What CEOs Don't Say on Earnings Calls Tells You More

The prepared remarks on an earnings call are a scripted press release. The real information is in what management avoids answering. This week we analyze Tesla's Q1 2026 earnings call using a professional framework.

Earnings Calls

Every public company holds an earnings call quarterly. Most retail investors either skip them entirely or read a summary article afterward. Professional investors listen to every one for the companies they cover, and often to calls for companies they do not yet own but might later.

The reason is not that the call contains new financial data — the press release that drops before the call usually contains every material number. The reason is that the call is the one scheduled event per quarter where management confronts unscripted questions from sophisticated, occasionally hostile, industry analysts. How they answer, what they deflect, what topics they voluntarily introduce, what they drop from this quarter that they emphasized last quarter — all of it is information. Often, more information than the numbers themselves.

This week we walk through Tesla's Q1 2026 earnings call, held on April 22, 2026, as the working example. The call produced a headline beat (revenue up 16 percent year over year, free cash flow unexpectedly positive at $1.4 billion) and a headline miss (capex guidance raised from $20B to over $25B, negative FCF guided for the rest of the year). More importantly, it produced several specific rhetorical patterns that reveal how management is thinking about parts of the business they did not want to talk about directly.

Core Framework: The Three Parts of an Earnings Call

Every earnings call has the same structure. Each part serves a different function, and each requires a different kind of attention.

| Part | Duration | What It Contains | What to Listen For |

|---|---|---|---|

| Prepared Remarks | 15–25 min | Scripted commentary from CEO/CFO | New information not in the press release; tonal emphasis |

| Analyst Q&A | 30–40 min | Unscripted responses to analyst questions | Deflections, hesitations, topic shifts, specific word choices |

| Close / Forward-looking framing | 3–5 min | CEO closes the call | What management wants as the final impression |

