The Document That Reveals Who Really Runs the Company

In November 2025, Tesla shareholders approved the largest CEO compensation package in corporate history. Most retail investors who voted had never read the proxy statement. This week we use Musk vs. Buffett as a case study.

Proxy Statements

Every public company files a proxy statement once a year, typically in the weeks leading up to its annual shareholder meeting. The legal purpose is to inform shareholders about the items they will be voting on — director elections, executive compensation plans, auditor ratification, and whatever shareholder proposals have been submitted. That is the surface function.

The analytical function is different. A proxy statement is the one document where companies are legally required to disclose, in full detail, how executives are paid, how the board operates, which directors have potential conflicts of interest, which shareholders hold significant voting power, and what internal controls govern management's actions. Almost no retail investors read proxy statements. The ones who do understand why some companies compound capital for decades while others destroy it reliably.

This week we read two proxy statements that represent the philosophical extremes of US corporate governance. Tesla's 2025 proxy, which proposed and won approval for the single largest executive compensation package ever awarded. Berkshire Hathaway's annual proxy, which discloses Warren Buffett's $100,000 base salary (unchanged since 1980) and essentially zero other forms of compensation. These two companies are both S&P 500 constituents. Both are considered successful by most metrics. Both have approval from a majority of their shareholders. And their governance approaches are structurally opposite. The comparison reveals the full spectrum of incentive design — and tells you which questions to ask about any company you own.

Core Framework: The Four Sections of a Proxy That Actually Matter

A proxy statement has many sections. Four contain almost all the analytical content.

| Section | What It Discloses | What to Look For |

|---|---|---|

| Executive Compensation (CD&A) | How senior executives are paid, including structure, metrics, and totals | Alignment, performance metrics, pay mix, cap exposure |

| Board of Directors | Who sits on the board, their backgrounds, independence status, committees | Independence, relevant expertise, tenure, interlocks |

| Related-Party Transactions | Deals between the company and insiders | Any private benefit flowing to management or directors |

| Ownership Information | Who owns significant blocks of voting stock | Concentration, insider skin-in-game, potential conflicts |

Three other sections — the auditor relationship, shareholder proposals, and general governance policies — are usually less revealing per page but occasionally contain important signals.

Section 1: Executive Compensation — The CD&A

The Compensation Discussion and Analysis (CD&A) is the longest and most revealing section of any proxy statement. It typically runs 30–60 pages and describes, in granular detail, how the named executive officers are paid, what performance metrics trigger bonuses and equity awards, and what the total compensation for each executive was for the prior year.

The Musk 2025 CEO Performance Award: Maximum Variance

Tesla's 2025 proxy proposed an unprecedented compensation structure for Elon Musk. Key elements, as disclosed in the DEFA14A filings and approved by shareholders on November 6, 2025 with approximately 75 percent support:

Structure: 12 tranches of restricted stock, each representing approximately 1 percent of Tesla's outstanding shares. Total maximum award: approximately 423.7 million shares (~12 percent of Tesla's share count).

Market cap milestones (all 12 must be achieved for full vesting):

| Tranche | Market Cap Target |

|---|---|

| 1 | $2.0 trillion |

| 2 | $2.5 trillion |

| 3 | $3.0 trillion |

| 4 | $3.5 trillion |

| 5 | $4.0 trillion |

| 6 | $4.5 trillion |

| 7 | $5.0 trillion |

| 8 | $5.5 trillion |

| 9 | $6.0 trillion |

| 10 | $6.5 trillion |

| 11 | $7.5 trillion |

| 12 | $8.5 trillion |

Operational milestones (12 required, matched to market cap tranches):

- 20 million Tesla vehicles delivered (vs approximately 8 million cumulative at time of grant)

- 10 million active FSD subscriptions (vs ~1.3 million at time of disclosure)

