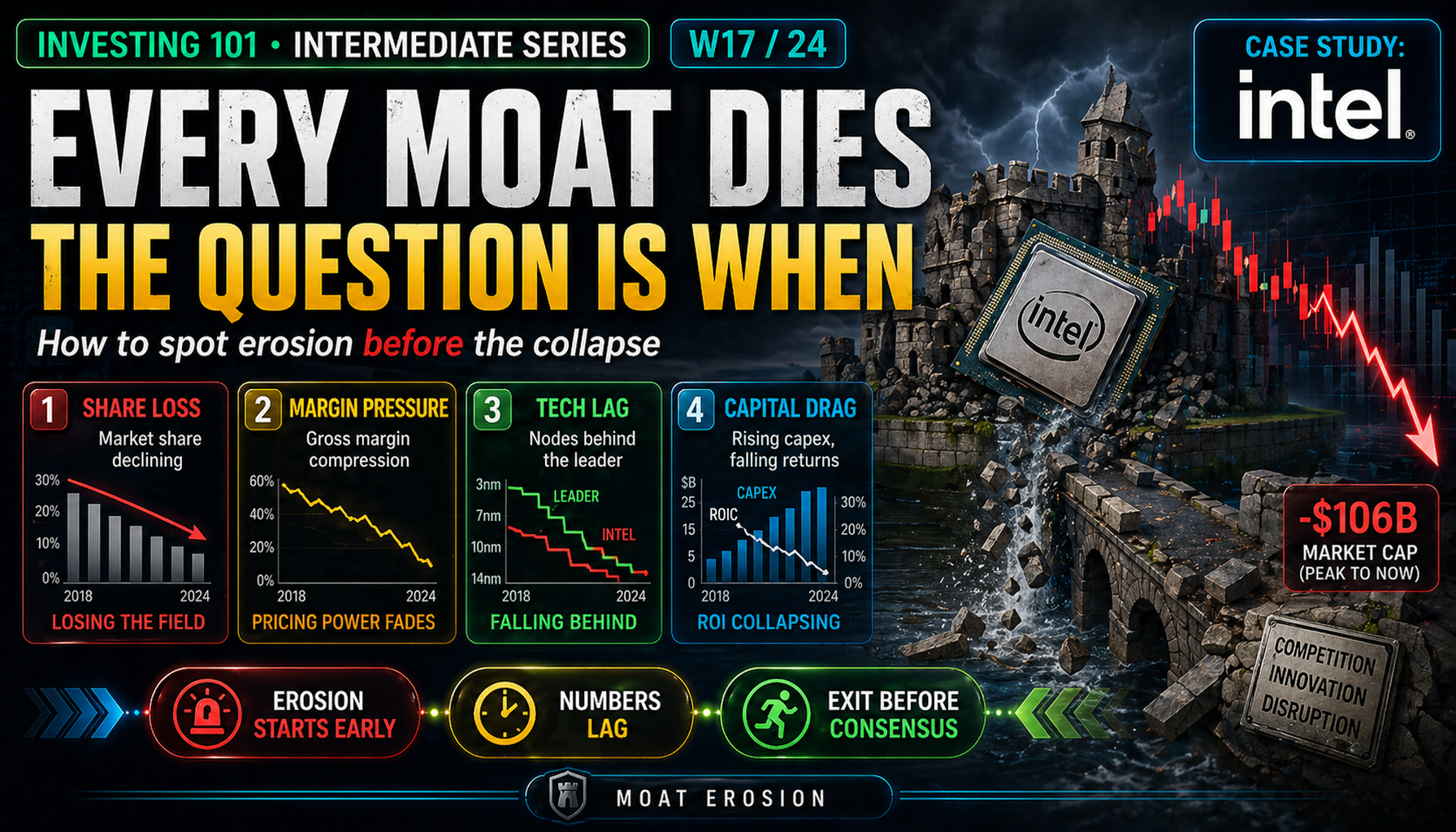

Every Moat Dies. The Question Is When.