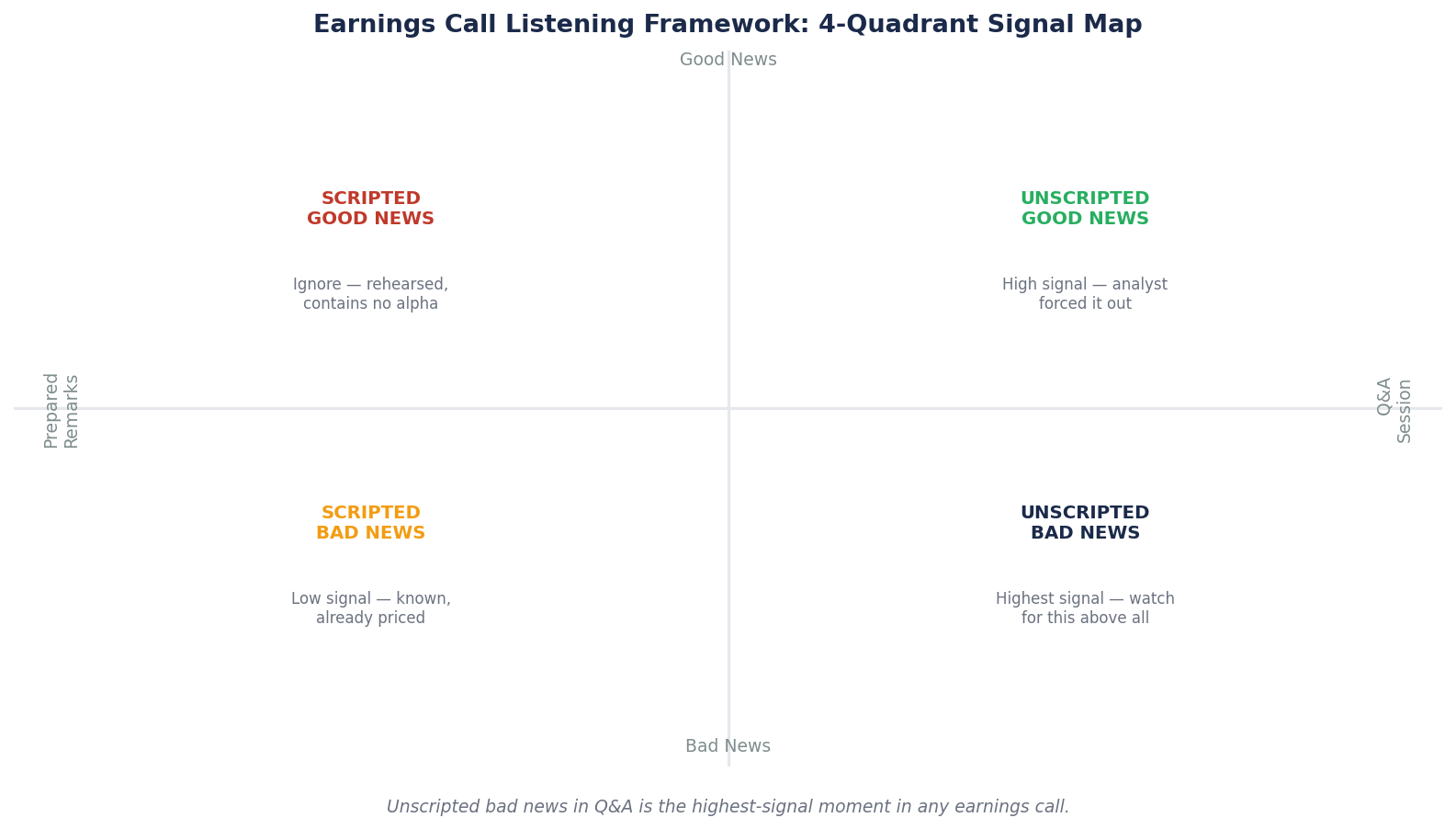

Retail investors tend to pay most attention to Part 1 (prepared remarks) because it is clean and structured. Professionals pay most attention to Part 2 (Q&A) because it is where management is most likely to reveal what they did not plan to say. The contrast between the script and the ad-lib is often the most valuable signal of the quarter.

Part 1: The Prepared Remarks on Tesla Q1 2026

The prepared remarks phase of the Tesla call covered roughly 25 minutes. The CFO and CEO each spoke. The material new information — beyond what was in the press release — came in three specific passages.

1. The capex re-guidance. CFO Vaibhav Taneja delivered what was probably the most market-moving piece of information on the call:

"As Elon mentioned, we are in a very big capital investment phase, which is going to start now and would last a couple of years. Based on that, our current expectation for 2026 is over $25 billion of CapEx. Just to remind you, we are paying for six factories which we're going to go into operation."

The press release had alluded to elevated capex but had not explicitly stated a figure above $25B. Last quarter Tesla had guided to approximately $20B for 2026. A $5B+ re-guidance mid-year, delivered with the phrase "for a couple of years," is a significant commitment change — and the market responded accordingly, with the stock falling roughly 3.6 percent the next trading day after rising 4 percent in after-hours.

2. The framing of the cash flow outcome. Taneja continued:

"While this may seem like a lot, and will have the impact of negative free cash flow for the rest of the year, we believe this is the right strategy to position the company for the next era."

Two specific phrases to note. "May seem like a lot" is a pre-emptive softening — the CFO is addressing an objection before it is raised. "Position the company for the next era" is forward-looking rhetoric that reframes the current burn as strategic investment rather than margin pressure. Both are craft. Neither is a neutral statement of fact. The fact itself — negative FCF for the rest of 2026 — is what matters. The framing is what management wants you to emphasize.

3. The Musk opening statement on autonomy and robotics. Musk's prepared remarks emphasized investment across "battery powertrain, AI software, AI training, chip design" and described a future of "significantly increased manufacturing production." He said explicitly that Tesla is "laying the groundwork" for a production ramp and mentioned the company has "already started placing orders for the research semiconductor fab in Austin."

