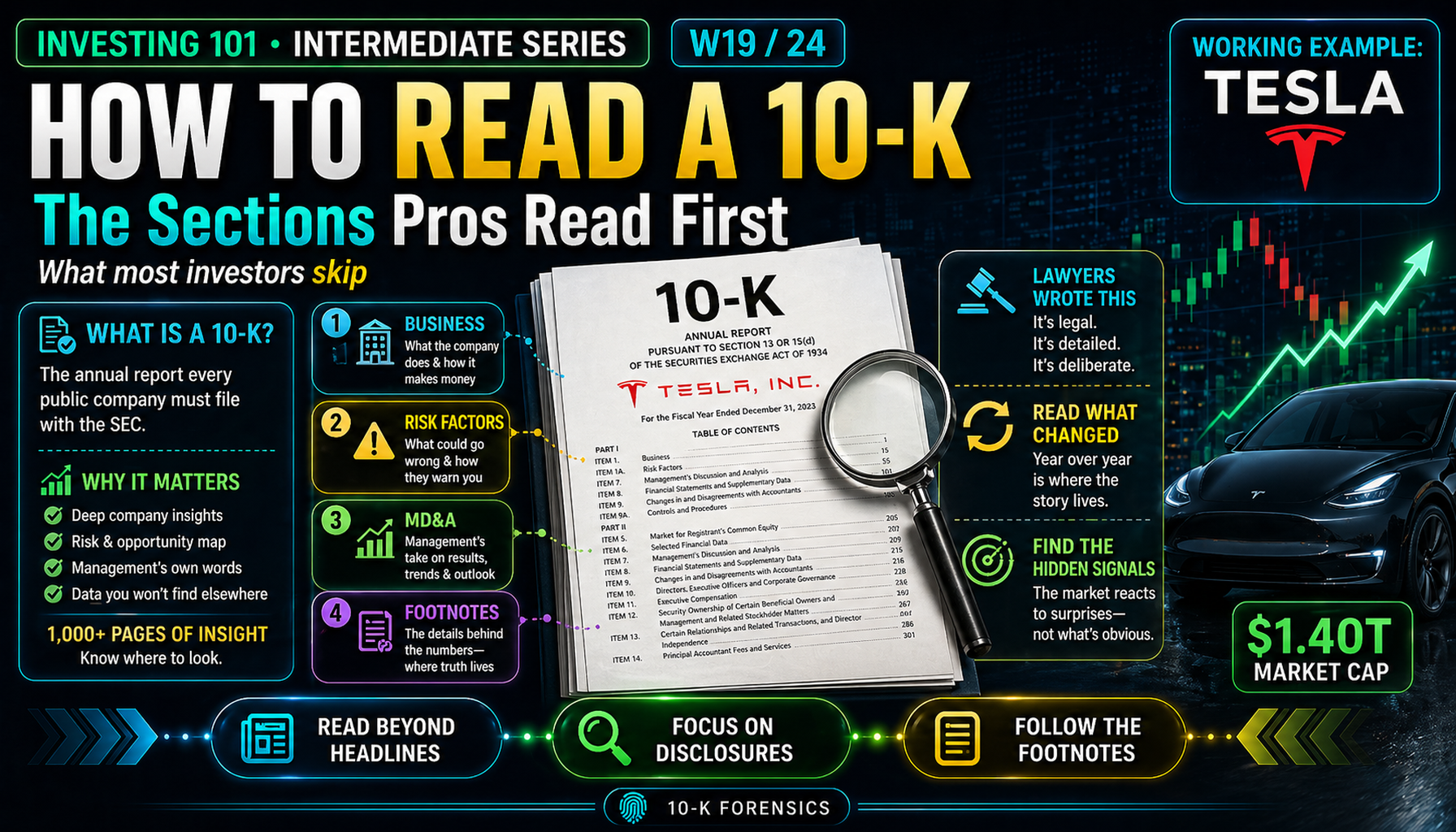

The 10-K Sections Most Investors Skip. Pros Read Them First.

Most retail investors never read a 10-K. Those who try give up in the financials. The sections that professional analysts read first are the ones most people skip entirely. This week we work through Tesla's actual 10-K.