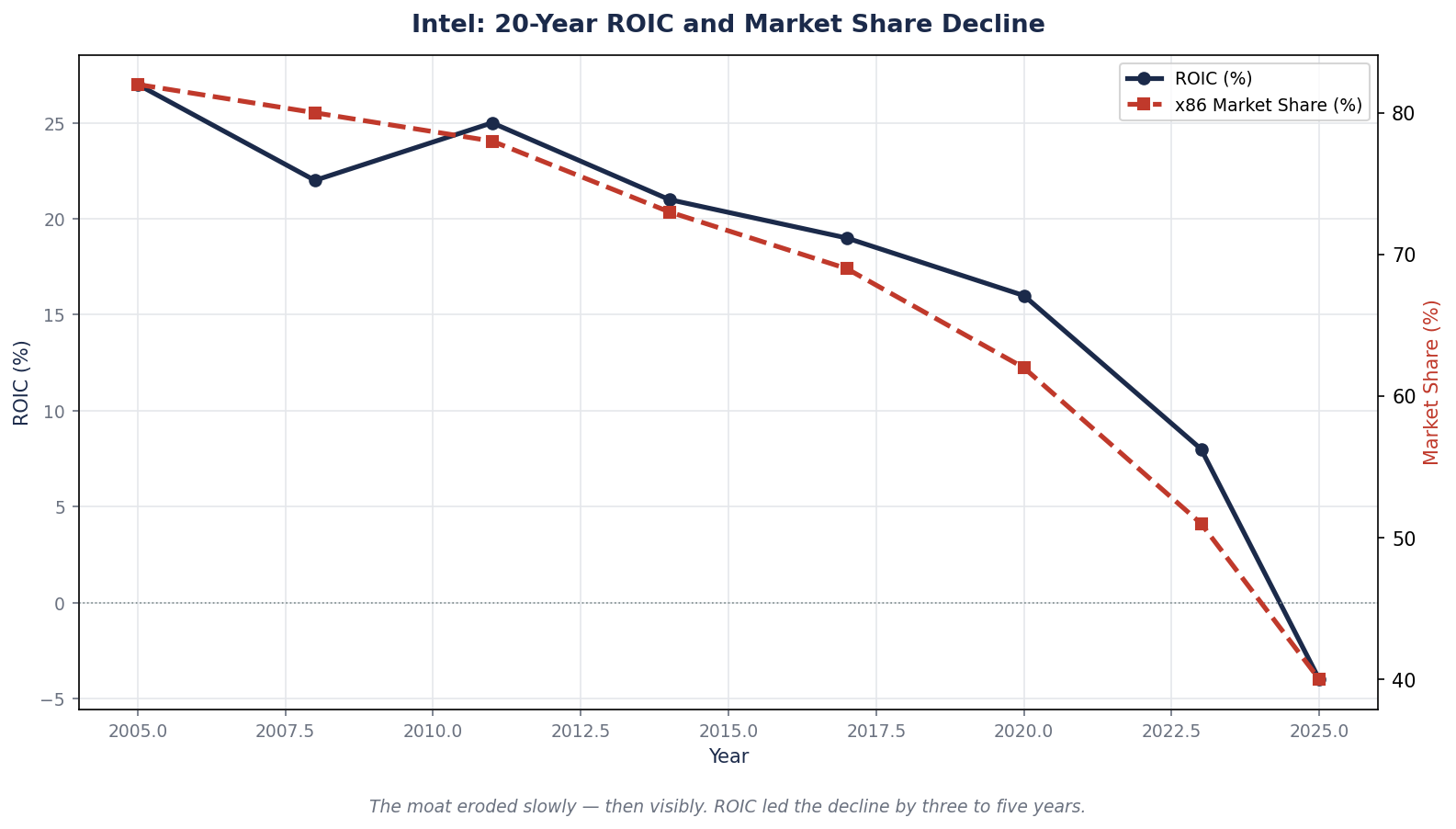

In 2005, Intel dominated CPUs with a near-monopoly and 25%+ returns on invested capital. By 2024, the stock had underperformed the S&P 500 by more than 500 percentage points. This week we follow the exact sequence of moat erosion — and show how to spot it early in a company you hold today.

Moat Erosion

Last week we identified the five structural advantages that actually behave like moats. This week we have to accept an uncomfortable truth about all of them.