This is classic forward-narrative Musk. The prepared remarks pitched the story that the capex ramp is an investment in Tesla's next decade. The specificity varies by topic — chip fab orders are concrete, production ramp specifics are not.

What to Note from Part 1

- New information that was not in the press release: the "couple of years" language on capex, the specific reference to "six factories," the Austin semiconductor fab order placement.

- Framing that shapes interpretation: "next era," "the right strategy," "position the company." Investor should read these as deliberate choices by management, not neutral descriptions.

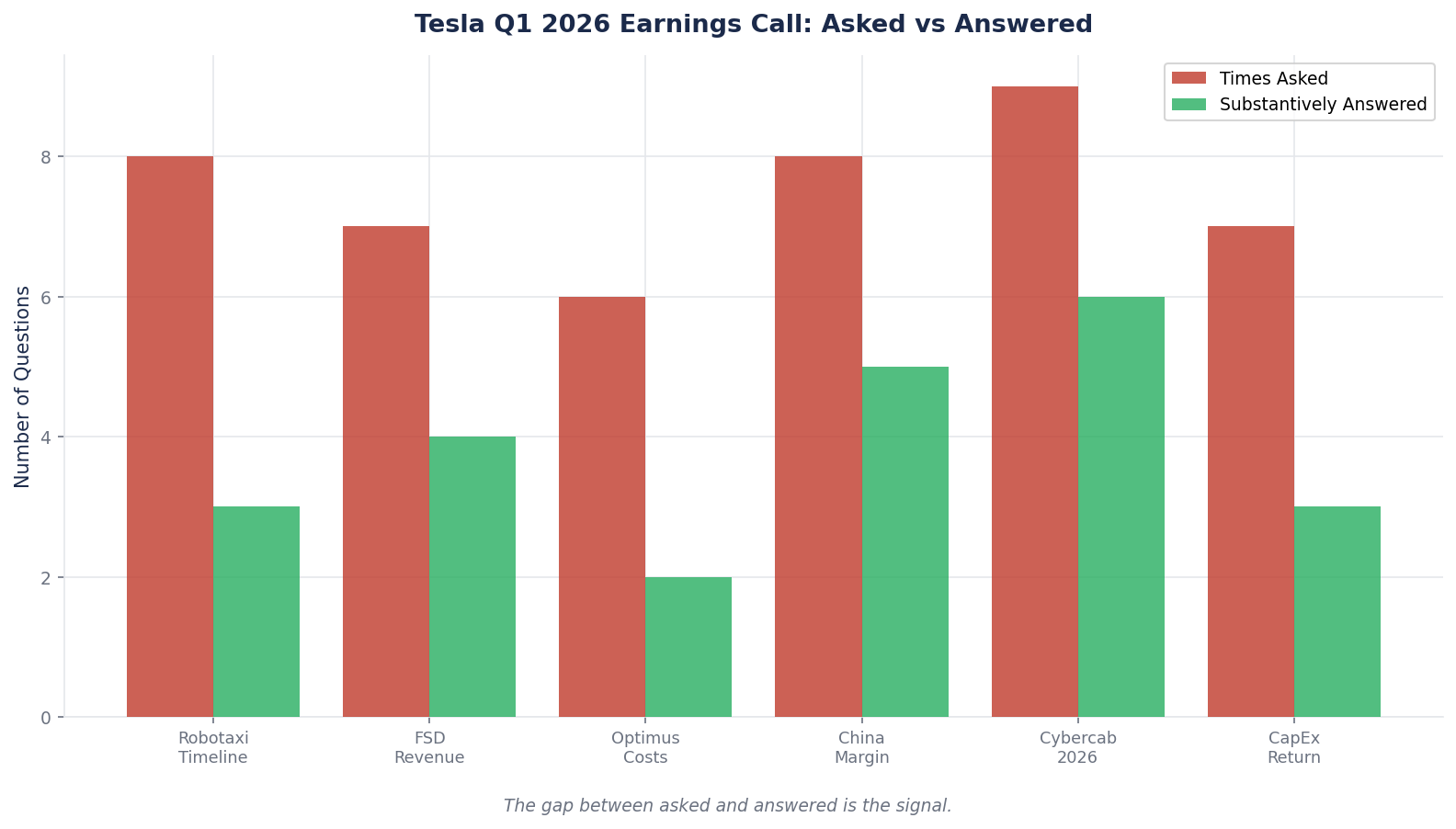

- What was NOT in the prepared remarks: no specific unit volume guidance for Cybercab. No specific timeline for Optimus revenue. No specific Robotaxi revenue target for 2026. Each of these absences is significant for a company whose multi-trillion-dollar valuation rests partially on these products.

Part 2: The Q&A — Where the Real Information Lives

The Tesla Q1 2026 Q&A ran roughly 35 minutes. Analysts asked approximately a dozen questions. Several patterns emerged that a careful listener would have flagged in real time.

Deflection Pattern 1: The Vague Future Tense

When an analyst asked specifically about milestones for unsupervised FSD and Robotaxi expansion, Musk responded:

"Well, we certainly hope to have unsupervised FSD or Robotaxi operating in a dozen or so states by the end of this year. Initially, we're taking a very cautious approach to the rollout here. Like we haven't had any injuries and certainly no fatalities to date with the unsupervised FSD and Robotaxi expansion. We want to keep it that way."

Then he added the key line:

"And so I don't — I think probably unsupervised FSD or Robotaxi revenue would not be super material this year. But I do think it will be material — it will be material probably in a significant way next year."

Read that carefully. The analyst asked two specific questions: milestones and revenue impact. The answer on milestones is "a dozen or so states" with qualifier "we certainly hope." The answer on revenue impact is "not super material this year... material... probably... in a significant way next year."