10-K Forensics

Every US-listed company is required to file a Form 10-K annually with the SEC. It is the single most important document a public company produces — a legally mandated, auditor-reviewed, lawyer-scrubbed account of what the business actually is, what it does, what it is exposed to, and how it made its money. It typically runs 150 to 400 pages. It is boring on purpose. And it is where the real work of analysis happens.

The 10-K is not a marketing document. It is the inverse — a defensive document, written under threat of securities litigation, where every disclosure has been negotiated between management and legal counsel to say exactly what the company is legally comfortable saying and no more. That constraint is what makes it valuable. The press release presents the story the company wants you to believe. The earnings call lets executives color it in. The 10-K tells you what the lawyers would allow to be printed.

This week we walk through the 10-K the way a professional investor actually reads it — in a specific order, with attention to specific sections, looking for specific signals. Using Tesla's most recent 10-K as the working example, you will see how the sections most retail investors skip are the ones most likely to change an investment thesis.

Core Framework: The Four 10-K Sections That Matter Most

A 10-K has 15 major items. Most of them are formality. Four of them contain almost all the analytical value.

| Item | Section | What It Actually Tells You |

|---|---|---|

| Item 1 | Business | How the company describes its own business model and segments |

| Item 1A | Risk Factors | What management is legally required to disclose as potential downside |

| Item 7 | MD&A (Management's Discussion and Analysis) | Why the reported numbers are what they are |

| Item 8 (Notes) | Financial Statement Footnotes | The specific accounting choices and disclosures that the summary numbers compress |

