an investment.

Moat 2: Switching Costs — Microsoft

Switching costs are the friction a customer experiences when trying to move from one provider to another. The friction can be financial, technical, procedural, or psychological. In every case, it makes the customer reluctant to leave even when the alternative is superior.

The cleanest public-market example is Microsoft.

The usual shorthand for Microsoft's moat is "Windows and Office." That is the 1990s version. The current version is much stronger: a Fortune 500 company running its entire operational stack on Microsoft — Azure infrastructure, Microsoft 365 productivity, Dynamics for operations, Active Directory for identity, Teams for communications, Copilot for AI — has effectively no exit path. Switching means retraining tens of thousands of employees, rebuilding integrations, migrating years of data, re-permissioning every system, and accepting months of productivity loss. A competitor might be 30 percent cheaper and 20 percent better. It does not matter at the scale of enterprise IT decisions.

Microsoft — financial fingerprint of a switching-cost moat

| Metric | Microsoft (TTM) | Pre-cloud MSFT (2010s) |

|---|---|---|

| Revenue (TTM) | ~$320B | ~$70B |

| Operating margin | ~44% | ~35% |

| Gross margin | ~69% | ~75% |

| ROE | ~35% | ~25% |

| Commercial RPO backlog | $625B (+110% YoY) | N/A |

| Azure YoY growth (most recent Q) | 39% | — |

The number that tells the moat story best is not the revenue or the margin. It is the $625 billion commercial remaining performance obligation backlog reported in Q2 FY26 — a 110 percent year-over-year increase. That is $625 billion of signed, contracted, not-yet-delivered revenue. Customers are not just using Microsoft; they are signing multi-year forward commitments in staggering volume. Those commitments are voluntary evidence of the switching cost. The customer has quantified, in money, how expensive it would be to leave.

How Switching Costs Show Up in Retention

For enterprise software, the relevant metric is not "customer retention" (almost everyone retains when contracts auto-renew). It is net revenue retention — how much the average customer spends this year versus last. Microsoft's commercial cloud businesses consistently run NRR in the 115–125 percent range. That means the average customer not only does not leave, but spends materially more each year. That pattern is impossible without genuine switching costs: churn-neutral growth requires the customer to be locked in by something beyond love.

Where Microsoft's Moat Could Erode

Switching costs erode when new technology reduces the friction. Cloud-native competitors broke the switching-cost advantage of legacy on-premise vendors in the 2010s. API-first and agent-based architectures are currently eroding some parts of the moat — it is now theoretically easier to mix-and-match productivity tools via AI agents than it was in a traditional integrated stack. Microsoft's counter is to be the default AI layer (Copilot) across its existing stack, which works as long as the agent layer does not disintermediate the underlying apps. This is a live, real-time test, and the result is still five to ten years out.

Moat 3: Cost Advantage — Costco

Cost advantage is the most abused moat word. Being big is not a moat. Being big in a way that gives you a structural cost advantage over any realistic competitor is a moat.

The cleanest public-market example is Costco.

Costco's moat is not scale alone — Walmart is much larger and has weaker unit economics. The moat is the specific combination of three things: (1) a limited-SKU warehouse model (roughly 4,000 items versus 50,000+ at a typical grocer) that maximizes per-SKU purchasing leverage, (2) a membership fee that subsidizes merchandise margins to near-zero, and (3) a Kirkland-branded private-label strategy that captures margin the vendors would otherwise keep.

Costco — financial fingerprint of a cost-advantage moat

| Metric | Costco (FY2025) | Typical US retailer |

|---|---|---|

| Revenue (FY2025) | $269.9B | — |

| Membership fee revenue | $5.3B (+10% YoY) | — |

| Gross margin | ~11% | ~25–35% |

| Operating margin | ~3.1% | ~4–6% |

| ROIC | ~19.9% | ~11% |

| Paid memberships | ~81M | — |

| Worldwide renewal rate | 89.8% | — |

| US/Canada renewal rate | 92.3% | — |

| Executive membership penetration of sales | 74.2% | — |

Look at the apparent paradox. Costco has a lower gross margin than Walmart and Target. It has lower operating margins than most grocers. By standard retail metrics, it looks weaker than peers. And yet its ROIC is nearly double the retail industry average.

The resolution is the membership fee. Costco's merchandise business effectively runs at break-even on purpose. Merchandise margins compress so that prices can be lower than any competitor can match, which drives membership signups and renewals, which generates approximately $5.3 billion in pure-profit membership fees — money that flows to the bottom line at essentially 100 percent margin. Those fees represent less than 2 percent of total revenue but approximately 52 percent of operating income in any given year.