The rhetorical pattern: Hopeful language ("hope to," "probably," "in a significant way") paired with hedging ("we certainly hope," "I don't think," "probably not super material"). The specific numeric commitment the analyst asked about is not given. Instead, the response is a vision statement about direction with no operational metrics.

For a company at $1.4 trillion market cap where 2026 Robotaxi revenue is a major component of the bull thesis, "probably not super material this year" is the informational content of the answer. Everything else is framing.

Deflection Pattern 2: Reframing the Constraint

When Dan Ives from Wedbush asked about what limits Robotaxi expansion, Musk responded:

"I think a lot of what limits wider deployment of Robotaxi are actually not safety issues, but convenience issues, or the car basically gets paranoid and gets stuck. Because it's programmed for maximum safety."

This is a revealing reframe. The analyst was implicitly asking about the pace of rollout. The answer "not safety, but convenience" functions to do two things at once: (1) reassure on safety (the bigger investor concern), and (2) introduce a new concept — "paranoid and gets stuck" — that sounds operational and specific but actually reveals that the current system is not reliable enough for independent deployment at scale. If the car is regularly "getting stuck" for caution, that is a meaningful user experience problem for a commercial robotaxi service.

Professional investors noted this admission. It is a real constraint, stated by the CEO in plain language, about a product the valuation assumes is near-deployment-ready. "Gets paranoid and gets stuck" is the kind of phrase that ends up in sell-side research notes the next morning.

Deflection Pattern 3: The Topic That Gets Skipped

Every earnings call has topics that analysts ask about but management consistently routes past. For Tesla Q1 2026, one obvious example: Optimus production rate exiting 2026.

This was one of the most upvoted questions from retail investors submitted to the analyst platform. Musk mentioned Optimus multiple times in the prepared remarks and in response to other questions, but did not provide a specific production rate or unit volume target for end-of-year 2026. The topic was discussed narratively; the numbers were not provided.