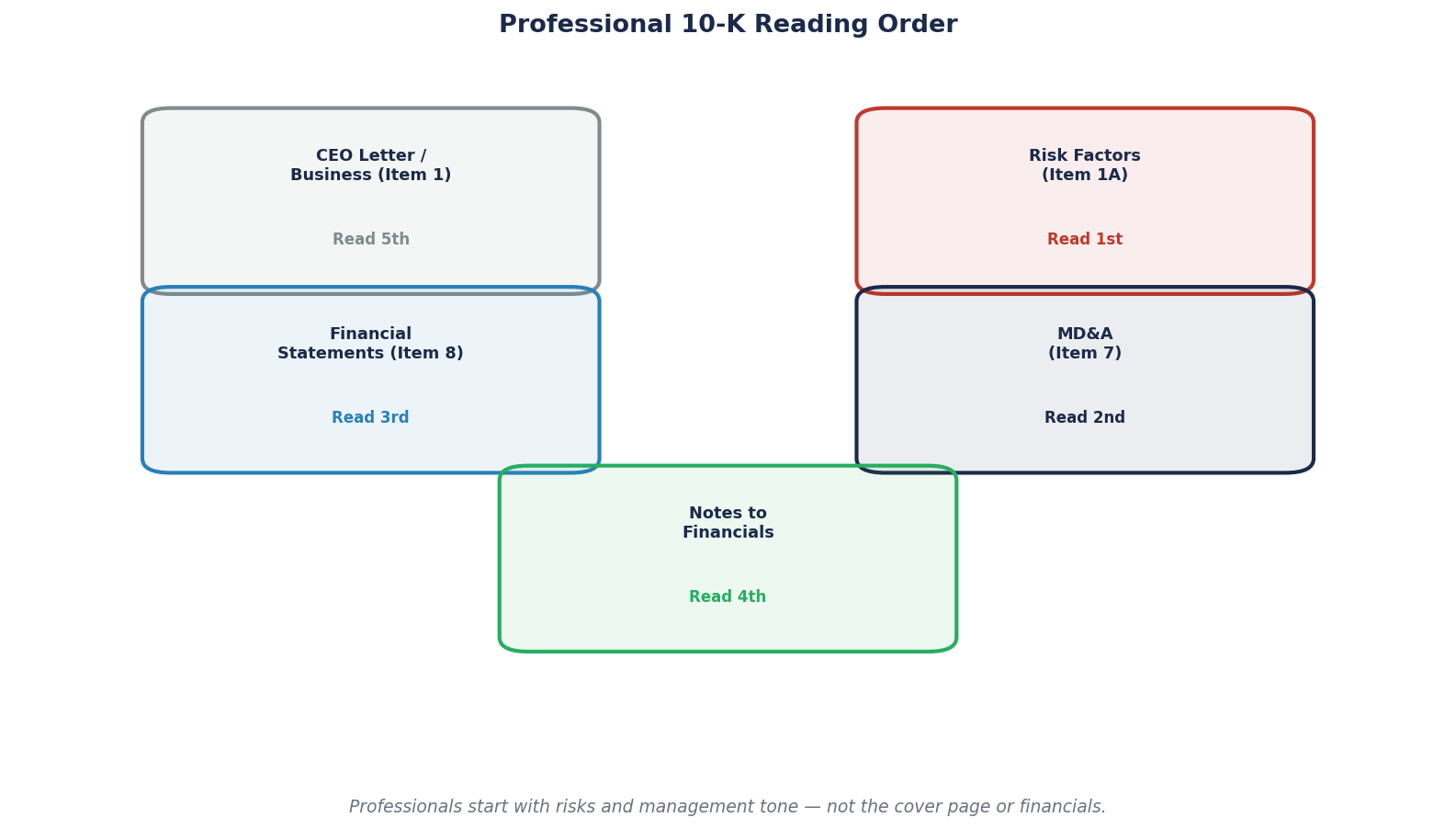

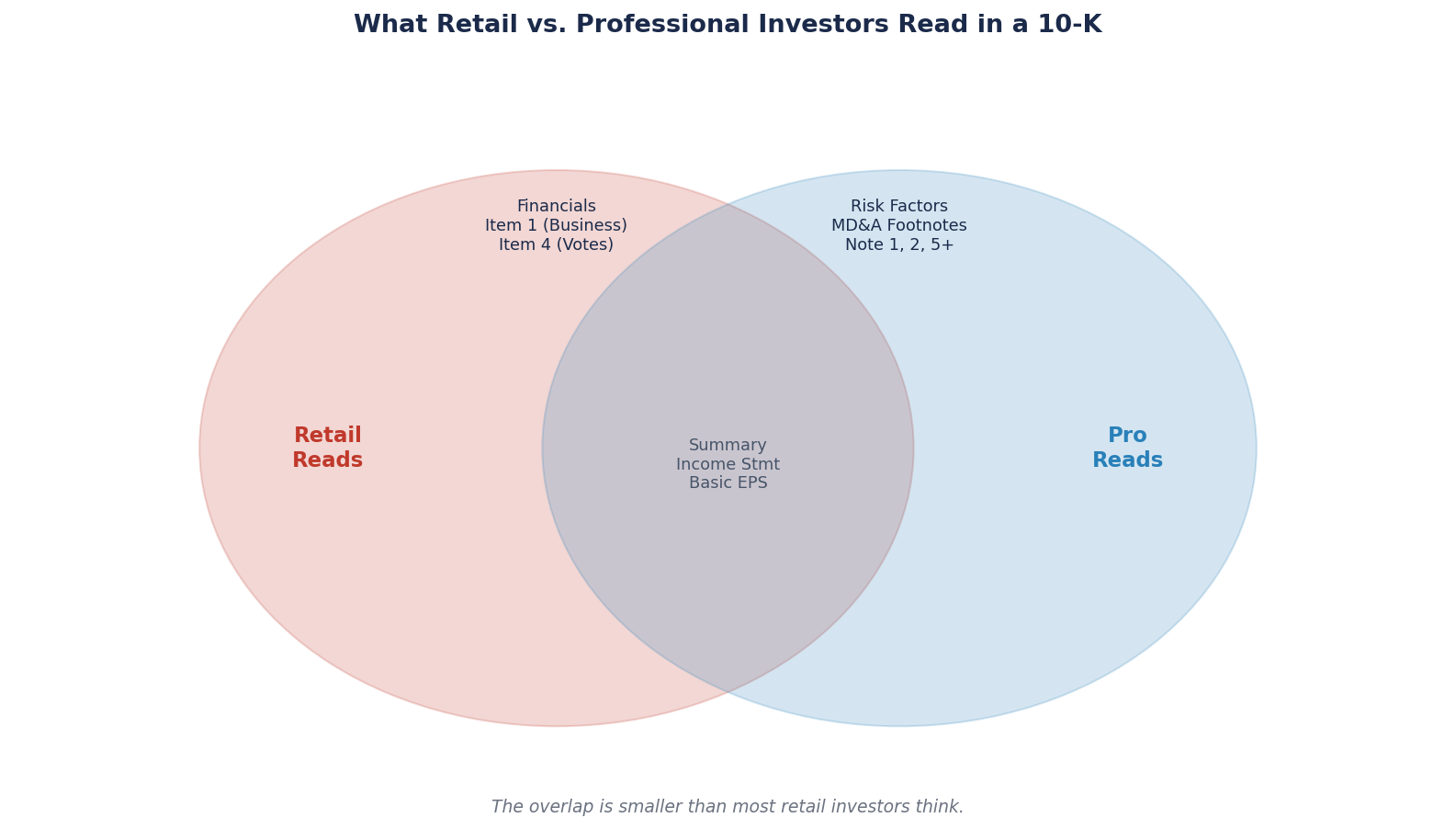

Most retail investors read none of these — they read the press release and the headline revenue number. Most professional investors read Items 1A and the Notes first, then Item 7, then Item 1. The reasons map directly to where the most information per page lives.

Item 1 — Business: How the Company Sees Itself

Item 1 is the company's own description of what it does. For most companies this section is relatively uninformative — it describes the business segments, products, customers, and competitive environment in language that has been polished over years.

The analytical value of Item 1 is in two specific things:

1. Segment definition changes. When a company reorganizes its reported segments, they are telling you something about how they plan to be measured. Tesla's 10-K separates its business into Automotive and Energy Generation and Storage. The Automotive segment includes both vehicle sales and "FSD (Supervised)" features, plus the Cybercab Robotaxi product. Grouping Robotaxi inside Automotive rather than as a separate segment is a choice. It tells you that, for disclosure purposes, Tesla wants Robotaxi financial impact to remain bundled with vehicle economics rather than broken out as a standalone business.

2. Language shifts between filings. The 10-K is filed annually. Comparing this year's Item 1 to last year's — paragraph by paragraph — often reveals what management's narrative has quietly shifted toward or away from. For Tesla, recent 10-Ks have increasingly emphasized "Full Self-Driving (Supervised)," AI, and robotics, while the language around traditional EV manufacturing has become more matter-of-fact. These shifts reflect management's priority reordering and often precede strategic announcements.

The Tesla Example

In Tesla's 2024 annual 10-K (filed January 2025), the Business section reads in part:

"We have planned electric vehicles to address additional vehicle markets, and continue leveraging developments in our proprietary Full Self-Driving ('FSD') (Supervised) features, including through our purpose-built Robotaxi product — Cybercab, and battery cell and other technologies."