- 1 million Optimus bots delivered

- 1 million Robotaxis in commercial operations

- $50B / $80B / $130B / $210B / $300B / $400B of Adjusted EBITDA milestones

- Additional $400B Adjusted EBITDA achievements over separate quarterly periods

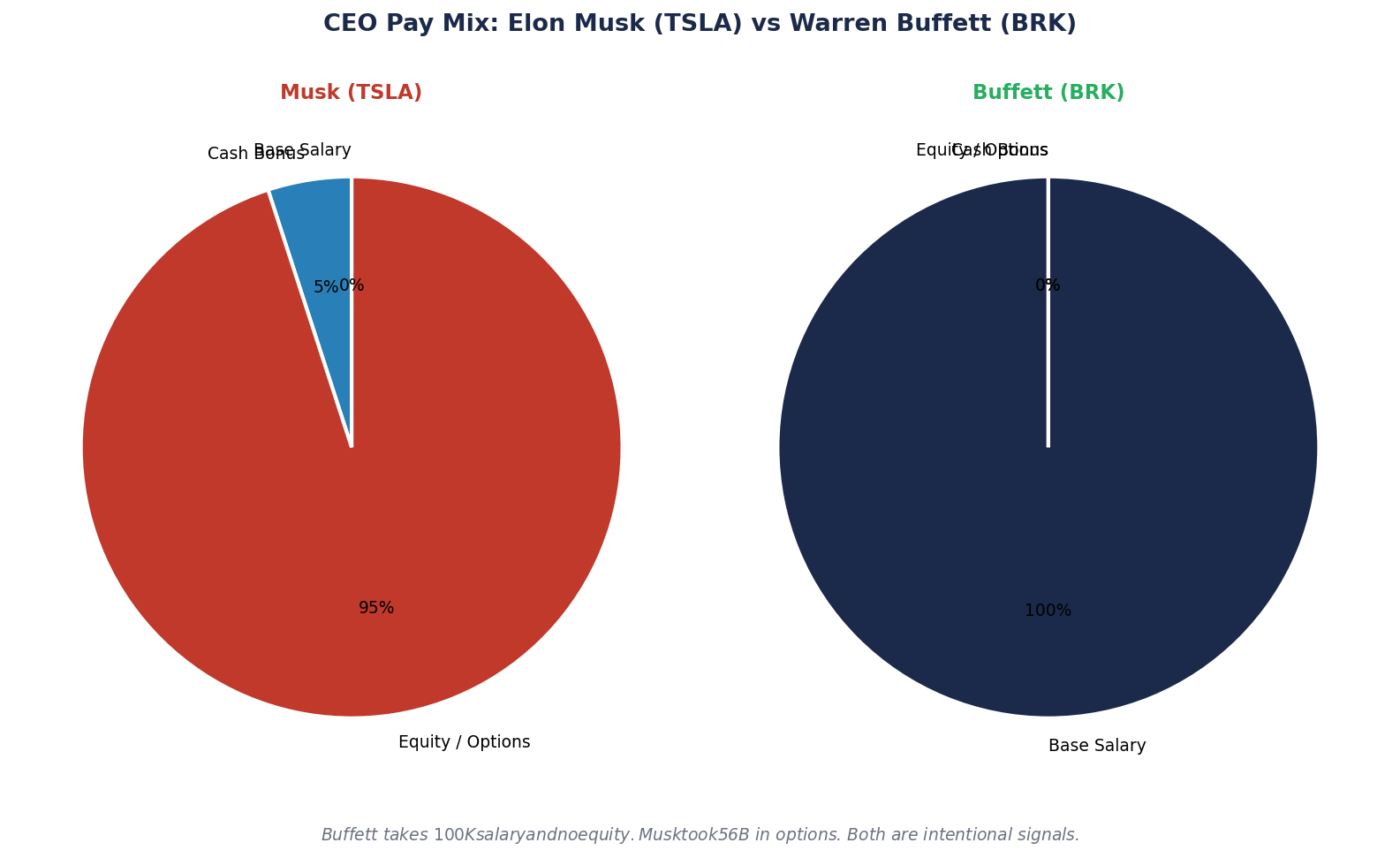

Base salary: $0. No guaranteed cash compensation.

Voting rights: If all milestones achieved, Musk's ownership increases from approximately 13 percent to 25 percent; voting power shifts accordingly.