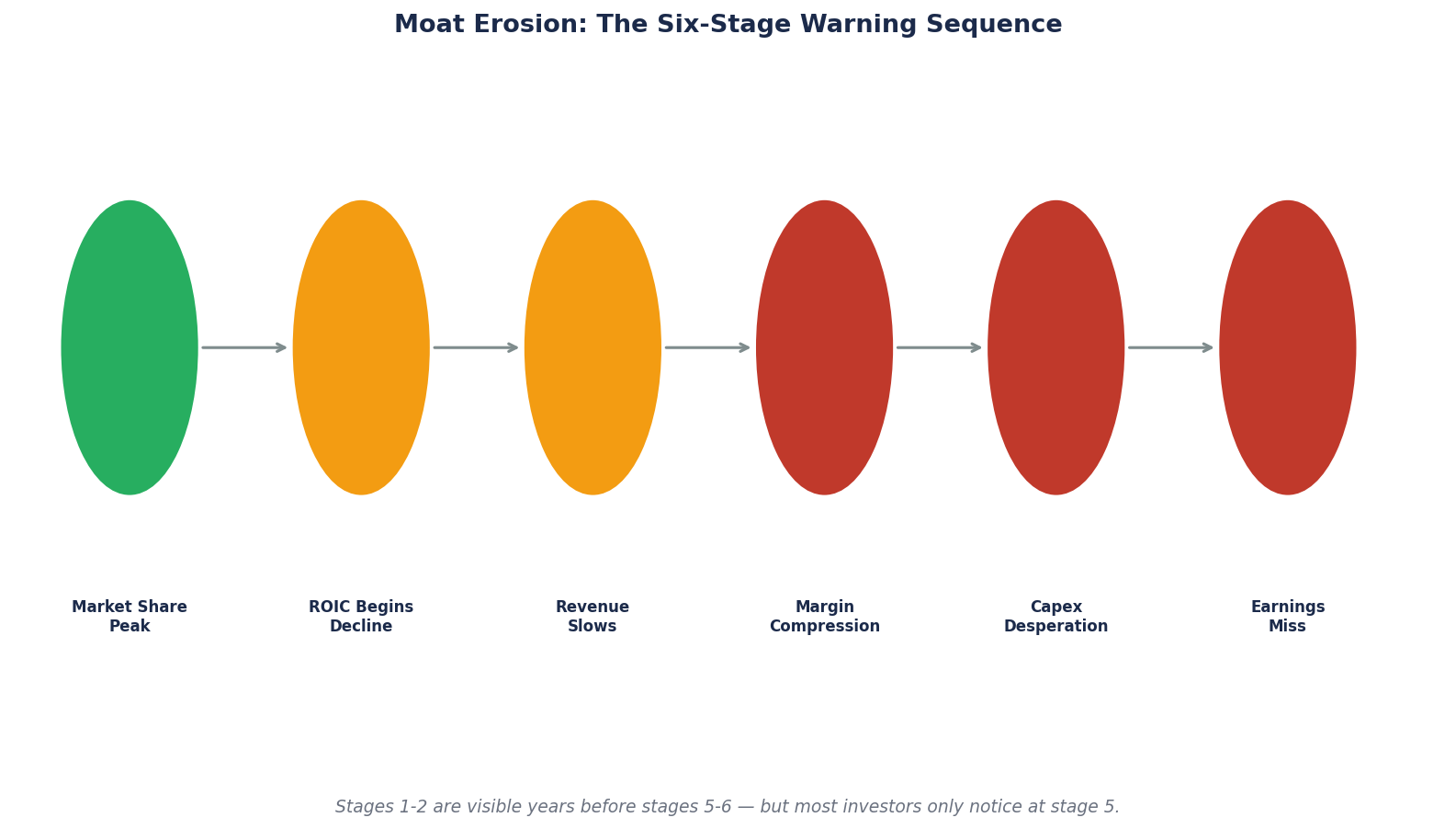

Every moat eventually weakens. Most do not collapse overnight — they erode, slowly, in ways that are visible years before the financial statements catch up. The best ones last 30 years. The greatest last 50. None are truly permanent. An investor who believes otherwise will eventually hold a business through a transition that the market quietly priced in long before the income statement showed it.

The skill is not predicting that a moat will die. It is recognizing the early signals of erosion while the reported numbers still look fine, so that you can exit — or at least stop adding — before the collapse becomes consensus. This skill is worth more than most stock-picking skills combined, because the largest investor losses come not from picking bad companies but from holding great companies too long after they stopped being great.

This week we examine the single most instructive case in modern public-market history: the twenty-year erosion of Intel's CPU moat, from dominance in 2005 to existential crisis in 2024, to an uncertain recovery bet in 2026. Every stage of the erosion had visible signals. Investors who read them captured different outcomes than investors who did not.