The phrasing is careful. "Proprietary Full Self-Driving (Supervised) features" is specific — the "Supervised" designation appears in every official Tesla document because the product is not yet approved for unsupervised autonomous operation, and the legal distinction matters for regulatory and liability purposes. Cybercab is referenced as a "purpose-built Robotaxi product," which is forward-looking language. The sentence bundles autonomy, robotaxi, and batteries together, reflecting how Tesla positions them as a unified technology stack rather than separable businesses.

A reader who skips this section misses the framing the entire rest of the document assumes.

Item 1A — Risk Factors: Where the Legal Constraint Actually Bites

Item 1A is the most revealing section in any 10-K, and the one most consistently underread.

Companies are required to disclose material risks to their business. They also have every incentive to disclose those risks in the most generic language the SEC will permit, because each specific risk disclosure creates potential securities litigation exposure. The result is a section that looks repetitive and boilerplate to a casual reader — and contains surgically specific language to a reader who knows what to look for.

Three categories of information in Risk Factors:

1. New risks that did not appear in last year's filing. These are the highest-value. A risk added to the 10-K did not exist (legally speaking) a year ago, which means something changed operationally to require the disclosure. Read this year's Item 1A side-by-side with last year's and mark every new paragraph. That list is your priority investigation queue.

2. Risks where the language has intensified. A risk that was previously described as "may" or "could potentially" and is now described as "is likely to" or "has materialized" is a signal. Companies do not intensify risk language lightly — it triggers disclosure-committee review and legal-team scrutiny. Watch for verb shifts.

3. Risks that are now quantified where they previously were not. A risk that used to say "may impact our operations" and now says "resulted in a $XXX million impact in the prior fiscal year" is telling you the situation has moved from theoretical to actual.