When a topic is prominent in framing but absent from quantification, that gap is information. Management has chosen not to quantify because either (a) the number is not yet confident, (b) the number would disappoint, or (c) both. In Optimus's case, the absence suggests the company is not yet confident enough in its production ramp to commit to a public number — which is meaningful given that previous Musk statements had referenced substantial production volumes by this timeframe.

The Pattern in Aggregate

Put these three together. A future-tense response on Robotaxi milestones with no hard number. A reframe of the Robotaxi constraint to something the CEO can describe in plain words. A topic (Optimus production) that is omnipresent in narrative and absent in quantification.

This is a pattern that sell-side analysts recognize instantly. The company is protecting its long-term narrative while gently lowering near-term expectations — a technique sometimes called "narrative hedging." The 2026 story is softened ("not super material this year") while the 2027+ story is elevated ("material in a significant way next year").

The stock's 3.6 percent decline the next day reflected the market processing this pattern. The numbers beat estimates. The guidance and narrative hedging did not.

Listening for Specific Tonal Signals

Beyond the specific topics, earnings calls contain tonal signals that leading-edge analysts track over time. Four categories matter.

1. Confident language vs hedged language. When management uses phrases like "we expect," "we are targeting," "we will deliver" — these carry more commitment weight than "we hope," "we believe," "we think." A company that shifts from confident to hedged language on a specific metric is signaling lower internal conviction.

2. First-person vs third-person framing. When Musk says "the car is programmed for maximum safety" (third-person, distanced), he is describing a property of the product. When he says "we will have unsupervised" (first-person commitment), he is making a personal and corporate promise. The same topic can be discussed in multiple voices, and which voice management selects tells you something about how they are holding the commitment.

3. Absence of previously emphasized topics. If management spent the last four calls talking extensively about a specific initiative, and this call barely mentions it, something has changed. The omission is the signal. Track topic frequency quarter over quarter to catch these shifts.

4. Cross-call language evolution. Language that persists across multiple calls ("we remain on track") is different from language that appears for the first time ("we are accelerating our approach"). Evolving phrases often precede operational changes.