Core Framework: The Four Paths of Moat Erosion

Moats rarely die from a single event. They erode along one of four paths, often stacking on top of each other.

| Erosion Path | How It Works | Typical Timeline |

|---|---|---|

| Technology disruption | A new technology resets the cost or performance curve | 5–15 years |

| Platform shift | The underlying market migrates to a different form factor or delivery | 3–10 years |

| Regulatory change | New rules alter the unit economics or force structural separation | 1–5 years |

| Internal decay | Execution failures compound, eroding the advantage from within | 5–20 years |

Each path has a different rhythm. Technology disruption is usually the slowest — R&D cycles and capex scale mean it takes years for a better technology to reach parity at scale. Platform shifts are faster because end-user adoption can accelerate once a new form factor crosses a threshold. Regulatory changes are the fastest, sometimes cutting margin structures in a single year. Internal decay is the quietest and often the most dangerous — it looks like management issues for years before anyone calls it a moat problem.

Intel's story is instructive because it has been affected by all four, in sequence, over two decades.

The Peak: Intel in 2005

In 2005, Intel had one of the strongest moats in public equity markets. Consider the snapshot.

Intel — 2005 financial fingerprint

| Metric | 2005 |

|---|---|

| x86 CPU market share (client + server, combined) | ~80% |

| Operating margin | ~31% |

| ROIC | ~25–27% |

| Manufacturing leadership | Clear — 65nm node ahead of every competitor |

| Direct competitors with viable roadmap | 1 (AMD, much smaller) |

| Installed software base optimized for x86 | Nearly 100% of PC and server software |

Intel had network effects (the entire software ecosystem was written for x86), switching costs (enterprises had built procurement and support around Intel platforms for decades), cost advantage (manufacturing scale), and scale economies (R&D spend larger than competitors' total revenue). Multiple moats stacked. By the three-test framework from last week, this was a textbook moat business.

An investor in 2005 could reasonably have concluded that Intel's moat would persist for at least another decade. That conclusion would have been correct — in fact, Intel remained highly profitable through roughly 2015. But the erosion was already starting, in a signal most investors dismissed.

2005–2010: The First Warning (Missed)

In 2007, Apple launched the iPhone. The CPU inside it was not made by Intel. It was an ARM-based chip manufactured by Samsung, designed around an architecture optimized for low power consumption rather than raw performance.

At the time, this was not seen as a threat to Intel's core business. PCs and servers still used x86. iPhone sales were initially small. Intel itself made a strategic decision — documented in later interviews with Paul Otellini — to decline Apple's request that Intel manufacture the iPhone CPU, because the margin structure did not meet Intel's hurdle rate. That decision is now taught in business schools as one of the most expensive strategic errors in corporate history.

What an investor should have noticed (but most did not):

The issue was not that Intel lost one product. The issue was that a new platform was emerging outside Intel's moat — a category of computing that ran on a fundamentally different architecture (ARM) and a fundamentally different manufacturing approach (fabless design, contract manufacturing). Every ARM-based chip sold was a software developer and a device user who was now part of a non-Intel ecosystem.

Through 2010, mobile computing grew explosively. Intel shipped a few attempts at mobile chips (Atom, Medfield) but never achieved meaningful share. The installed base of ARM-compatible software and devices grew by orders of magnitude. Intel's moat was not shrinking — its absolute x86 position was fine — but the addressable market protected by the moat was being contested by a parallel track that Intel did not control.

This is the first lesson of moat erosion: the moat did not weaken. The market around it moved.

2010–2018: The Quiet Decade

Through most of the 2010s, Intel's financial statements looked healthy. Revenue grew from $44B (2010) to approximately $71B (2018). Margins stayed elevated. PC and server markets continued to drive the core business. For an investor looking only at the numbers, Intel appeared to be compounding successfully.

But four erosion signals were building in the background:

1. Manufacturing cadence slipping. Intel's historic advantage was process leadership — each new node (the "tick-tock" model) roughly every two years. The 14nm node took significantly longer than plan. The 10nm node, originally scheduled for 2016, suffered multi-year delays. Meanwhile TSMC — Intel's contract-manufacturing competitor — was closing the gap.

2. AMD restructuring. AMD was widely viewed as a failing competitor through most of the decade. In 2014, Lisa Su became CEO. Between 2014 and 2017, AMD reorganized around a new x86 architecture (Zen), outsourced manufacturing to TSMC, and prepared a generation of processors that would compete at parity with Intel for the first time in a decade.