Performance window: 10 years, with specific vesting periods in 2033 and 2035.

The Buffett Arrangement: Maximum Alignment Through Nothing

Berkshire Hathaway's proxy disclosures, filed annually, describe Warren Buffett's compensation in a single short paragraph in the CD&A:

- Base salary: $100,000 per year

- Bonus: $0

- Stock-based compensation: $0

- Stock option grants: $0

- Personal use of corporate aircraft: reimbursed by Buffett personally

- Total direct compensation: approximately $100,000 to $400,000 including disclosed perquisites and security costs

Salary increases: None since 1980.

Performance metrics tied to compensation: None.

Alignment mechanism: Buffett's personal ownership of Berkshire Hathaway, which represents the vast majority of his net worth. No formal incentive structure is required because Buffett's personal wealth outcomes are directly tied to the company's per-share intrinsic value growth through his equity position.

What the Contrast Actually Reveals

Read these two structures side by side.

Musk package:

- Alignment through future equity that must be earned via extreme milestones

- All upside; effectively no downside compensation

- Pay-at-risk in every sense

- If Tesla is a $500B company in 10 years instead of $8.5T, Musk receives $0

- If Tesla reaches $8.5T, Musk receives approximately $1T of stock

- Approval signals shareholder appetite for maximum variance incentive

Buffett structure:

- Alignment through existing equity ownership

- All risk is already in place through ownership concentration

- No formal incentive required because skin-in-the-game is total

- Salary is nearly symbolic

- Philosophy: "management and shareholders win and lose together as a matter of fact, not as a matter of contract"

Neither approach is inherently wrong. Both have produced compounding outcomes for their respective shareholders. What they reveal is a spectrum: at one end, maximum-variance incentive contracts that can create $1 trillion of personal wealth if extreme outcomes are achieved. At the other end, natural-alignment structures where management wealth moves with shareholder wealth simply because management is already a shareholder.

An investor's job is to understand which philosophy the company they own follows, because the two structures produce very different management behaviors over long periods.