What to Look for in Tesla's 10-K

Tesla's Risk Factors historically cover supply-chain, battery material dependence, regulatory treatment of autonomous vehicles, direct sales model, defects and recalls, cybersecurity, union activity, competition, key-person risk (Elon Musk), and regulatory subsidy changes. Over recent filings, certain specific items have intensified:

- Language around autonomy regulatory pathway has become more specific and more extensive as the company's commitments to Robotaxi scale have grown.

- Hardware capability limitations — specifically the question of whether older HW3 vehicles will be able to run future FSD versions — is a disclosure item that has quietly expanded in scope. This has real financial implications for the company's deployed fleet and installed-base moat story.

- Key-person dependence on Elon Musk is a stock risk factor that has become longer over time as the company has made more statements tying its long-term plans specifically to Musk's continuing leadership.

- Regulatory credits and subsidy dependence — language about potential US regulatory changes affecting EV tax credits and emissions credits has evolved across recent filings.

Each of these is a paragraph that a retail investor almost certainly skips. Each is also the kind of detail that can change how to price risk in the underlying thesis.

Item 7 — MD&A: The Bridge Between the Numbers and the Explanation

Item 7 — Management's Discussion and Analysis of Financial Condition and Results of Operations — is the section where the reported numbers get their narrative context. This is where management explains why revenue grew, why margins compressed, why capital allocation changed.

Unlike the press release or earnings call, the MD&A in a 10-K is held to a higher disclosure standard. It is audited by the auditor's fairness review, reviewed by the audit committee, and scrutinized by legal counsel for forward-looking statement liability. The language is more measured, and the explanations are more complete.

What to read carefully in the MD&A:

Segment revenue decomposition. The top-line number is an aggregation. The MD&A breaks it into components — which segments grew, which contracted, which had pricing versus volume effects. For Tesla, the key decomposition is vehicle revenue (pricing, volume, mix), regulatory credit revenue (which has historically varied significantly quarter to quarter), FSD deferred revenue recognition, and energy storage revenue. Each has very different margin profiles and very different sustainability characteristics.

Cost trend explanations. When operating margin compresses or expands, the MD&A is required to explain the underlying drivers. Look for specific attributions — raw material costs, logistics costs, pricing actions, manufacturing scale effects. The relative weight the company gives to each tells you what management sees as sustainable versus temporary.

Cash flow vs earnings reconciliation. This is usually where the most revealing information lives. Reported net income and actual cash generated often diverge for specific reasons — working capital changes, deferred revenue, stock-based compensation, one-time items. The MD&A's explanation of the divergence is the closest thing you will get to understanding "what the business actually earned."

Liquidity and capital allocation. A section on cash on hand, debt maturity schedule, share repurchase activity, and capital expenditure plans. For capital-intensive businesses like Tesla, capital allocation is often the single most important management decision in any given year.

The Tesla Q4 MD&A Pattern

For Tesla specifically, the MD&A has been where the most significant narrative shifts have occurred over the past three years:

- The transition from "gross vehicle sales volume growth" as the headline story (2021–2022) to "operating leverage and cost reduction" (2023) to "AI and autonomy as the value driver" (2024–2025) to "capital expenditure re-guidance for AI and robotics" (2026 Q1, where the full-year capex guidance was raised from $20B to over $25B).

Reading three consecutive years of MD&A side by side gives you a time-lapse of how Tesla's narrative has evolved. That evolution is often what analysts are trying to reconstruct after the fact, using interviews and earnings call excerpts. The MD&A is a cleaner source.

Item 8 Notes — Where the Specific Disclosures Live

The financial statement Notes are the most under-read and most information-dense section of any 10-K. They typically run 40–80 pages and contain the specific disclosures that the summary income statement, balance sheet, and cash flow statement aggregate away.

Seven specific Notes to always read:

1. Summary of Significant Accounting Policies. Every 10-K begins the Notes with a description of how the company recognizes revenue, depreciates assets, treats stock-based compensation, and handles other key accounting choices. Changes to these policies year-over-year are legally required to be disclosed. When policy changes occur, they almost always represent either a strategic reframing or a response to audit pressure.

2. Revenue Recognition. For software and AI companies, revenue recognition is where the real business model lives. What percentage of reported revenue is subscription versus transactional? How much is deferred? What is the typical contract length? Over what period is FSD subscription revenue recognized for Tesla? These are disclosed only here.