3. Apple silicon development. Apple was quietly building an in-house chip team. The iPad switched to Apple-designed A-series chips in 2010. By 2018 industry reports widely discussed the eventual transition of Mac computers from Intel to Apple Silicon. This was a direct, announced-in-advance threat to approximately $4–5B of Intel's annual revenue.

4. Cloud custom silicon. Amazon began developing Graviton (ARM-based data center chips) in 2015. Google started shipping TPUs. By 2018, every major hyperscaler had an internal silicon program aimed at reducing dependence on Intel CPUs. None of these programs was large yet. All of them were explicit moat attacks.

What the Financials Still Showed (and Why It Misled)

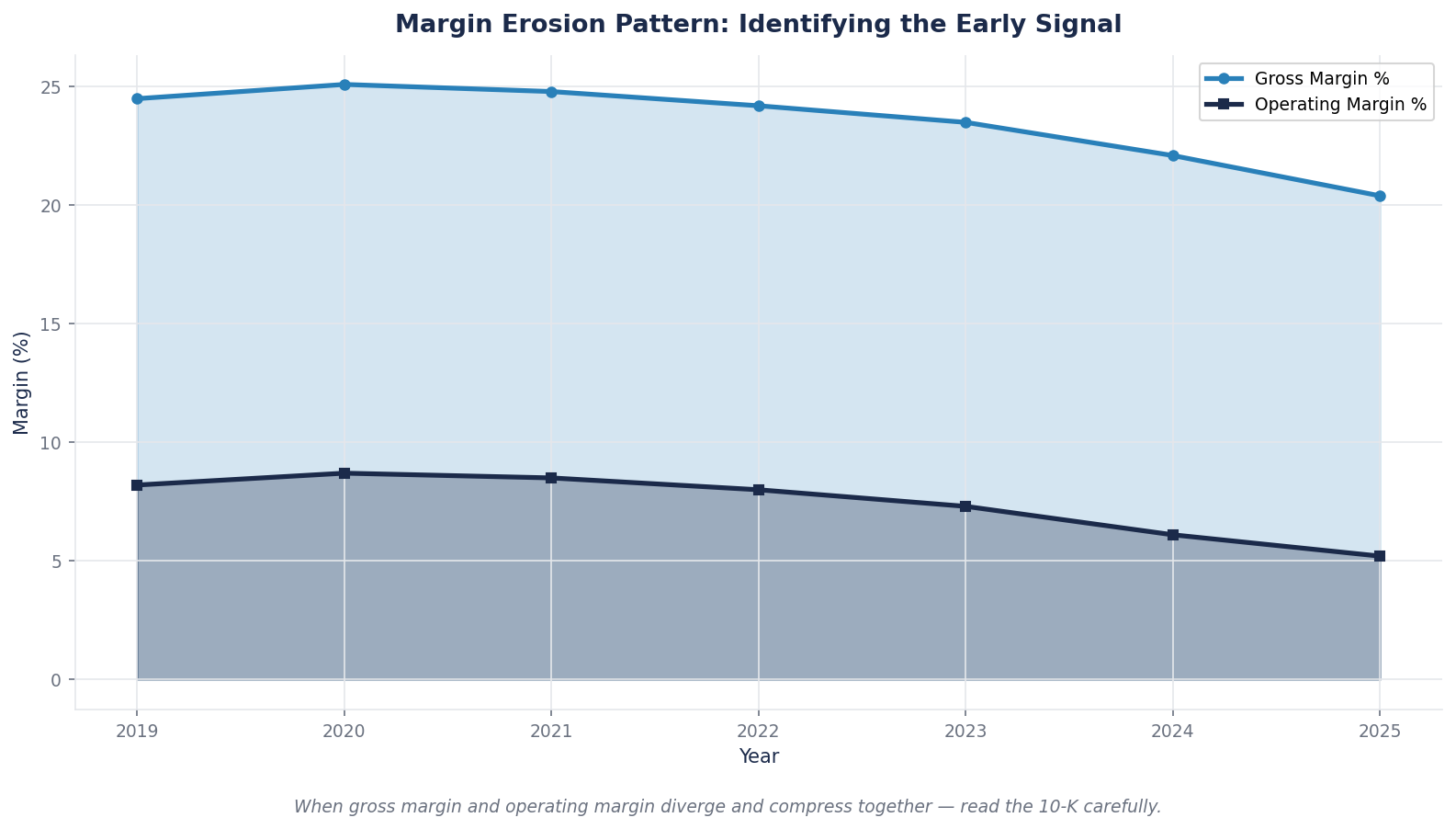

Through 2018, Intel's reported numbers continued to look strong. Operating margin remained above 30 percent. Revenue was growing. Dividends and buybacks were generous. An investor reading only the income statement would see no moat erosion yet.