Why Competitors Cannot Copy It

A competitor cannot neutralize this moat by raising prices or cutting costs — those are the wrong levers. They would have to replicate the entire model: limited SKUs, membership warehouse, private-label scale, and most critically, the 89.8 percent renewal rate that represents three decades of accumulated customer trust. Amazon Prime is the closest thing anyone has built to compete, and Costco's membership renewal rate is still meaningfully higher. A new entrant with $20 billion could open warehouses but could not build the trust. The cost advantage is not on the shelf. It is in the member's wallet and the member's habit.

Where Costco's Moat Could Erode

Three plausible erosion paths. Online grocery delivery at scale with superior convenience economics (Amazon Fresh, Instacart) could dilute the membership value proposition. E-commerce pricing transparency could erode the "Costco is always the cheapest" habit — shoppers may compare prices on each purchase rather than default-trusting the warehouse. Demographic shift toward smaller households could reduce the appeal of bulk purchasing. None of these has pushed renewal rates down meaningfully yet. Watch the renewal rate quarterly. It is the single cleanest signal of moat health.

Moat 4: Intangible Assets — Adobe

Intangible assets are legally or practically defensible positions that are hard to acquire, hard to replicate, and hard to compete against. Three subtypes matter most: patents and regulatory approvals, brand-and-standards, and proprietary data or process.

The cleanest public-market example is Adobe.

Adobe's Photoshop, Illustrator, Premiere, and Acrobat are not protected by patents in any meaningful way. Their moat is different — they are the industry standard for professional creative work. Every design school teaches on them. Every agency pipeline assumes them. PDF was invented by Adobe and remains a de facto global document standard. When a creative professional joins a new company, the assumption is that they know these tools; the company does not need to hire for fluency, because fluency is a given.

Adobe — financial fingerprint of an intangible-asset moat

| Metric | Adobe (TTM) | Industry average (SaaS) |

|---|---|---|

| Revenue (TTM) | ~$23B | — |

| Gross margin | ~88% | ~70–75% |

| Operating margin | ~35% | ~15–20% |

| ROIC | ~25%+ | ~12% |

| Creative Cloud retention | 95%+ | 85–90% typical |

| Pricing power | Consistent annual increases absorbed by customer base | Competitive discounting common |

The clearest moat signal is pricing power. Adobe has raised subscription prices multiple times over the past decade. Customers complain loudly. Almost none actually leave. A design studio that switched off the Adobe stack to save $600 per user per year would face re-training, client-compatibility, and workflow-rebuild costs in the tens of thousands. The economics of leaving are unambiguous: stay and pay.

How Intangible Moats Are Structured

Adobe's moat is three layers deep:

1. Standards layer: PDF as a global document standard. Uncountable assets already live in Adobe formats. A new entrant does not just compete with Adobe software; it competes with decades of installed file content.

2. Education layer: Every design curriculum, every tutorial library, every YouTube channel that teaches creative workflow assumes Adobe tools. Switching off Adobe means being professionally illiterate on any job site.

3. Ecosystem layer: Third-party plugins, presets, font libraries, and integration tools built around Adobe. A competitor with better core software still lacks the ecosystem surrounding it.

Each layer reinforces the others. Removing one does not collapse the moat — it compresses it. Removing all three takes a decade-plus of sustained competitor investment, and even then the embedded Adobe content does not unmake itself.

Where Adobe's Moat Could Erode

The erosion vector is AI-native creative tools. Midjourney, Runway, and emerging generative AI platforms are doing creative work that bypasses the Adobe pipeline entirely. If the professional workflow shifts from "create in Photoshop" to "prompt in Midjourney, refine in Runway, export to client," Adobe's industry-standard position is partially disintermediated. Adobe's response (Firefly, generative features inside Creative Cloud) is meaningful but its competitive position is genuinely contested for the first time in two decades. Watch Creative Cloud retention over the next three years — it is the canary.

Moat 5: Efficient Scale — UnitedHealth

Efficient scale is the rarest moat and the hardest to recognize. It exists when a market is just large enough to support one or two profitable competitors, and not a third. The sign of efficient scale is not growth — it is the persistent absence of new competition despite attractive returns over decades.

The public-market example is UnitedHealth.

UnitedHealth operates in US health insurance and healthcare services at a scale no competitor matches. UnitedHealthcare alone serves approximately 50 million people. Optum, its healthcare services arm, touches roughly 100 million lives. Combined, UnitedHealth is one of the largest private healthcare operators in the world, with 2025 revenues of $447.6 billion.