3. Income Taxes. The effective tax rate a company reports can diverge significantly from statutory rates due to geographic mix, R&D credits, stock-based compensation treatment, and deferred tax positions. The tax rate footnote reconciles the difference and is often where analysts catch either aggressive or conservative accounting.

4. Stock-Based Compensation. For technology companies, SBC is a substantial real cost that GAAP historically treats differently from cash compensation. The specific disclosures here — RSU grants, performance-based awards, dilution schedule — are where investors can see exactly how much of the company's earnings power is flowing to employees versus shareholders over time.

5. Commitments and Contingencies. Legal proceedings, contractual commitments, off-balance-sheet obligations, and other exposures that do not appear on the balance sheet but could materially affect the business. This is where pending lawsuits and regulatory actions are disclosed.

6. Segment Reporting. The financial detail for each reported segment — revenue, operating income, assets, depreciation. This is where the high-level segment commentary in Item 7 gets quantified.

7. Subsequent Events. Events after the balance-sheet date that are material enough to require disclosure but do not affect the period's reported numbers. This is often where the most recent strategic developments are formally disclosed to investors.

For Tesla Specifically

The most analytically valuable Notes items in Tesla's 10-K tend to be:

- Revenue recognition for FSD. The company recognizes FSD revenue over a specific deferral period tied to feature availability. Understanding this schedule is essential to understanding how the 456,000 active FSD subscribers convert to reported revenue.

- Warranty reserves. Tesla's reported warranty provision is a specific line item, and changes in warranty expense ratios can signal either changing product quality or changes in accounting assumptions.

- Regulatory credit revenue. Disclosed as a specific line, typically highly variable quarter-to-quarter. This is essentially non-operating income, and excluding it from "core operating margin" gives a very different picture than the headline.

- Commitments. Lease commitments for new facilities (Cybertruck, Cybercab, Optimus production lines, Terafab-adjacent investments) typically show up here before they show up on the balance sheet.

Case Study: Three 10-K Disclosures That Mattered

Consider three disclosure patterns and what careful readers took from them.

Pattern 1: New risk factor disclosure. In recent filings across the auto industry, risk factors relating to competitive pressure from Chinese EV manufacturers have expanded from a few sentences to multiple paragraphs. For US-listed auto OEMs, this pattern preceded significant share-price volatility as investors recognized that Chinese competition had moved from theoretical to material.

Pattern 2: Segment reorganization. When a company reports a new segment or consolidates existing segments, the disclosure itself tells you where management wants investor attention. A company breaking out a high-growth segment newly is signaling that it wants that segment to be valued separately. A company consolidating segments is often signaling the opposite — attempting to make it harder to dissect the business.

Pattern 3: Accounting policy changes. Adoption of new accounting standards is typically disclosed in the Notes with specific impact quantification. The FASB's adoption of the crypto assets standard in 2024–2025 required a recast of prior-period financial statements for companies holding cryptocurrency — Tesla among them. The Q4 2025 / Q1 2026 releases referenced these recast adjustments in the footnotes. Readers who caught the recast understood that prior quarterly comparisons were not apples-to-apples.

In each pattern, the information was publicly disclosed, in the required section, with appropriate prominence. It was available to anyone who read the document. Most retail investors did not.

Reading the 10-K Efficiently

A full careful read of a 10-K takes 90 minutes. Most investors do not have 90 minutes per holding per year. Here is the compressed version.

30-minute read (high-priority):

- Item 1A Risk Factors (compared to prior year, mark every new or intensified paragraph)

- Item 7 MD&A (segment revenue and cost trend sections, plus liquidity section)

- Item 8 Notes (Revenue Recognition, Commitments, Subsequent Events — skim for anything flagged)

60-minute read (more comprehensive):

- Add Item 1 Business (language shifts vs prior year)

- Add Item 8 Notes in full (Significant Accounting Policies, Income Taxes, Segment Reporting)

- Add the full Liquidity and Capital Allocation subsections of MD&A

90-minute read (full comprehension):

- Add Item 7A (Market Risk — usually interest rate and currency exposure)

- Add Part III (Governance — covered in more detail in the proxy statement, W21)

- Add the complete financial statements with all footnote cross-references

For a company you are considering owning for multiple years, the 90 minutes per year is a small investment. For a portfolio of 10 holdings, it is 15 hours a year — a half-day per quarter. Most retail investors do not spend this time. The ones who do have an information advantage that compounds every year of holding.