This is exactly the window where moat erosion becomes visible to readers of the business but invisible to readers of the numbers. By the time the numbers show it, the erosion has already been running for a decade. The early warning is in market share trends, competitive announcements, and strategic posture — not in margin history.

2018–2022: Market Share Starts to Move

In 2018, AMD launched the second-generation Zen architecture (Ryzen 2). The performance and price-to-performance ratios were genuinely competitive with Intel for the first time since ~2006.

In 2019, AMD's EPYC server chips started winning major data center deployments. Hyperscalers began buying EPYC alongside Intel Xeon. By 2022, AMD had captured roughly 18% of the server CPU market — up from under 2% in 2016.

Apple announced the M1 in November 2020. Every Mac sold from late 2020 onward used Apple Silicon instead of Intel. Approximately 10% of Intel's premium CPU volume was gone within 18 months.

In 2021, Pat Gelsinger returned to Intel as CEO and announced IDM 2.0 — a strategic pivot to become both a chip designer and a contract foundry. This was an acknowledgement that the chip design business alone could no longer fund the manufacturing business, because volume had been lost to ARM-based alternatives and to AMD.

Intel's signal shift became undeniable:

| Metric | 2018 | 2022 |

|---|---|---|

| Server CPU market share (vs AMD) | ~96% | ~82% |

| Client CPU market share (vs AMD) | ~85% | ~74% |

| Manufacturing process vs TSMC | Roughly parity | Clearly behind |

| Operating margin | ~33% | ~22% |

| ROIC | ~25% | ~13% |

The financials had finally caught up to the reality. The ROIC test — above cost of capital — was narrowing. The moat was no longer a high-return compounder. It was a defensive position.

2022–2024: The Acceleration

This is the phase where investors who had held Intel through the 2010s often realized what had happened too late.

- 2022: Intel's operating income fell 60% year over year as inventory corrections hit and market share losses compounded.

- 2023: Intel's foundry division (the contract-manufacturing arm of IDM 2.0) began reporting standalone segment losses in the billions of dollars.

- 2024: MPU market share fell to 65.3% — the lowest since 2002, a 22-year low. The foundry segment lost approximately $13.4 billion for the year. Intel cut its dividend by 65% and announced plans to lay off ~15,000 employees (~15% of workforce). The stock fell more than 50% from 2021 highs.

- End of 2024: Pat Gelsinger departed as CEO. The board's external communication pivoted from "IDM 2.0 is on track" to "we are evaluating strategic alternatives for the foundry business."

The Classic Pattern

Read that timeline carefully. The earliest moat-erosion signals appeared in 2007 (iPhone / ARM). The financial damage did not become undeniable until 2022. That is a 15-year lag between when the moat started weakening and when the reported numbers made the weakening obvious.

An investor who owned Intel from 2005 and sold in 2020 still made money — dividends plus modest capital appreciation. An investor who owned from 2005 and held through 2024 gave most of it back. The difference was not in the entry decision. It was in the exit decision.

2025–2026: The Recovery Bet

Intel's story did not end in 2024. In late 2025, 18A — Intel's first truly competitive manufacturing node in years — entered volume production. In February 2026 the US government took an equity stake in Intel, framing domestic chip manufacturing capability as a strategic national interest.

Then, on April 22, 2026, during Tesla's Q1 earnings call, Elon Musk announced that Tesla would use Intel's 14A manufacturing process for its Terafab project in Austin. Tesla became Intel's first publicly-named major external customer for 14A.

The market's reaction was instructive. Intel stock rose 3.6 percent in after-hours trading, extended to a 52-week high of $70.33 earlier in the week, and was up roughly 235 percent over the prior 12 months from the 2024 lows.

What the Market Is Pricing

| Before Terafab announcement | After | |

|---|---|---|

| "Intel's foundry business has no major external customer" | "Intel has one announced 14A customer" | |

| Implied probability of foundry exit | Meaningful | |

| Implied probability of foundry exit | Reduced | |

| Market cap | $220B range | $290B+ range |

One customer does not restore the moat. What it does is introduce an option: the possibility that Intel survives as a viable US-based leading-edge foundry alongside TSMC, serves multiple external customers, and over 5–10 years rebuilds a different kind of moat — one based on domestic sovereign supply and regulatory protection rather than pure manufacturing leadership.