The moat is not that UnitedHealth is better at health insurance (margins in the industry are structurally low across all players). The moat is that US health insurance is a regulated, multi-trillion-dollar industry with enormous fixed costs — compliance infrastructure, provider networks, actuarial capability, claims processing platforms — where scale dramatically reduces per-member cost. A new entrant trying to build a rival to UnitedHealthcare would need to spend tens of billions of dollars and roughly a decade to assemble equivalent provider networks. No venture-backed startup has successfully done it. The market simply does not support a fourth or fifth large national player.

UnitedHealth — efficient scale financial signature

| Metric | UnitedHealth (FY2025) | Note |

|---|---|---|

| Revenue (FY2025) | $447.6B | Largest private US healthcare operator |

| Members served (UnitedHealthcare) | ~50M | Largest private insurer in US |

| Medicare Advantage members | Largest share in US | Key segment |

| Operating margin (consolidated, 2025) | ~5–6% (compressed from prior years) | Persistent low-single-digit segment margin, but scale wins |

| UnitedHealthcare segment op margin (2025) | 2.7% | Sharp compression from 5.2% in 2024 |

| Adjusted op earnings (2025) | $21.7B |

A Moat Under Active Stress

UnitedHealth is the instructive example for a second reason: efficient scale moats can be genuinely tested. In 2025, UnitedHealthcare's segment operating margin compressed from 5.2 percent to 2.7 percent — a nearly 50 percent decline — as Medicare Advantage reimbursement rates were tightened under Biden-era regulatory changes and medical cost trends accelerated. The medical care ratio rose from 85.5 percent to 88.9 percent. Earnings from operations in the core insurance segment fell from $15.6 billion to $9.4 billion. The company guided 2026 to its first revenue contraction in decades.

Does this mean UnitedHealth has no moat? No. It means UnitedHealth has an efficient-scale moat that is regulated, and regulators have narrowed the margin structure. The market position is intact — UnitedHealth still has 50 million members, still has the largest Medicare Advantage footprint, still has Optum as a growing counterweight. But the moat's yield has compressed. The returns-on-capital test for a moat is failing temporarily even while the structural position holds.

This is a useful lesson. Efficient scale protects you from new competition. It does not protect you from regulation, demographic shifts, or cost pressures inside your industry. No moat does.

Where Efficient Scale Moats Break

They break when the market grows enough to support additional competitors, or when regulation changes the unit economics. For US health insurance, regulation is the primary risk. For pipelines, railroads, or port terminals, the usual risk is technology enabling a substitute (alternative transport modes, new energy sources, etc.). In every case, the moat protects only within the existing rule set of the industry. Change the rules, and efficient scale becomes inefficient.