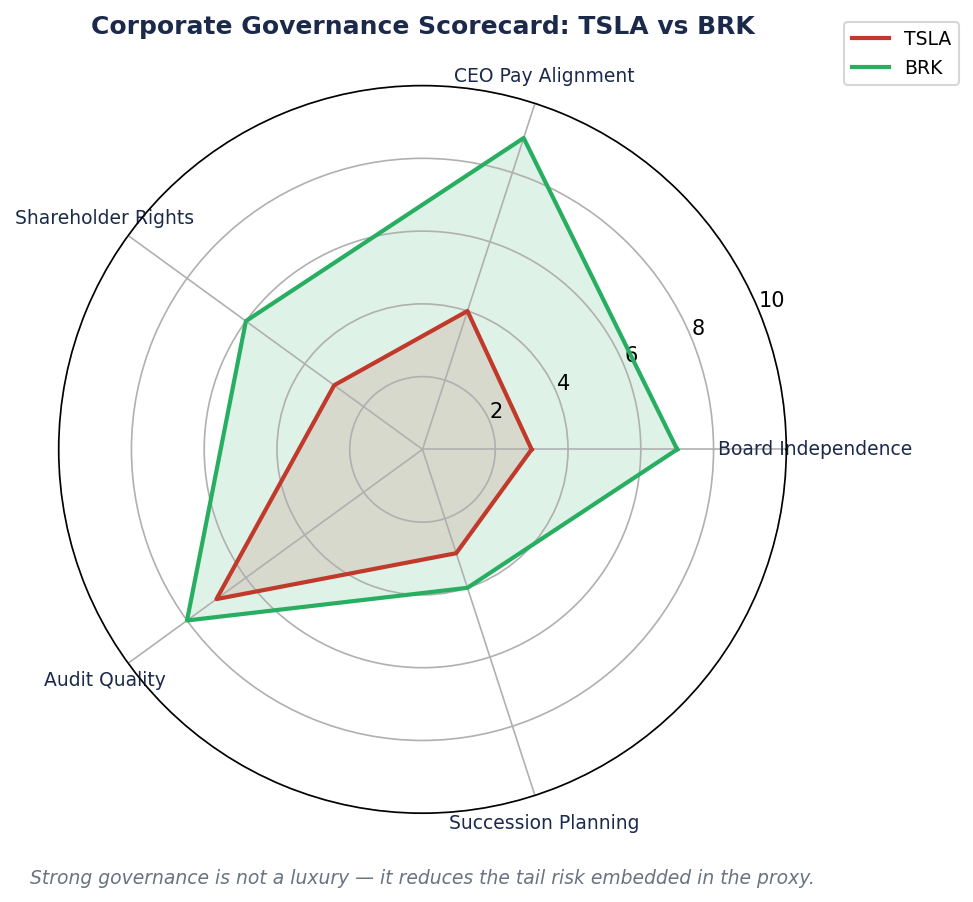

Section 2: Board of Directors — Independence and Expertise

The proxy's second most important section is the discussion of the board. This includes director biographies, committee memberships, independence classifications, and the annual director vote.

What to look for:

1. Independence ratio. The SEC and major stock exchanges require that a majority of directors be "independent" by specific criteria (no recent employment with the company, no material business relationship, no close family ties to senior executives). A company where 9 of 10 directors are independent generally has healthier oversight than one where 5 of 10 are independent — though independence is necessary, not sufficient.

2. Relevant expertise. The board of a technology company should contain directors with relevant operational experience. A board where everyone is a financial generalist or a professional board member may have less capacity to evaluate specific strategic decisions. Read each director's bio against the company's actual business.

3. Tenure. Very long tenures (15+ years) for directors can indicate either deep knowledge or entrenched interests. Very short tenures (fresh board every 3–4 years) can indicate either healthy refreshment or governance instability. Look at the distribution rather than any single tenure.

4. Interlocks and conflicts. Directors who sit on boards of customers, suppliers, or competitors have potential conflicts. Directors who are also members of management families or major shareholders have different potential conflicts. Both are disclosed in the proxy.

The Tesla Board Context

Tesla's proxy discloses a board that includes Robyn Denholm as chair, a mix of tech-industry directors, and — notably — Kimbal Musk, Elon's brother. The independence classifications have been the subject of significant debate in prior years, specifically the 2022 Tornetta v. Musk litigation in Delaware Chancery Court that challenged Musk's prior 2018 compensation package partly on board-independence grounds.

In reading Tesla's recent proxy, specific items worth flagging include: the approval process for the 2025 CEO Performance Award (including details of the negotiation between Musk and the board), the composition of the compensation committee specifically, and the discussion of "peer benchmarking" used to justify the package size.

The Berkshire Hathaway Board Context

Berkshire's board, by contrast, is notably stable and concentrated. It includes Buffett, Charlie Munger during his lifetime (who served until his 2023 passing), Buffett's son Howard Buffett (designated non-executive chairman in succession planning), Greg Abel (designated CEO successor), and a mix of long-tenured independent directors including Susan Decker, Meryl Witmer, and others.

The structure is unusual by modern governance standards — concentrated, family-inclusive, long-tenured — but the company's track record is equally unusual. The proxy is explicit that the Berkshire governance approach is intentional and that the board has planned a specific succession path.

Different approaches. Different results. Both approved by their shareholders. Governance is rarely one-size-fits-all.

Section 3: Related-Party Transactions

This section discloses any material transaction between the company and an insider — officer, director, major shareholder, or affiliated entity. For most companies, this section is brief or nonexistent. When it is long, it deserves close reading.

Types of related-party transactions to note:

- Leases where the company rents property from an officer or affiliated entity

- Purchases of goods or services from companies in which directors have ownership

- Loans to or from officers

- Family members on payroll

- Business dealings with other companies controlled by the same founder

- Payments for consulting or advisory services to former executives or directors

Each of these is legal if properly disclosed and approved. But each also represents a potential leak of shareholder value to insiders, and the cumulative pattern often matters more than any individual transaction.