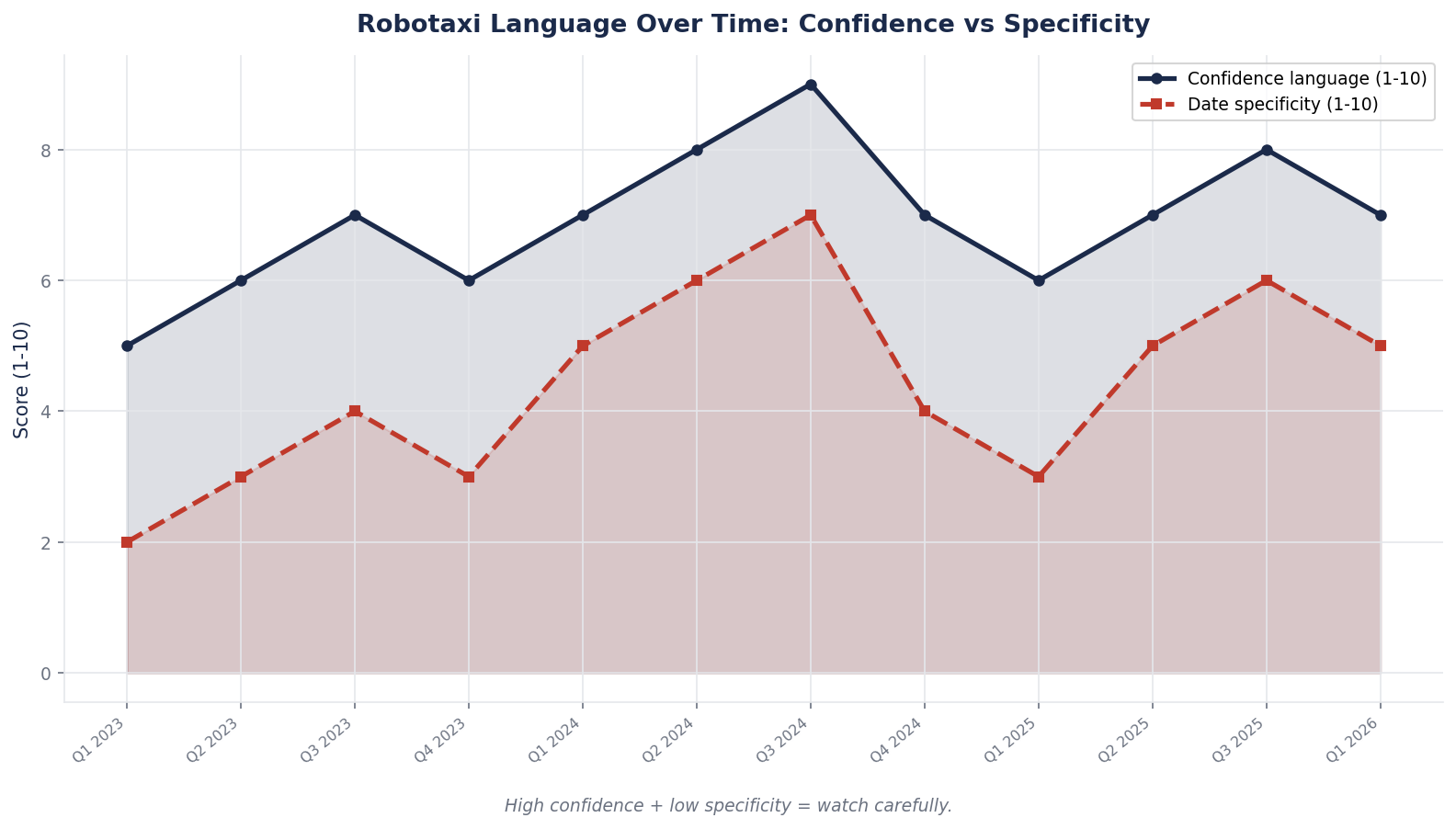

For Tesla specifically, the cross-call pattern on Robotaxi over the past six quarters has moved from "launching this year" (Q2 2025) to "expanding the pilot" (Q3 2025) to "scaling carefully" (Q4 2025) to "a dozen or so states, probably not super material this year" (Q1 2026). That progression is meaningful. Each quarter sounds optimistic in isolation. The trend is a gradual, narrative lowering of the near-term commitment level.

Case Study: Two CEOs, Same Quarter, Different Styles

To calibrate the Tesla example, compare to Tim Cook's typical Apple earnings call. Apple's style is notoriously consistent across quarters. The company delivers prepared remarks that stick almost verbatim to a formula. The Q&A gives precise, numbers-where-possible answers to analyst questions. Cook rarely reframes analyst questions; he answers them directly or explicitly declines to answer.

The contrast with Musk's style is stark. Musk uses more narrative, more first-person conviction, more reframing. Both styles are legitimate CEO communication strategies, and both contain information — but you have to read them differently.

The Apple pattern: analysts know what they will get. Answers are brief, specific, and numerically grounded. Tone rarely shifts. Information is extracted from what is not said (Apple rarely comments on specific products before launch) and from year-over-year changes in specific metric disclosures.

The Tesla pattern: analysts get narrative with embedded signal. Answers often reframe the question. Tone shifts substantially between topics. Information is extracted from the gap between ambition and commitment, between framing and quantification.

Neither is better. They require different analytical approaches. An investor holding both AAPL and TSLA needs to read each company's calls with a different listening framework — and applying the Apple framework to Tesla, or vice versa, misses the information each style actually communicates.

The Common Mistake: Reading the Summary Instead of Listening

The single most destructive habit among retail earnings-call listeners is reading a third-party summary afterward instead of listening live or reading the full transcript.