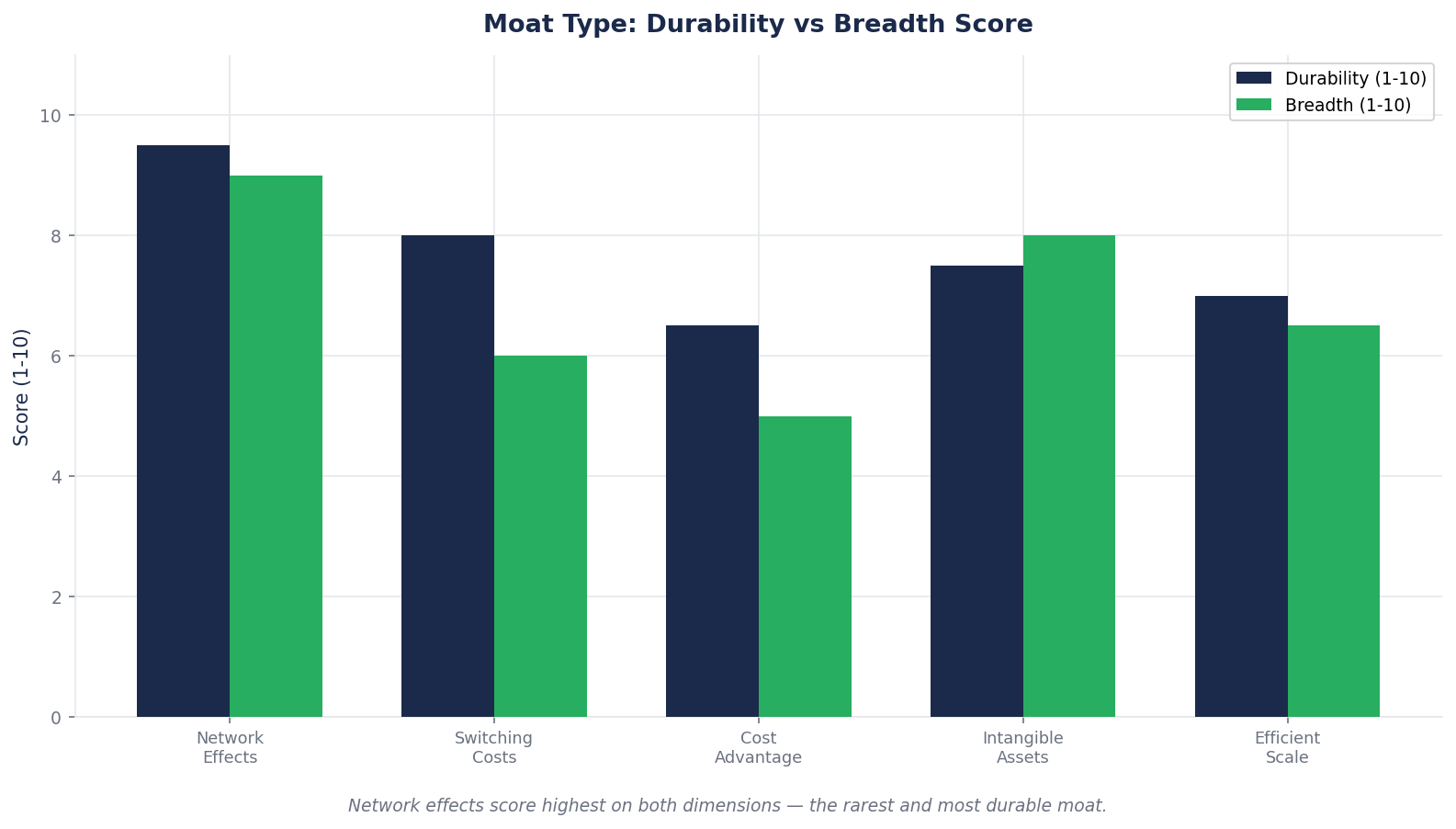

Putting It Together: The Moat Classification Table

Here is how the five moats stack on the three tests established at the start.

| Moat Type | Example | Durability | Scale Reinforcement | Typical ROIC |

|---|---|---|---|---|

| Network effects | Visa | Very high | Very strong | 25–35% |

| Switching costs | Microsoft | High | Strong | 20–30% |

| Cost advantage | Costco | Medium–high | Strong | 15–22% |

| Intangible assets | Adobe | Medium–high | Medium | 20–30% |

| Efficient scale | UnitedHealth | High (rule-set dependent) | N/A (self-limiting) | 12–20%* |

*UnitedHealth's consolidated ROIC has historically run 14–18 percent. 2025 compression brings it lower temporarily — watch 2026–2027 recovery or persistence.

The Six Things People Call Moats That Aren't

For every real moat there are several imitations. Here are the most common.

| Claimed "Moat" | Why It Usually Isn't One |

|---|---|

| "Great management" | Management can leave. Advantages that disappear when a CEO retires were never structural. |

| "First-mover advantage" | Being first often costs more than it helps. Second movers with deeper pockets routinely overtake first movers. |

| "Superior technology" | Unless protected by patents or deep scale, technology advantages rarely last more than 3–5 years. |

| "Customer service" | Replicable with enough investment. Rarely produces sustained pricing power on its own. |

| "Proprietary AI models" | Most current model advantages are 12–24 months. The moat, if any, is in data access or distribution — not the model weights. |

| "Ecosystem" | Often used interchangeably with "network effect" but usually means "we have some integrations." Real ecosystems have network-effect math behind them. |

The test for any claimed moat: if I had $5 billion and five years, could I neutralize this advantage? If the answer is yes, it is not a moat. It is a competitive position — which is valuable, but different.

Case Study: Stacking Moats

The most powerful businesses do not have one moat. They have two or three, stacked.

Microsoft has switching costs (enterprise contracts, training, integrations) plus network effects (Office compatibility across the global workforce, Azure's partner and ISV ecosystem) plus scale economics (R&D spend of over $30B per year — larger than most competitors' total revenue).

Any one of those would be a meaningful moat. Together, they produce a business that has been effectively impossible to displace for two decades, despite dozens of well-funded attempts. This is why Microsoft's ROIC has stayed above 25 percent through multiple CEO transitions, technology platform shifts, and regulatory interventions.