The Common Mistake: Reading the Press Release Instead

The most destructive pattern in 10-K analysis is the same pattern retail investors have with every corporate communication — reading the summary and assuming the summary is the document.

The press release is written by investor relations. It is a narrative the company has chosen to tell. The 10-K is a legally binding disclosure document that must contain specific information whether the company likes it or not. These two documents about the same quarter or year are related but materially different products of different processes, reviewed by different people, bound by different legal standards.

When the press release headline says "record revenue of $XB, up Y%" and the 10-K buried in the Notes says the growth came from a one-time reclassification of deferred revenue — both are true, and the 10-K tells you more. When the earnings call says "strong momentum into next year" and the 10-K risk factor adds a new paragraph about customer concentration — again, both are true, and the 10-K is the source you trust.

A professional investor's discipline is to treat the press release and earnings call as the story, and the 10-K as the truth check on the story. When they agree, the thesis is durable. When they disagree, the 10-K wins.

What to Watch

Three habits will turn 10-K reading from an annual ritual into a real analytical edge.

Compare year-over-year, not just current to expectation. The highest-signal changes in a 10-K are almost always delta-based. What does the risk factors section say this year that it did not say last year? Which MD&A commentary shifted? Which footnote expanded? Current-year snapshots are useful; year-over-year deltas are where the actual information lives.

Read the companies you do not own. You will read Tesla's 10-K if you own Tesla. Read Ford's, GM's, and BYD's at the same time. The comparative read tells you which risks are industry-wide and which are company-specific, which language is boilerplate and which is distinctive. The 10-K is most valuable when read comparatively.

Mark every new disclosure with a date. When a new risk factor appears, make a note — "new disclosure: [topic], filed [date]." Over years, the accumulated list becomes a timeline of how the business has evolved in the legal view of its own management. That timeline is one of the cleanest long-term analytical assets you can build, and it takes almost no effort beyond annual reading.

Brutal Edge Coverage Integration

This week's framework maps directly onto our coverage:

- TSLA Deep Dive Rev.2 (BEAF 58/C+) — our thesis incorporates specific readings from Tesla's most recent 10-K, including the FSD revenue recognition schedule, the regulatory-credit dependency analysis, and the risk-factor language shifts on autonomy, HW3, and capital allocation. The 58 score reflects exactly the tension between management's public narrative and the legally-bound 10-K disclosures.

- Physical AI Sector Report — the 10-K reading frameworks are applied across the Physical AI names we cover, flagging specific disclosure patterns that investors should watch as the autonomy and robotics categories mature.

- NVDA Deep Dive (BEAF 83/B+) — a case where the 10-K reading reinforces rather than complicates the headline thesis. The Notes on customer concentration (hyperscalers as top-10 customers) are worth reading as a counter-example to Tesla's more contested disclosures.

- Microsoft Deep Dive (BEAF 81/B+) — the Commercial RPO disclosure ($625B, +110% YoY) is exactly the kind of Note-level detail that transforms a surface quarterly number into a structural moat signal.

For additional frameworks, see our Deep Dive archive.

Looking Ahead

The 10-K is the regulatory document. Next week we cover the event where management meets the market and answers unscripted questions — the earnings call. We walk through Tesla's Q1 2026 call (held April 22) as the working example, examining what was said, what was deflected, and what the tonal shifts revealed about management's own confidence in specific parts of the thesis. Most retail investors listen to earnings calls for the headline beat-or-miss. Professionals listen for everything else.

For now, sit with this week's lesson. The 10-K is not a brochure. It is a legally mandated disclosure document, and the disclosures most worth reading are the ones least likely to be highlighted by the company itself. Learn to read what the document says, not what the company says about it.

Brutal Edge. Frameworks over forecasts. Signal over noise.

Disclaimer. Brutal Edge is an independent investment research platform. This report is published for educational and informational purposes only and does not constitute investment advice, a recommendation to buy or sell any security, or an offer to transact in any financial instrument. All valuations, forecasts, and opinions are the analyst's own and are subject to change without notice. Past performance does not guarantee future results. Readers should conduct their own due diligence and consult a qualified financial professional before making investment decisions.

Educational content only. Not investment advice. Always do your own research.