Summary articles — by design — extract the 3–5 most "newsworthy" statements. Those are usually the statements that move the stock the most in the short term. They are rarely the statements that matter the most for long-term investment thesis. The specific rhetorical patterns that reveal management's confidence level, the deflections that flag topics they cannot quantify, the tonal shifts that precede strategic changes by 2–3 quarters — all of these are lost in summary.

The 90-minute investment of listening to (or reading the full transcript of) a quarterly earnings call for any stock you hold for years produces information that 3-minute summaries cannot. Over a 5-year holding period, that is 20 calls at 90 minutes each — 30 hours total, for a position you might hold through several strategic transitions. This is a small investment of time for a genuinely non-trivial informational edge.

The Listening Checklist

For any earnings call you listen to, the following checklist converts passive listening into analytical review.

During the prepared remarks:

- Mark every piece of information not in the press release

- Flag specific framing language ("next era," "step function," "unprecedented")

- Note what topics get substantial airtime vs what topics get brief mention

- Compare topic emphasis to the previous 2–3 quarterly calls

During the Q&A:

- Track which analyst questions get direct numerical answers vs narrative responses

- Flag any reframes (where management redefines what was asked)

- Note when management volunteers information not directly asked — this is usually more revealing than the ostensible topic

- Flag any previously-emphasized items that are omitted

After the call:

- Reread your notes from the previous two calls

- Compare language evolution on 3–5 key topics quarter over quarter

- Mark any topics that have quietly disappeared from commentary

Brutal Edge Coverage Integration

This week's framework maps directly onto our coverage:

- TSLA Deep Dive Rev.2 (BEAF 58/C+) — the Tesla narrative-vs-quantification gap is explicitly part of our 58/C+ score. Our thesis decomposition incorporates the specific patterns we flagged from the Q1 2026 call and tracks how they evolve quarter over quarter.

- Physical AI Sector Report — the same listening framework is applied to Chinese AV programs, Waymo parent Alphabet's earnings calls, and humanoid robotics category earnings commentary. Cross-company call reading is where Tesla's relative position becomes clearest.

- NVDA Deep Dive (BEAF 83/B+) — a case where management's earnings call commentary has generally matched quantitative commitments. Jensen Huang's language has been notably direct on Blackwell and Rubin ramps, and the numbers have generally delivered.

- Microsoft Deep Dive (BEAF 81/B+) — the Q2 FY26 call specifically is a useful comparison point. Satya Nadella's commentary on Azure capacity ("demand remains significantly ahead of capacity") is direct and committal, contrasting with Tesla's more narrative style.

For additional frameworks, see our Deep Dive archive.

Looking Ahead

Next week we finish the disclosure trilogy with the proxy statement — the annual document where companies disclose how executives are paid, how the board operates, and what internal governance controls are in place. We examine Tesla's Musk 2028 CEO compensation package (targeting $1 trillion in market cap milestones) alongside Berkshire Hathaway's Buffett arrangement ($100,000 base salary, no bonus, no stock options) to show what the spectrum of executive incentive design looks like and why governance structure is one of the most underpriced factors in long-term returns.

For now, sit with this week's lesson. An earnings call is not a performance evaluation of last quarter. It is a real-time disclosure event where sophisticated outsiders pressure-test a company's narrative in public. Learning to read that pressure-test — not just the headline result — is one of the most consistent sources of information advantage available to any investor willing to put in the listening time.

Brutal Edge. Frameworks over forecasts. Signal over noise.

Disclaimer. Brutal Edge is an independent investment research platform. This report is published for educational and informational purposes only and does not constitute investment advice, a recommendation to buy or sell any security, or an offer to transact in any financial instrument. All valuations, forecasts, and opinions are the analyst's own and are subject to change without notice. Past performance does not guarantee future results. Readers should conduct their own due diligence and consult a qualified financial professional before making investment decisions.

Educational content only. Not investment advice. Always do your own research.