Tesla-Adjacent Relationships

Tesla's proxies have historically disclosed various transactions involving Musk-related entities (SpaceX, Boring Company, xAI, Neuralink). The 2026 context includes the newly-announced Terafab project, which is a joint undertaking involving Tesla, SpaceX, and now Intel as a supplier. The related-party implications of such cross-Musk-entity projects are specifically addressed in proxy disclosures.

A reader of Tesla's proxy should specifically examine: revenue or expense flows between Tesla and SpaceX, the accounting treatment of any joint-development work, and the specific director approval trail for the 2025 CEO Award negotiation.

Section 4: Ownership Structure

The proxy discloses the largest beneficial owners of the company's voting shares. This information is also available through 13-F and 13-G filings, but the proxy presents it in one place with additional context.

What to look for:

1. Insider ownership percentage. How much of the company do officers and directors own? For Tesla, Musk's stake was approximately 13 percent at the time of the 2025 proxy and would rise to approximately 25 percent if all compensation milestones are achieved. For Berkshire, Buffett has personally owned the vast majority of his voting power since the 1960s.

2. Major institutional holders. Index funds (Vanguard, BlackRock, State Street) typically hold 5–10 percent each in large-cap US equities. The specific mix can indicate whether active managers or passive funds dominate the shareholder base.

3. Dual-class structures and special voting rights. Many modern technology companies have dual-class share structures that give founders voting power disproportionate to economic ownership. Tesla does not. Berkshire does (Class A and Class B with different voting rights).

4. Concentration risk. A company where any single shareholder holds more than 10 percent of voting power has a different governance profile than one with highly diffuse ownership. The concentration may be helpful (aligned founder leadership) or harmful (entrenched control with no accountability). The analytical question is which.

The Tornetta v. Musk Precedent

Worth noting separately because it features in both Tesla's history and in broader discussions of executive compensation governance: the Delaware Chancery Court ruling in Tornetta v. Musk (January 2024) rescinded Musk's prior 2018 CEO compensation package on the grounds that the Tesla board was insufficiently independent in its approval process and that shareholders were not fully informed.

The 2025 CEO Performance Award was explicitly designed in the aftermath of Tornetta. The proxy language around the 2025 award — including heavier emphasis on board independence, extensive shareholder communication (the DEFA14A filings), and specific operational milestones that were not present in the 2018 package — reflects lessons learned from the litigation. The November 2025 shareholder vote, at 75 percent approval, was explicitly framed by the company as a response to the Tornetta ruling: a second, clearer mandate from shareholders.

An investor reading the Tesla 2025 proxy should understand this context. The structure is not normal. It is specifically designed around the legal and governance pressure points that emerged in the prior litigation.

Case Study: Reading the Disclosure Gap

Here is the most important analytical exercise with proxy statements. Read three consecutive years from the same company and mark every change.

For Tesla, a three-year proxy comparison surfaces:

- The evolution of Musk's compensation structure from the 2018 package (Tornetta-rescinded), to the immediate post-rescission period, to the 2025 Performance Award

- Changes to the board composition and committee assignments

- Growing disclosure around related-party arrangements involving SpaceX and other Musk-affiliated entities

- Year-over-year changes in the description of the CEO succession plan (significantly expanded in the 2025 proxy as part of the new compensation award)

For Berkshire, a three-year proxy comparison surfaces:

- The formalization of the Greg Abel CEO-succession plan following Charlie Munger's death in 2023

- Modest evolution in director composition

- Consistently minimal changes to Buffett's compensation (the pattern itself is the signal — the company is governance-stable by intent)

The delta-based reading is where proxy analysis produces the highest analytical yield. A single year's proxy gives you a snapshot. Three years compared gives you a trajectory.

The Common Mistake: Skipping the Proxy Because "They All Look the Same"

Retail investors tend to skip proxy statements because they look long, legalistic, and repetitive. The section headings are similar across companies. The language is careful. The formatting is dense. It is easy to conclude that there is nothing to find.

This is exactly wrong. Proxies look similar because SEC rules require common sections — but the content varies enormously company to company. Two competitors in the same industry can have proxies that look structurally identical and disclose wildly different governance practices. A company where insiders own 1 percent and have guaranteed $50M-per-year compensation packages is fundamentally different from a company where insiders own 15 percent and earn modest salaries with performance equity. That difference is not visible anywhere except in the proxy.