This is the third lesson of moat erosion: moats can partially reform, but rarely in their original shape. Intel's original moat (x86 architecture dominance + manufacturing leadership) is gone and will not return. A new, different, partially-protected position (US-sovereign leading-edge foundry, subsidized, multi-customer) may emerge. An investor betting on Intel today is not betting on the 2005 moat — they are betting on a different business entirely, and should price it that way.

Case Study: UnitedHealth in Real Time

Intel is the fully-played-out example. UnitedHealth, last week's efficient-scale moat example, is watching the process happen in real time.

Recall from W16: UnitedHealth's 2025 segment operating margin compressed from 5.2 percent to 2.7 percent in twelve months. The medical care ratio jumped from 85.5 percent to 88.9 percent. Earnings in the core insurance business fell from $15.6B to $9.4B — a $6.2B drop in one year.

The erosion path is different from Intel — UnitedHealth is facing regulatory change (Medicare funding reductions), not technology disruption. But the pattern of what happens first in a real-time erosion is similar:

1. Surface metrics still look acceptable. UnitedHealth grew revenue 16 percent to $345B in 2025. Surface growth was fine.

2. Underlying metrics tell a different story. Operating margin cut nearly in half. Medical care ratio at a multi-year high. Earnings from operations down 40 percent.

3. Guidance signals the scope of the problem. The company guided 2026 to its first revenue contraction in decades.

4. The market price reacts with a delay, then overshoots both ways. The stock experienced significant volatility through 2025 as analysts worked out which pieces of the erosion were cyclical (medical cost trends) and which were structural (regulatory margin compression).

The open question with UnitedHealth is whether this is a multi-year cyclical compression (like technology companies in 2001–2003, which recovered) or a permanent regulatory repricing of the moat (like some utilities after deregulation, which never did). Both are defensible views. The three-test framework from W16 is still passing for UnitedHealth structurally — the market position is intact, competitive entry remains deterred, the company still has pricing power through Optum — but the yield of the moat has compressed meaningfully. An investor who continues to hold UnitedHealth through this period is betting specifically that margin recovers to 5%+ in 2–3 years. That bet may or may not be correct, but it should be made explicitly, not passively.

The Early Signals That Actually Matter

Looking at Intel's 15-year decline, five specific signals were visible long before the financials caught up. Each one is observable for any company you own today.

1. Market share inflection. The most reliable leading indicator. A business losing 50 basis points of share per quarter looks unchanged on a short timeline and catastrophic over a decade. Track share quarterly for every holding with a quantifiable market. For Intel, the server share decline started in 2019. Five years later, the margin damage was unavoidable.

2. Manufacturing or process cadence slipping. For any business whose moat includes a technology or operational advantage, the cadence at which that advantage refreshes is critical. When Intel's manufacturing node introductions began slipping in 2015–2016, the moat was already weakening. Intel's reported margins did not reflect it for another five years.

3. Key customer announcements pointing elsewhere. When a dominant customer announces they are building or buying an alternative, that is a moat-erosion event even if the impact is years away. Apple's announced transition to Apple Silicon in 2020 was a structural signal that Intel did not control premium PC customers anymore. AWS Graviton deployment was the same signal in data centers.

4. Strategic pivots that acknowledge the erosion. IDM 2.0 (Intel's 2021 strategic pivot) was the company implicitly admitting that the old moat was no longer sustainable on a standalone basis. When a business that claimed to be a dominant compounder suddenly announces a major strategic restructuring, the restructuring itself is evidence that the internal view of the moat has shifted.

5. Competitor language shifts. Smart competitors know when they have an opening. When a previously-confident incumbent starts sounding defensive in earnings calls, and a previously-quiet upstart starts sounding aggressive, something structural has shifted. These tonal changes in industry conferences, analyst days, and executive statements frequently precede financial inflections by 2–3 years.

The Common Mistake: Confusing Cyclical Weakness with Moat Erosion

The hardest judgment in moat analysis is distinguishing cyclical compression from structural erosion.

A moat business having a bad year is normal. Intel had bad years in 2001–2002 and 2008–2009 and fully recovered both times. The 2022–2024 downturn, initially, looked similar — analysts argued it was another cyclical reset. Some of it was. But underneath the cyclical noise was a structural decline that had been building for years.