Typical durability profiles:

| Moat Profile | Typical ROIC | Typical Duration Above Cost of Capital |

|---|---|---|

| Three stacked moats | 25–40% | 20+ years |

| Single strong moat | 15–25% | 10–15 years |

| Weak or no moat | 5–10% | 3–5 years |

The magic is in the stacking. A business with three reinforcing moats does not just have 3x the protection. It has compounding protection, because each moat buys time for the others to deepen.

The Common Mistake: Mistaking Tailwind for Moat

Here is the error that costs intermediate investors most.

A business is growing revenue at 30 percent, gaining share, posting expanding margins. You look at the results and conclude it has a strong moat. You pay 25x revenue based on that conviction.

But the business may not have a moat at all. It may simply be riding a strong end-market tailwind — a category growing 40 percent annually, where every participant looks like a winner. When the tailwind fades, the absence of a real structural advantage shows up fast: margins compress, competition intensifies, share stops growing.

The fix is to separate the two questions explicitly. First: how fast is the underlying market growing? Second: within that market, does this specific business have a structural reason to capture a disproportionate share?

A business with a strong moat in a flat market will outperform a business with no moat in a booming market, over a full cycle. The booming market creates a lot of temporary "winners" who turn out to be riders rather than owners of the advantage.

Write down, for any business you are about to buy, whether its recent success is explained by: (a) a real moat, (b) a temporary industry tailwind, or (c) some combination. You will be wrong sometimes, but the exercise forces you to stop confusing the two.

What to Watch

Three signals tell you whether a claimed moat is real.

Watch returns on invested capital over a full cycle. A real moat shows up as ROIC above cost of capital through both good and bad years. A business that earns 30 percent ROIC in a boom and 4 percent in a recession does not have a moat — it has cyclical leverage. The test is what the number looks like at the bottom of the cycle, not the top. UnitedHealth's current margin compression is exactly this stress test, in real time.

Watch competitive entry. If well-funded competitors have tried to enter the market in the last five years and failed, there is probably a real moat. If competitors are still raising capital confidently because the market "has room for multiple winners," the moat thesis is untested. In US health insurance, startup disruptors keep emerging and keep failing to scale — that failure is the moat evidence.

Watch pricing behavior. A business with a real moat can raise prices ahead of inflation without losing meaningful volume. Adobe raises subscription prices every few years. Costco raised its membership fee in September 2024 — the first increase since 2017. Visa periodically adjusts interchange. None of these losing volume in response. That pass-through is one of the cleanest real-time signals of moat strength available in public equity markets.

Brutal Edge Coverage Integration

This week's framework maps directly onto our coverage:

- Microsoft Deep Dive (BEAF 81/B+) — the switching-cost analysis quantified through Commercial RPO, net revenue retention, and the AI-era stress test. The moat decomposition in that report applies the exact framework built here.

- Physical AI Sector Report — covers the emerging moats in AI infrastructure (NVIDIA platform effects, hyperscaler switching costs, data network effects in training), and which AI "moats" qualify under the three-test framework and which are still tailwinds masquerading as moats.

- NVDA Deep Dive (BEAF 83/B+) — a case where network effects (CUDA ecosystem) and switching costs (developer training, framework lock-in) stack with scale economics. Useful for seeing the exact pattern Microsoft exhibits in a different industry.

- TSLA Deep Dive Rev.2 (BEAF 58/C+) — the counterpoint. Tesla's frequently-claimed moats (brand, FSD data lead, Supercharger network) are systematically evaluated against the three-test framework. Several fail. The score reflects exactly that gap.

For additional frameworks, see our Deep Dive archive.

Looking Ahead

Next week we go after a harder question: even the strongest moats eventually weaken. Some last decades. Some last a century. But none of them are truly permanent. How do you tell when a moat is starting to break, while the financial statements still look fine? We take Intel — the single most instructive public-market moat-erosion case of the last 20 years — and trace what happened from 2005 to 2026 year by year. That timeline separates investors who get into great businesses early from the ones who get out too late.

For now, sit with this week's lesson. A moat is not a brand, not a relationship, not a product, not a culture. A moat is a structural feature of the business that makes competition mathematically difficult for an extended period. Five of them qualify. Everything else is weather.

Brutal Edge. Frameworks over forecasts. Signal over noise.

Disclaimer. Brutal Edge is an independent investment research platform. This report is published for educational and informational purposes only and does not constitute investment advice, a recommendation to buy or sell any security, or an offer to transact in any financial instrument. All valuations, forecasts, and opinions are the analyst's own and are subject to change without notice. Past performance does not guarantee future results. Readers should conduct their own due diligence and consult a qualified financial professional before making investment decisions.

Educational content only. Not investment advice. Always do your own research.