The fix is to read one proxy per holding per year, full text, with specific attention to the four sections above. A careful read of a proxy takes 45–60 minutes. Over a 10-holding portfolio, this is 10 hours annually — less than a full workday in total. The information extracted compounds across years of holding and becomes meaningful precisely at moments of governance stress (compensation votes, succession events, takeover attempts, dividend changes) where other information is noisy.

What to Watch

Three habits will turn proxy reading from a formality into a real analytical input.

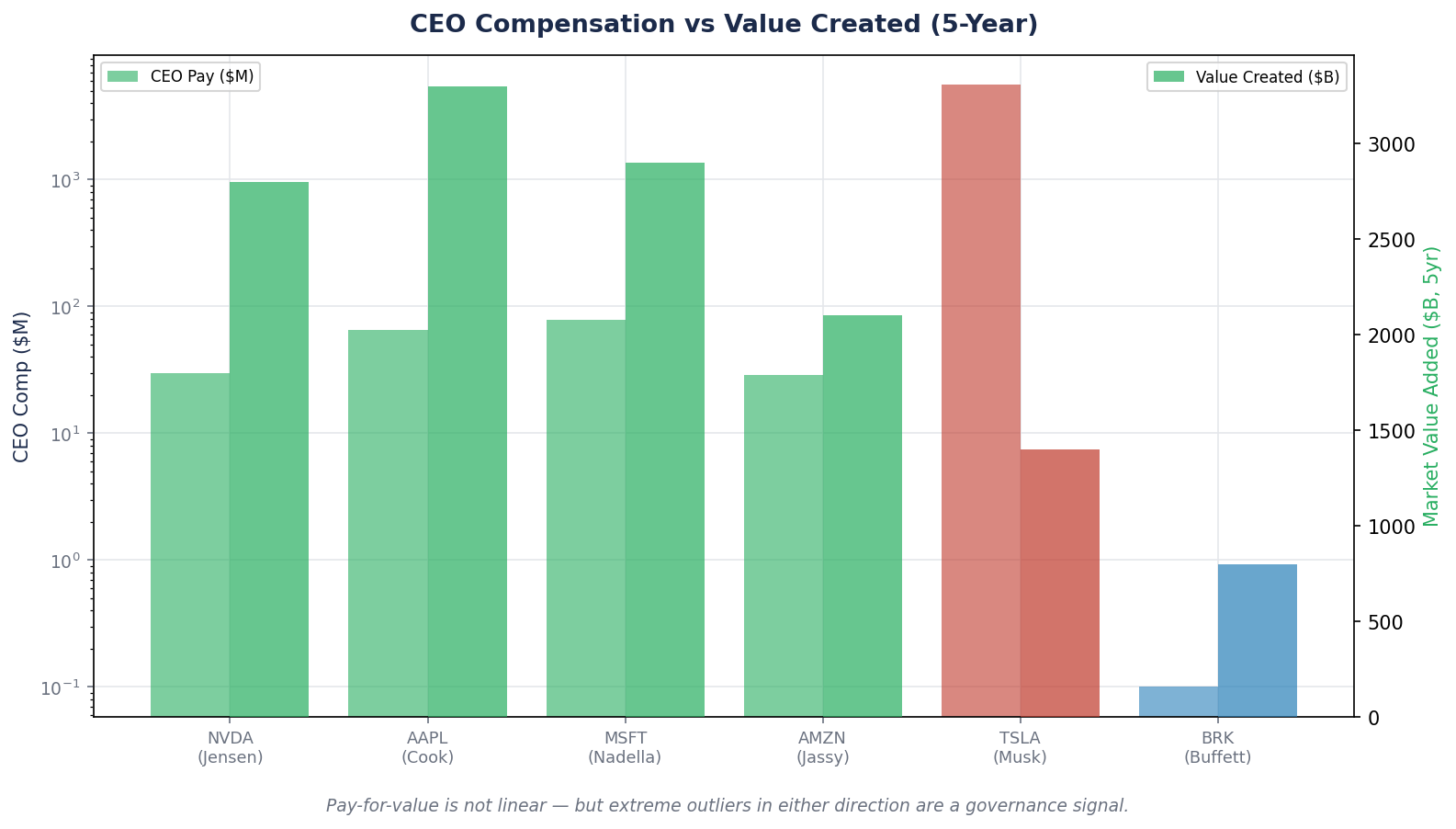

Watch executive pay growth versus per-share business value growth. The single cleanest governance signal is the ratio of CEO compensation to per-share intrinsic value growth over a multi-year window. If the CEO's compensation has grown 40 percent over five years while per-share earnings have grown 15 percent, the gap is a governance signal. If the relationship is tight across years, the incentive structure is working.

Watch for significant changes to the compensation philosophy. A company that shifts its performance metrics — for example, from EPS growth to "adjusted EBITDA" or from stock price to "strategic milestones" — is telling you something. Performance metrics evolve for good reasons (changing business model) and bad reasons (missing the original targets and needing easier ones). Reading the CD&A carefully will usually distinguish which is happening.

Watch for specific director activity. When specific directors join audit or compensation committees, when long-tenured directors step down, when new directors with specific expertise are added — these are deliberate signals. A board that is refreshing its technology expertise is preparing for a strategic transition. A board that is adding financial experts after a restatement is responding to a control failure. Board composition is a lagging indicator of internal events.

Brutal Edge Coverage Integration

This week's framework maps directly onto our coverage:

- TSLA Deep Dive Rev.2 (BEAF 58/C+) — our governance analysis of the 2025 CEO Performance Award, including the specific tranches, the operational milestone structure, and the shareholder-approval context after Tornetta. The governance discussion is a specific component of the 58/C+ score.

- Physical AI Sector Report — covers governance differentials across the Physical AI category, including how founder-dominated governance structures (Tesla, some Chinese AV programs) compare to more traditional governance at hyperscalers (Alphabet, Amazon) on decision velocity and capital-allocation discipline.