The distinguishing questions are specific and answerable:

Cyclical: Is the whole industry seeing the same pressure? Are peers' share metrics also suffering? Is management making long-term investments that assume the problem is temporary?

Structural: Is the pressure disproportionately on this company while peers hold up? Is management cutting R&D, delaying capex, or reshaping the narrative? Are leading indicators (share, customer wins, product pipeline) still deteriorating or stabilizing?

For Intel, by 2023 the answers were clear in the structural column. The peer (TSMC) was not experiencing the same pressure — TSMC's margins and share were expanding while Intel's were contracting. Management was cutting R&D and the dividend. Leading indicators were still deteriorating. Cyclical explanation failed.

For UnitedHealth in 2025, the answers are more ambiguous. Peer (Elevance) is seeing similar pressure — its benefit expense ratio also rose 150 basis points. Management is not cutting long-term investment. The regulatory pressure is industry-wide, not company-specific. The case for cyclical interpretation is real. That does not make it correct. But it makes the judgment a genuine judgment, not an obvious call.

An honest investor writes down, for any moat thesis they own, the three or four observations that would change their interpretation from cyclical to structural. If they cannot name them, they do not have a thesis — they have a hope.

What to Watch

Three habits separate investors who catch moat erosion early from those who catch it late.

Track leading indicators quarterly, not annually. Market share, customer wins and losses, product roadmap cadence, executive departures, and competitor posture are all observable at the quarterly level and move long before financial statements do. An investor who reads only the annual 10-K is typically 18–24 months behind an investor who reads the quarterly trade press and conference transcripts.

Distinguish ROIC trend from ROIC level. A business earning 22 percent ROIC still looks good at the level. The question is whether that number is 22 percent down from 27 percent three years ago (concerning) or 22 percent up from 18 percent three years ago (excellent). The trend usually matters more than the absolute number for moat-erosion detection.

Write down your exit triggers before you own the position. If you cannot name the specific events that would make you sell, you will not sell when those events occur. Intel's decline between 2015 and 2024 trapped many disciplined investors who had no pre-defined exit criteria. They waited for the data to tell them clearly. By then the data was catastrophic. Pre-commit to the criteria in writing, reread the list each quarter, and act when it triggers.

Brutal Edge Coverage Integration

This week's framework maps directly onto our coverage:

- TSLA Deep Dive Rev.2 (BEAF 58/C+) — explicitly addresses the difference between a moat under construction (Tesla's FSD data lead, Supercharger network) and moat claims that are not yet verified (brand, first-mover, "cult following"). The moat-erosion framework here helps distinguish which components are plausibly durable and which are tailwinds.

- NVDA Deep Dive (BEAF 83/B+) — covers the specific erosion risks to NVIDIA's current moat: hyperscaler custom silicon (Google TPU, Amazon Trainium, Marvell+Alphabet), open-source framework adoption, and the possibility that training-compute demand saturates faster than currently modeled. Each maps to one of the four erosion paths.

- Microsoft Deep Dive (BEAF 81/B+) — documents the live AI-era stress test on Microsoft's switching-cost moat and why the moat may partially reform around Copilot rather than erode.

- Physical AI Sector Report — traces moat erosion risk across all Tesla competitors, highlighting where incumbents' advantages (Waymo's engineering lead, Chinese AV scale) are structurally threatened or protected.

For additional frameworks, see our Deep Dive archive.

Looking Ahead

Next week we tackle the hardest version of this problem: identifying moats in businesses that did not exist five years ago. The frameworks we have built (three tests, four erosion paths, five moat types) were developed on companies with decades of visible history. They still apply to new-technology businesses — but you have to read them from behavioral signals rather than 20-year financial track records. We examine Anthropic and OpenAI as the live test case, and look at how to read moat formation in a category where the category itself is still being defined.

For now, sit with this week's lesson. No moat is permanent. The best ones last generations. The worst do not survive a decade. Your job as an investor is not to believe in any moat forever. It is to read the erosion signals early enough to act on them before the market does.

Brutal Edge. Frameworks over forecasts. Signal over noise.

Disclaimer. Brutal Edge is an independent investment research platform. This report is published for educational and informational purposes only and does not constitute investment advice, a recommendation to buy or sell any security, or an offer to transact in any financial instrument. All valuations, forecasts, and opinions are the analyst's own and are subject to change without notice. Past performance does not guarantee future results. Readers should conduct their own due diligence and consult a qualified financial professional before making investment decisions.

Educational content only. Not investment advice. Always do your own research.