- Microsoft Deep Dive (BEAF 81/B+) — Microsoft's proxy disclosures provide a useful mid-point between the Tesla and Berkshire extremes. Satya Nadella's compensation is performance-driven with significant stock-based elements, but structured within a standard large-cap technology framework rather than the Musk-level variance.

- Anthropic Private Investor Report — for private-company governance, the relevant parallel is the Public Benefit Corporation structure combined with the "long-term benefit trust" governance mechanism Anthropic has adopted. Private-company governance documents are not filed as proxies but follow analogous principles.

For additional frameworks, see our Deep Dive archive.

Looking Ahead

This week closes the disclosure module. You now have the frameworks to read the three core public-company documents — the 10-K (legal truth), the earnings call (real-time management), and the proxy (governance and alignment). Over the next three weeks we shift from document-reading to portfolio construction: how to size the positions that result from this analysis. Next week we tackle one of the least-taught skills in retail investing: the Kelly Criterion and its application to conviction-based position sizing. We take three names from the Brutal Edge coverage universe — NVDA, TSLA, MSFT — and apply the Kelly framework to actual position sizes based on their scores, expected returns, and downside exposures.

For now, sit with this week's lesson. A proxy statement is not a routine regulatory filing. It is a window into how a company is actually governed, and over long holding periods, governance determines an enormous portion of outcomes. The asymmetry — publicly disclosed, rarely read — is the opportunity. Forty-five minutes per year per holding is a small price for durable investment insight.

Brutal Edge. Frameworks over forecasts. Signal over noise.

Disclaimer. Brutal Edge is an independent investment research platform. This report is published for educational and informational purposes only and does not constitute investment advice, a recommendation to buy or sell any security, or an offer to transact in any financial instrument. All valuations, forecasts, and opinions are the analyst's own and are subject to change without notice. Past performance does not guarantee future results. Readers should conduct their own due diligence and consult a qualified financial professional before making investment decisions.

Educational content only. Not investment advice. Always do your own research.